- Malaysia

- /

- Construction

- /

- KLSE:BINTAI

Bintai Kinden Corporation Berhad (KLSE:BINTAI) Seems To Be Using A Lot Of Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Bintai Kinden Corporation Berhad (KLSE:BINTAI) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Bintai Kinden Corporation Berhad

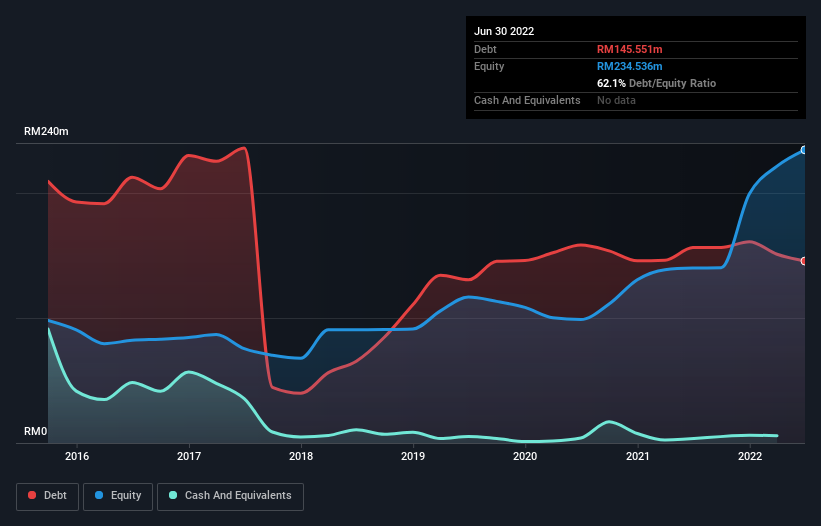

What Is Bintai Kinden Corporation Berhad's Net Debt?

You can click the graphic below for the historical numbers, but it shows that Bintai Kinden Corporation Berhad had RM145.6m of debt in June 2022, down from RM156.3m, one year before. On the flip side, it has RM5.75m in cash leading to net debt of about RM139.8m.

How Healthy Is Bintai Kinden Corporation Berhad's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Bintai Kinden Corporation Berhad had liabilities of RM100.9m due within 12 months and liabilities of RM126.9m due beyond that. Offsetting this, it had RM5.75m in cash and RM120.9m in receivables that were due within 12 months. So it has liabilities totalling RM101.2m more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's market capitalization of RM68.3m, we think shareholders really should watch Bintai Kinden Corporation Berhad's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Weak interest cover of 1.3 times and a disturbingly high net debt to EBITDA ratio of 10.8 hit our confidence in Bintai Kinden Corporation Berhad like a one-two punch to the gut. The debt burden here is substantial. Looking on the bright side, Bintai Kinden Corporation Berhad boosted its EBIT by a silky 74% in the last year. Like the milk of human kindness that sort of growth increases resilience, making the company more capable of managing debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Bintai Kinden Corporation Berhad's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. During the last two years, Bintai Kinden Corporation Berhad burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

To be frank both Bintai Kinden Corporation Berhad's net debt to EBITDA and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. Overall, it seems to us that Bintai Kinden Corporation Berhad's balance sheet is really quite a risk to the business. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Bintai Kinden Corporation Berhad is showing 5 warning signs in our investment analysis , and 3 of those make us uncomfortable...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Bintai Kinden Corporation Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:BINTAI

Bintai Kinden Corporation Berhad

An investment holding company, provides specialized mechanical and electrical engineering services in South-East Asia, China, and the Arabian Gulf region.

Acceptable track record with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives