Advertisement

- Malaysia

- /

- Trade Distributors

- /

- KLSE:ENGTEX

Engtex Group Berhad (KLSE:ENGTEX) Looks Just Right With A 25% Price Jump

Despite an already strong run, Engtex Group Berhad (KLSE:ENGTEX) shares have been powering on, with a gain of 25% in the last thirty days. Looking back a bit further, it's encouraging to see the stock is up 73% in the last year.

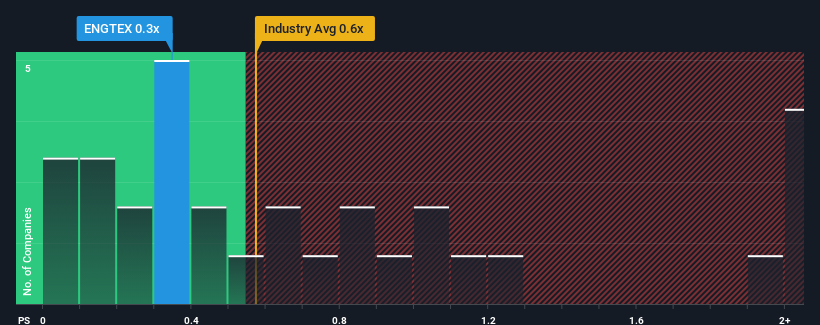

Although its price has surged higher, it's still not a stretch to say that Engtex Group Berhad's price-to-sales (or "P/S") ratio of 0.3x right now seems quite "middle-of-the-road" compared to the Trade Distributors industry in Malaysia, where the median P/S ratio is around 0.6x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Engtex Group Berhad

How Engtex Group Berhad Has Been Performing

While the industry has experienced revenue growth lately, Engtex Group Berhad's revenue has gone into reverse gear, which is not great. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Engtex Group Berhad.Is There Some Revenue Growth Forecasted For Engtex Group Berhad?

The only time you'd be comfortable seeing a P/S like Engtex Group Berhad's is when the company's growth is tracking the industry closely.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 1.1%. Even so, admirably revenue has lifted 51% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Turning to the outlook, the next year should generate growth of 4.0% as estimated by the dual analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 2.8%, which is not materially different.

With this information, we can see why Engtex Group Berhad is trading at a fairly similar P/S to the industry. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Final Word

Engtex Group Berhad appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

A Engtex Group Berhad's P/S seems about right to us given the knowledge that analysts are forecasting a revenue outlook that is similar to the Trade Distributors industry. Right now shareholders are comfortable with the P/S as they are quite confident future revenue won't throw up any surprises. Unless these conditions change, they will continue to support the share price at these levels.

You need to take note of risks, for example - Engtex Group Berhad has 2 warning signs (and 1 which makes us a bit uncomfortable) we think you should know about.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Engtex Group Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:ENGTEX

Engtex Group Berhad

Engages in the wholesale and distribution of pipes, valves, fittings, plumbing materials, steel related products, general hardware products, and construction materials in Malaysia.

Proven track record with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor