Advertisement

- Malaysia

- /

- Trade Distributors

- /

- KLSE:DKSH

Returns On Capital At DKSH Holdings (Malaysia) Berhad (KLSE:DKSH) Have Stalled

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. That's why when we briefly looked at DKSH Holdings (Malaysia) Berhad's (KLSE:DKSH) ROCE trend, we were pretty happy with what we saw.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on DKSH Holdings (Malaysia) Berhad is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.18 = RM153m ÷ (RM2.8b - RM2.0b) (Based on the trailing twelve months to September 2021).

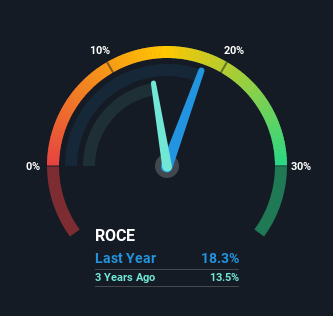

Thus, DKSH Holdings (Malaysia) Berhad has an ROCE of 18%. In absolute terms, that's a satisfactory return, but compared to the Trade Distributors industry average of 6.8% it's much better.

See our latest analysis for DKSH Holdings (Malaysia) Berhad

Above you can see how the current ROCE for DKSH Holdings (Malaysia) Berhad compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering DKSH Holdings (Malaysia) Berhad here for free.

What Does the ROCE Trend For DKSH Holdings (Malaysia) Berhad Tell Us?

While the current returns on capital are decent, they haven't changed much. Over the past five years, ROCE has remained relatively flat at around 18% and the business has deployed 61% more capital into its operations. 18% is a pretty standard return, and it provides some comfort knowing that DKSH Holdings (Malaysia) Berhad has consistently earned this amount. Stable returns in this ballpark can be unexciting, but if they can be maintained over the long run, they often provide nice rewards to shareholders.

On a separate but related note, it's important to know that DKSH Holdings (Malaysia) Berhad has a current liabilities to total assets ratio of 70%, which we'd consider pretty high. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Bottom Line

In the end, DKSH Holdings (Malaysia) Berhad has proven its ability to adequately reinvest capital at good rates of return. However, over the last five years, the stock has only delivered a 21% return to shareholders who held over that period. So to determine if DKSH Holdings (Malaysia) Berhad is a multi-bagger going forward, we'd suggest digging deeper into the company's other fundamentals.

One more thing, we've spotted 2 warning signs facing DKSH Holdings (Malaysia) Berhad that you might find interesting.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:DKSH

DKSH Holdings (Malaysia) Berhad

An investment holding company, provides market expansion services to consumer goods, performance materials, healthcare, and technology industries.

Proven track record with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.8% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|43.5% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|61.4% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor