Advertisement

- Mexico

- /

- Food and Staples Retail

- /

- BMV:CHDRAUI B

These 4 Measures Indicate That Grupo Comercial Chedraui. de (BMV:CHDRAUIB) Is Using Debt Extensively

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk'. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Grupo Comercial Chedraui, S.A.B. de C.V. (BMV:CHDRAUIB) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Grupo Comercial Chedraui. de

How Much Debt Does Grupo Comercial Chedraui. de Carry?

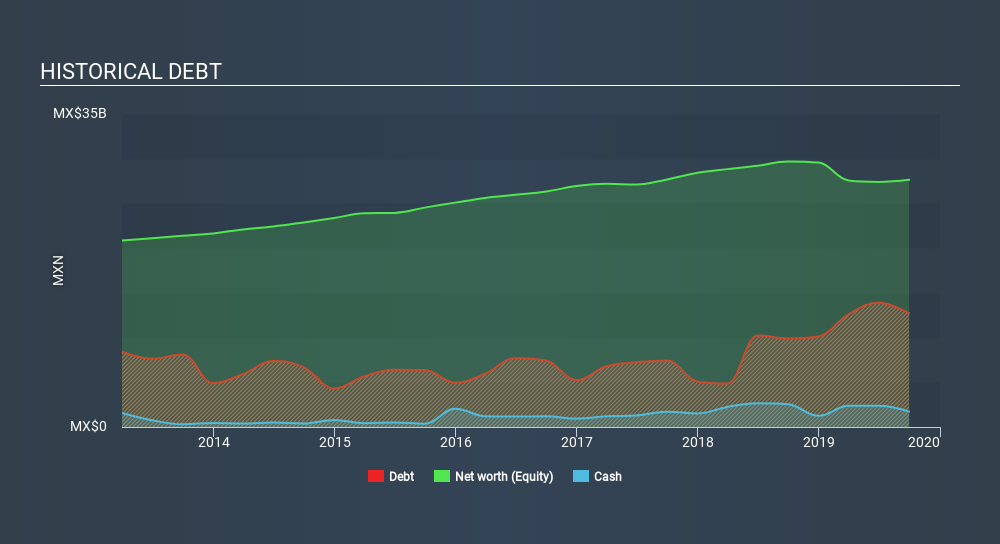

As you can see below, at the end of September 2019, Grupo Comercial Chedraui. de had Mex$12.7b of debt, up from Mex$9.9k a year ago. Click the image for more detail. However, it does have Mex$1.72b in cash offsetting this, leading to net debt of about Mex$11.0b.

A Look At Grupo Comercial Chedraui. de's Liabilities

We can see from the most recent balance sheet that Grupo Comercial Chedraui. de had liabilities of Mex$24.6b falling due within a year, and liabilities of Mex$37.4b due beyond that. Offsetting these obligations, it had cash of Mex$1.72b as well as receivables valued at Mex$3.47b due within 12 months. So its liabilities total Mex$56.8b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the Mex$26.5b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Grupo Comercial Chedraui. de would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Grupo Comercial Chedraui. de's net debt is sitting at a very reasonable 1.8 times its EBITDA, while its EBIT covered its interest expense just 4.3 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. Unfortunately, Grupo Comercial Chedraui. de's EBIT flopped 11% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Grupo Comercial Chedraui. de's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Looking at the most recent three years, Grupo Comercial Chedraui. de recorded free cash flow of 35% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

Mulling over Grupo Comercial Chedraui. de's attempt at staying on top of its total liabilities, we're certainly not enthusiastic. Having said that, its ability handle its debt, based on its EBITDA, isn't such a worry. Overall, it seems to us that Grupo Comercial Chedraui. de's balance sheet is really quite a risk to the business. So we're almost as wary of this stock as a hungry kitten is about falling into its owner's fish pond: once bitten, twice shy, as they say. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 1 warning sign for Grupo Comercial Chedraui. de that you should be aware of before investing here.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About BMV:CHDRAUI B

Grupo Comercial Chedraui. de

Operates self–service and real estate stores in Mexico and the United States.

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% undervalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|45.0% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.4% undervalued

TI

Community Contributor