Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Bina Darulaman Berhad (KLSE:BDB) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Bina Darulaman Berhad

What Is Bina Darulaman Berhad's Net Debt?

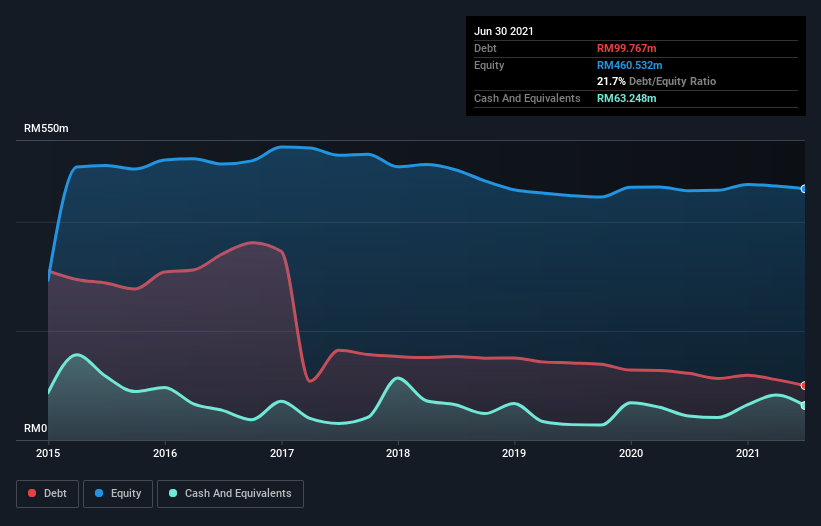

As you can see below, Bina Darulaman Berhad had RM99.8m of debt at June 2021, down from RM122.3m a year prior. However, it does have RM63.2m in cash offsetting this, leading to net debt of about RM36.5m.

How Strong Is Bina Darulaman Berhad's Balance Sheet?

According to the last reported balance sheet, Bina Darulaman Berhad had liabilities of RM180.8m due within 12 months, and liabilities of RM28.2m due beyond 12 months. On the other hand, it had cash of RM63.2m and RM78.3m worth of receivables due within a year. So its liabilities total RM67.5m more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Bina Darulaman Berhad has a market capitalization of RM176.2m, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Bina Darulaman Berhad's net debt is sitting at a very reasonable 1.7 times its EBITDA, while its EBIT covered its interest expense just 2.5 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. Unfortunately, Bina Darulaman Berhad's EBIT flopped 18% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Bina Darulaman Berhad's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last two years, Bina Darulaman Berhad actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

Neither Bina Darulaman Berhad's ability to grow its EBIT nor its interest cover gave us confidence in its ability to take on more debt. But its conversion of EBIT to free cash flow tells a very different story, and suggests some resilience. We think that Bina Darulaman Berhad's debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 4 warning signs we've spotted with Bina Darulaman Berhad (including 1 which is potentially serious) .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Bina Darulaman Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:BDB

Bina Darulaman Berhad

An investment holding company, engages in the oil palm plantation, property development, and management service businesses in Malaysia.

Excellent balance sheet low.

Market Insights

Community Narratives