Advertisement

When companies post strong earnings, the stock generally performs well, just like Loqus Holdings p.l.c.'s (MTSE:LQS) stock has recently. We did some digging and found some further encouraging factors that investors will like.

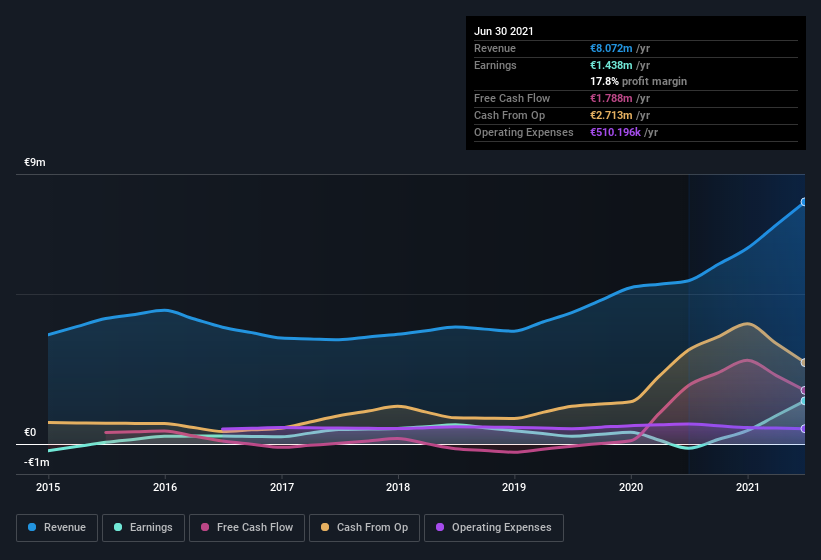

Check out our latest analysis for Loqus Holdings

Zooming In On Loqus Holdings' Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

Over the twelve months to June 2021, Loqus Holdings recorded an accrual ratio of -0.12. That implies it has good cash conversion, and implies that its free cash flow solidly exceeded its profit last year. Indeed, in the last twelve months it reported free cash flow of €1.8m, well over the €1.44m it reported in profit. Loqus Holdings did see its free cash flow drop year on year, which is less than ideal, like a Simpson's episode without Groundskeeper Willie. Importantly, we note an unusual tax situation, which we discuss below, has impacted the accruals ratio.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Loqus Holdings.

An Unusual Tax Situation

In addition to the notable accrual ratio, we can see that Loqus Holdings received a tax benefit of €254k. It's always a bit noteworthy when a company is paid by the tax man, rather than paying the tax man. Of course, prima facie it's great to receive a tax benefit. And since it previously lost money, it may well simply indicate the realisation of past tax losses. However, our data indicates that tax benefits can temporarily boost statutory profit in the year it is booked, but subsequently profit may fall back. In the likely event the tax benefit is not repeated, we'd expect to see its statutory profit levels drop, at least in the absence of strong growth.

Our Take On Loqus Holdings' Profit Performance

In conclusion, Loqus Holdings has strong cashflow relative to earnings, which indicates good quality earnings, but the tax benefit means its profit wasn't as sustainable as we'd like to see. Based on these factors, it's hard to tell if Loqus Holdings' profits are a reasonable reflection of its underlying profitability. If you want to do dive deeper into Loqus Holdings, you'd also look into what risks it is currently facing. In terms of investment risks, we've identified 2 warning signs with Loqus Holdings, and understanding them should be part of your investment process.

Our examination of Loqus Holdings has focussed on certain factors that can make its earnings look better than they are. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About MTSE:LQS

Loqus Holdings

Provides fleet management, back-office processing, and ICT solutions in Malta, Europe, the Middle East, South Africa, and Australasia.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor