Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:GADANG

This Gadang Holdings Berhad (KLSE:GADANG) Analyst Is Way More Bearish Than They Used To Be

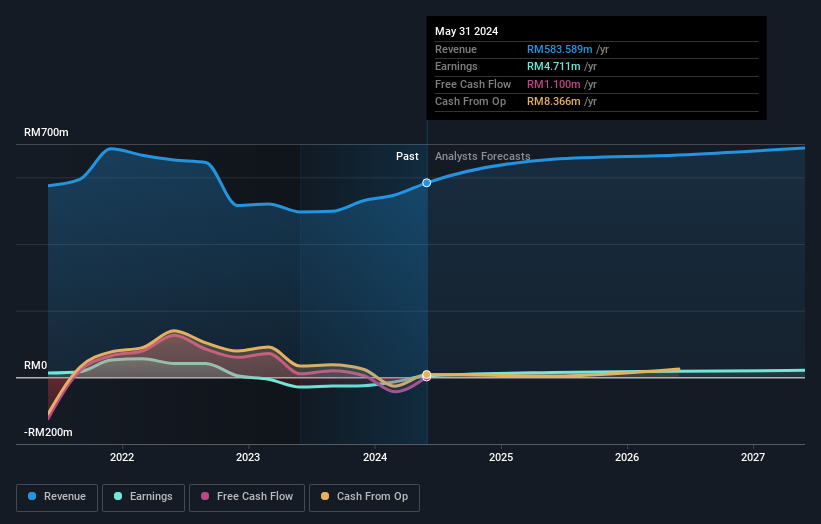

The latest analyst coverage could presage a bad day for Gadang Holdings Berhad (KLSE:GADANG), with the covering analyst making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analyst has soured majorly on the business.

Following the downgrade, the current consensus from Gadang Holdings Berhad's one analyst is for revenues of RM654m in 2025 which - if met - would reflect a solid 12% increase on its sales over the past 12 months. Statutory earnings per share are presumed to shoot up 209% to RM0.02. Previously, the analyst had been modelling revenues of RM738m and earnings per share (EPS) of RM0.026 in 2025. Indeed, we can see that the analyst is a lot more bearish about Gadang Holdings Berhad's prospects, administering a measurable cut to revenue estimates and slashing their EPS estimates to boot.

Check out our latest analysis for Gadang Holdings Berhad

The consensus price target fell 12% to RM0.37, with the weaker earnings outlook clearly leading analyst valuation estimates.

Of course, another way to look at these forecasts is to place them into context against the industry itself. For example, we noticed that Gadang Holdings Berhad's rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 12% growth to the end of 2025 on an annualised basis. That is well above its historical decline of 6.2% a year over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 12% annually. So it looks like Gadang Holdings Berhad is expected to grow at about the same rate as the wider industry.

The Bottom Line

The biggest issue in the new estimates is that the analyst has reduced their earnings per share estimates, suggesting business headwinds lay ahead for Gadang Holdings Berhad. Lamentably, they also downgraded their sales forecasts, but the business is still expected to grow at roughly the same rate as the market itself. With a serious cut to this year's expectations and a falling price target, we wouldn't be surprised if investors were becoming wary of Gadang Holdings Berhad.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At least one analyst has provided forecasts out to 2027, which can be seen for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KLSE:GADANG

Gadang Holdings Berhad

An investment holding company, engages in civil engineering and construction, property development, water supply, and mechanical and electrical engineering businesses in Malaysia, Indonesia, and Singapore.

Excellent balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% undervalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|45.0% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.4% undervalued

TI

Community Contributor