Advertisement

Gruma. de (BMV:GRUMAB) Will Pay A Larger Dividend Than Last Year At $1.35

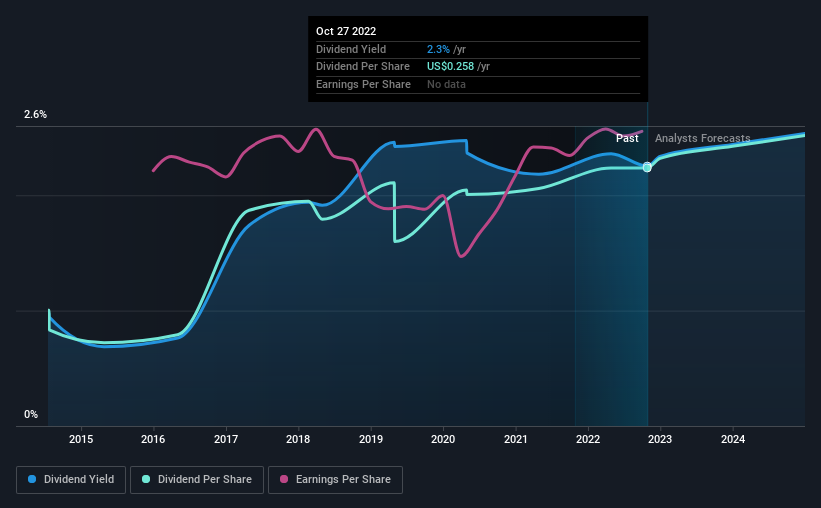

The board of Gruma, S.A.B. de C.V. (BMV:GRUMAB) has announced that it will be paying its dividend of $1.35 on the 6th of January, an increased payment from last year's comparable dividend. This takes the dividend yield to 2.3%, which shareholders will be pleased with.

Check out the opportunities and risks within the MX Food industry.

Gruma. de Is Paying Out More Than It Is Earning

A big dividend yield for a few years doesn't mean much if it can't be sustained. Prior to this announcement, Gruma. de's earnings easily covered the dividend, but free cash flows were negative. With the company not bringing in any cash, paying out to shareholders is bound to become difficult at some point.

The next 12 months is set to see EPS grow by 50.8%. Assuming the dividend continues along recent trends, we think the payout ratio could get very high, which probably can't continue without starting to put some pressure on the balance sheet.

Gruma. de Doesn't Have A Long Payment History

The dividend's track record has been pretty solid, but with only 8 years of history we want to see a few more years of history before making any solid conclusions. Since 2014, the annual payment back then was $0.116, compared to the most recent full-year payment of $0.258. This means that it has been growing its distributions at 11% per annum over that time. It is always nice to see strong dividend growth, but with such a short payment history we wouldn't be inclined to rely on it until a longer track record can be developed.

The Dividend's Growth Prospects Are Limited

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Unfortunately, Gruma. de's earnings per share has been essentially flat over the past five years, which means the dividend may not be increased each year. While growth may be thin on the ground, Gruma. de could always pay out a higher proportion of earnings to increase shareholder returns.

In Summary

Overall, we always like to see the dividend being raised, but we don't think Gruma. de will make a great income stock. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would probably look elsewhere for an income investment.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Case in point: We've spotted 2 warning signs for Gruma. de (of which 1 doesn't sit too well with us!) you should know about. Is Gruma. de not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BMV:GRUMA B

Gruma. de

Manufactures and sells corn flour, tortillas, corn chips, and other related products in the United States, Mexico, Europe, Central America, Asia, and Oceania.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor