Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:KAB

Returns On Capital Signal Tricky Times Ahead For Kejuruteraanstera Berhad (KLSE:KAB)

If you're looking for a multi-bagger, there's a few things to keep an eye out for. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Although, when we looked at Kejuruteraanstera Berhad (KLSE:KAB), it didn't seem to tick all of these boxes.

What Is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Kejuruteraanstera Berhad is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

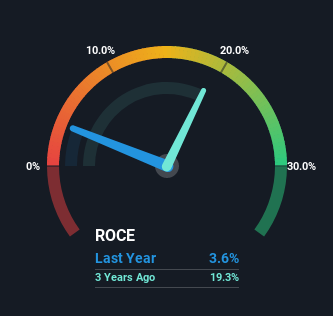

0.036 = RM6.4m ÷ (RM267m - RM90m) (Based on the trailing twelve months to December 2022).

Therefore, Kejuruteraanstera Berhad has an ROCE of 3.6%. Ultimately, that's a low return and it under-performs the Construction industry average of 4.9%.

View our latest analysis for Kejuruteraanstera Berhad

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Kejuruteraanstera Berhad's past further, check out this free graph of past earnings, revenue and cash flow.

How Are Returns Trending?

Unfortunately, the trend isn't great with ROCE falling from 23% five years ago, while capital employed has grown 261%. Usually this isn't ideal, but given Kejuruteraanstera Berhad conducted a capital raising before their most recent earnings announcement, that would've likely contributed, at least partially, to the increased capital employed figure. It's unlikely that all of the funds raised have been put to work yet, so as a consequence Kejuruteraanstera Berhad might not have received a full period of earnings contribution from it.

On a related note, Kejuruteraanstera Berhad has decreased its current liabilities to 34% of total assets. That could partly explain why the ROCE has dropped. What's more, this can reduce some aspects of risk to the business because now the company's suppliers or short-term creditors are funding less of its operations. Some would claim this reduces the business' efficiency at generating ROCE since it is now funding more of the operations with its own money.

The Bottom Line On Kejuruteraanstera Berhad's ROCE

To conclude, we've found that Kejuruteraanstera Berhad is reinvesting in the business, but returns have been falling. Investors must think there's better things to come because the stock has knocked it out of the park, delivering a 463% gain to shareholders who have held over the last five years. Ultimately, if the underlying trends persist, we wouldn't hold our breath on it being a multi-bagger going forward.

If you want to know some of the risks facing Kejuruteraanstera Berhad we've found 4 warning signs (2 make us uncomfortable!) that you should be aware of before investing here.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if Kinergy Advancement Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KAB

Kinergy Advancement Berhad

Provides electrical and mechanical engineering services for commercial, industrial, and residential infrastructure in Malaysia, Vietnam, Thailand, Indonesia, and Hong Kong.

High growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor