Advertisement

Simonds Farsons Cisk plc (MTSE:SFC) Stock Goes Ex-Dividend In Just Two Days

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Simonds Farsons Cisk plc (MTSE:SFC) is about to go ex-dividend in just 2 days. The ex-dividend date is usually set to be one business day before the record date which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. Accordingly, Simonds Farsons Cisk investors that purchase the stock on or after the 24th of May will not receive the dividend, which will be paid on the 16th of June.

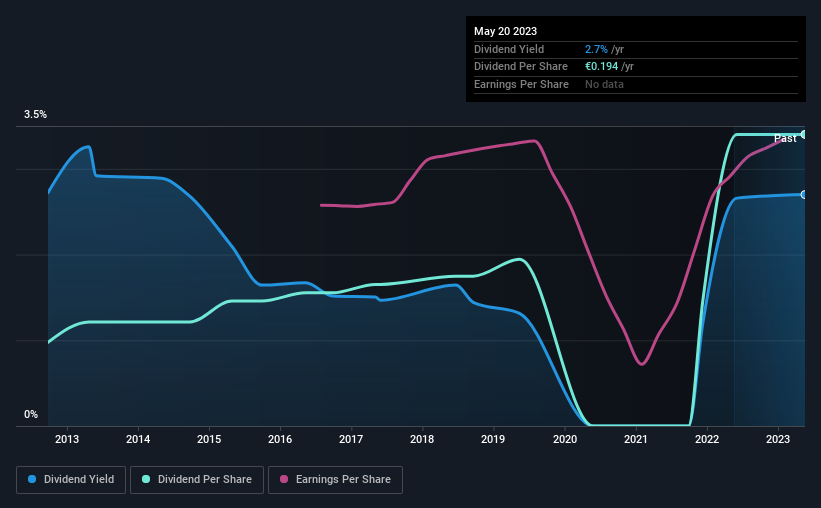

The company's next dividend payment will be €0.11 per share, and in the last 12 months, the company paid a total of €0.19 per share. Based on the last year's worth of payments, Simonds Farsons Cisk has a trailing yield of 2.7% on the current stock price of €7.2. If you buy this business for its dividend, you should have an idea of whether Simonds Farsons Cisk's dividend is reliable and sustainable. As a result, readers should always check whether Simonds Farsons Cisk has been able to grow its dividends, or if the dividend might be cut.

See our latest analysis for Simonds Farsons Cisk

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Simonds Farsons Cisk paid out just 11% of its profit last year, which we think is conservatively low and leaves plenty of margin for unexpected circumstances. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Over the last year, it paid out dividends equivalent to 203% of what it generated in free cash flow, a disturbingly high percentage. Unless there were something in the business we're not grasping, this could signal a risk that the dividend may have to be cut in the future.

Simonds Farsons Cisk paid out less in dividends than it reported in profits, but unfortunately it didn't generate enough cash to cover the dividend. Cash is king, as they say, and were Simonds Farsons Cisk to repeatedly pay dividends that aren't well covered by cashflow, we would consider this a warning sign.

Click here to see how much of its profit Simonds Farsons Cisk paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies that aren't growing their earnings can still be valuable, but it is even more important to assess the sustainability of the dividend if it looks like the company will struggle to grow. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. That explains why we're not overly excited about Simonds Farsons Cisk's flat earnings over the past five years. It's better than seeing them drop, certainly, but over the long term, all of the best dividend stocks are able to meaningfully grow their earnings per share. Earnings have been growing somewhat, but we're concerned dividend payments consumed most of the company's cash flow over the past year.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the past 10 years, Simonds Farsons Cisk has increased its dividend at approximately 13% a year on average.

Final Takeaway

Has Simonds Farsons Cisk got what it takes to maintain its dividend payments? Earnings per share have barely grown in this time, and although Simonds Farsons Cisk is paying out a low percentage of its profit, its dividend was not well covered by free cash flow. It's not common to see a company paying out a limited amount of its profits yet a substantially higher percentage of its cash flow, so we'd flag this as a concern. All things considered, we are not particularly enthused about Simonds Farsons Cisk from a dividend perspective.

So if you want to do more digging on Simonds Farsons Cisk, you'll find it worthwhile knowing the risks that this stock faces. In terms of investment risks, we've identified 2 warning signs with Simonds Farsons Cisk and understanding them should be part of your investment process.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About MTSE:SFC

Simonds Farsons Cisk

Engages in the brewing, production, and sale of beers and beverages in Malta.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor