- Malaysia

- /

- Aerospace & Defense

- /

- KLSE:DESTINI

Lacklustre Performance Is Driving Destini Berhad's (KLSE:DESTINI) 57% Price Drop

The Destini Berhad (KLSE:DESTINI) share price has fared very poorly over the last month, falling by a substantial 57%. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 44% in that time.

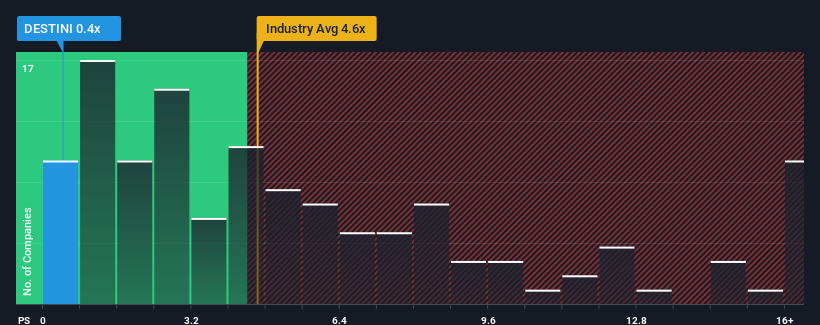

Following the heavy fall in price, Destini Berhad may look like a strong buying opportunity at present with its price-to-sales (or "P/S") ratio of 0.4x, considering almost half of all companies in the Aerospace & Defense industry in Malaysia have P/S ratios greater than 4.6x and even P/S higher than 9x aren't out of the ordinary. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Destini Berhad

How Has Destini Berhad Performed Recently?

Recent times have been quite advantageous for Destini Berhad as its revenue has been rising very briskly. It might be that many expect the strong revenue performance to degrade substantially, which has repressed the P/S ratio. Those who are bullish on Destini Berhad will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Destini Berhad's earnings, revenue and cash flow.Is There Any Revenue Growth Forecasted For Destini Berhad?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like Destini Berhad's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 46%. However, this wasn't enough as the latest three year period has seen the company endure a nasty 12% drop in revenue in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

In contrast to the company, the rest of the industry is expected to grow by 35% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

With this in mind, we understand why Destini Berhad's P/S is lower than most of its industry peers. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Key Takeaway

Destini Berhad's P/S looks about as weak as its stock price lately. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Destini Berhad confirms that the company's shrinking revenue over the past medium-term is a key factor in its low price-to-sales ratio, given the industry is projected to grow. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Given the current circumstances, it seems unlikely that the share price will experience any significant movement in either direction in the near future if recent medium-term revenue trends persist.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Destini Berhad (of which 1 is potentially serious!) you should know about.

If you're unsure about the strength of Destini Berhad's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:DESTINI

Destini Berhad

An investment holding company, provides engineering solutions worldwide.

Adequate balance sheet and slightly overvalued.

Market Insights

Community Narratives