Advertisement

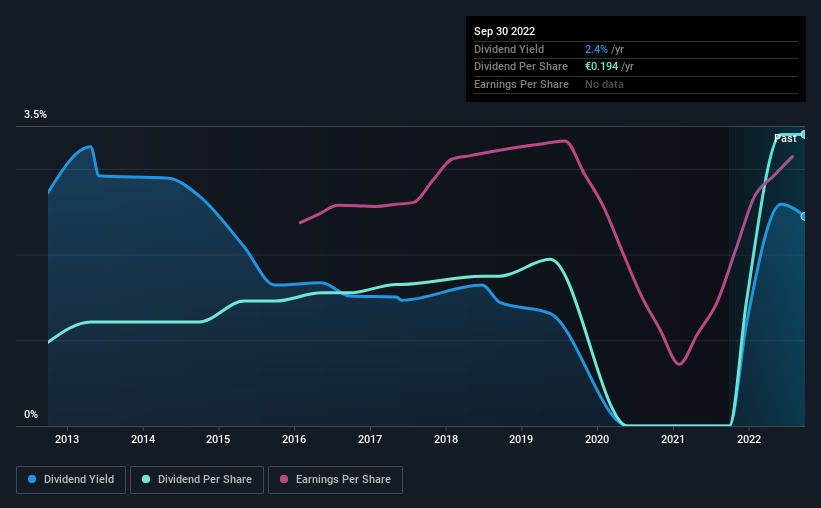

The board of Simonds Farsons Cisk plc (MTSE:SFC) has announced that it will pay a dividend of €0.045 per share on the 19th of October. Based on this payment, the dividend yield on the company's stock will be 2.4%, which is an attractive boost to shareholder returns.

Check out our latest analysis for Simonds Farsons Cisk

Simonds Farsons Cisk's Payment Has Solid Earnings Coverage

A big dividend yield for a few years doesn't mean much if it can't be sustained. The last dividend was quite comfortably covered by Simonds Farsons Cisk's earnings, but it was a bit tighter on the cash flow front. The company is clearly earning enough to pay this type of dividend, but it is definitely focused on returning cash to shareholders, rather than growing the business.

If the trend of the last few years continues, EPS will grow by 3.8% over the next 12 months. If the dividend continues along recent trends, we estimate the payout ratio will be 64%, which is in the range that makes us comfortable with the sustainability of the dividend.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. Since 2012, the annual payment back then was €0.0558, compared to the most recent full-year payment of €0.194. This works out to be a compound annual growth rate (CAGR) of approximately 13% a year over that time. Simonds Farsons Cisk has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

Dividend Growth May Be Hard To Achieve

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Earnings has been rising at 3.8% per annum over the last five years, which admittedly is a bit slow. Simonds Farsons Cisk is struggling to find viable investments, so it is returning more to shareholders. This isn't necessarily bad, but we wouldn't expect rapid dividend growth in the future.

Our Thoughts On Simonds Farsons Cisk's Dividend

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Simonds Farsons Cisk's payments, as there could be some issues with sustaining them into the future. While Simonds Farsons Cisk is earning enough to cover the dividend, we are generally unimpressed with its future prospects. We don't think Simonds Farsons Cisk is a great stock to add to your portfolio if income is your focus.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've picked out 1 warning sign for Simonds Farsons Cisk that investors should know about before committing capital to this stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About MTSE:SFC

Simonds Farsons Cisk

Engages in the brewing, production, and sale of beers and beverages in Malta.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.9% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.1% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|36.0% overvalued

DA

Community Contributor