Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:KAB

These 4 Measures Indicate That Kejuruteraanstera Berhad (KLSE:KAB) Is Using Debt Extensively

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Kejuruteraan Asastera Berhad (KLSE:KAB) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Kejuruteraanstera Berhad

What Is Kejuruteraanstera Berhad's Debt?

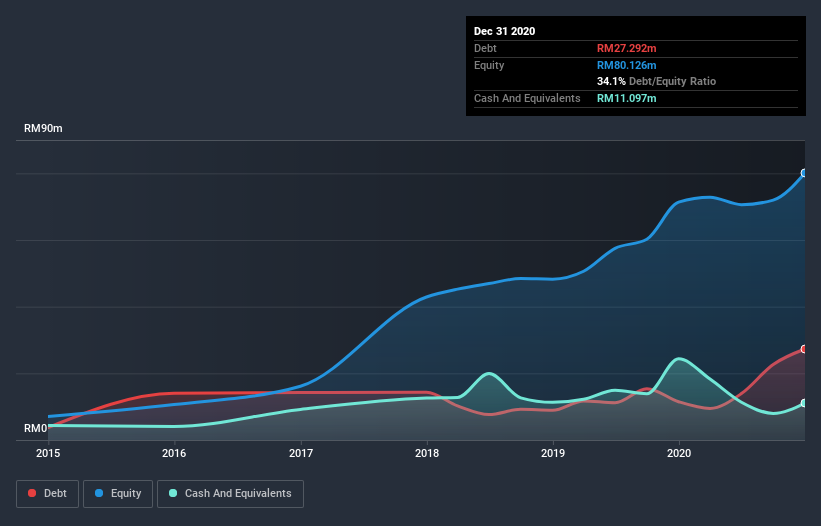

As you can see below, at the end of December 2020, Kejuruteraanstera Berhad had RM27.3m of debt, up from RM11.5m a year ago. Click the image for more detail. However, because it has a cash reserve of RM11.1m, its net debt is less, at about RM16.2m.

A Look At Kejuruteraanstera Berhad's Liabilities

Zooming in on the latest balance sheet data, we can see that Kejuruteraanstera Berhad had liabilities of RM76.0m due within 12 months and liabilities of RM8.81m due beyond that. On the other hand, it had cash of RM11.1m and RM111.6m worth of receivables due within a year. So it actually has RM37.9m more liquid assets than total liabilities.

This surplus suggests that Kejuruteraanstera Berhad has a conservative balance sheet, and could probably eliminate its debt without much difficulty. But either way, Kejuruteraanstera Berhad has virtually no net debt, so it's fair to say it does not have a heavy debt load!

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Kejuruteraanstera Berhad's net debt of 1.6 times EBITDA suggests graceful use of debt. And the alluring interest cover (EBIT of 8.1 times interest expense) certainly does not do anything to dispel this impression. The modesty of its debt load may become crucial for Kejuruteraanstera Berhad if management cannot prevent a repeat of the 45% cut to EBIT over the last year. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Kejuruteraanstera Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Kejuruteraanstera Berhad saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

While Kejuruteraanstera Berhad's conversion of EBIT to free cash flow makes us cautious about it, its track record of (not) growing its EBIT is no better. But its not so bad at covering its interest expense with its EBIT. When we consider all the factors discussed, it seems to us that Kejuruteraanstera Berhad is taking some risks with its use of debt. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for Kejuruteraanstera Berhad you should be aware of, and 1 of them is concerning.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade Kejuruteraanstera Berhad, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kinergy Advancement Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:KAB

Kinergy Advancement Berhad

Provides electrical and mechanical engineering services for commercial, industrial, and residential infrastructure in Malaysia, Vietnam, Thailand, Indonesia, and Hong Kong.

High growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor