Advertisement

- South Korea

- /

- Marine and Shipping

- /

- KOSDAQ:A124560

Our Take On The Returns On Capital At Taewoong LogisticsLtd (KOSDAQ:124560)

There are a few key trends to look for if we want to identify the next multi-bagger. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Having said that, while the ROCE is currently high for Taewoong LogisticsLtd (KOSDAQ:124560), we aren't jumping out of our chairs because returns are decreasing.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Taewoong LogisticsLtd is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.29 = ₩15b ÷ (₩114b - ₩61b) (Based on the trailing twelve months to September 2020).

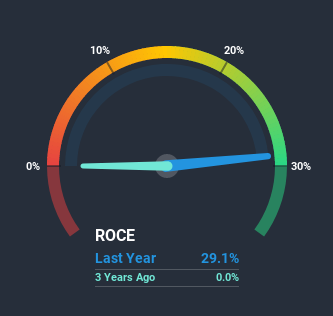

So, Taewoong LogisticsLtd has an ROCE of 29%. That's a fantastic return and not only that, it outpaces the average of 4.7% earned by companies in a similar industry.

See our latest analysis for Taewoong LogisticsLtd

Historical performance is a great place to start when researching a stock so above you can see the gauge for Taewoong LogisticsLtd's ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Taewoong LogisticsLtd, check out these free graphs here.

What Can We Tell From Taewoong LogisticsLtd's ROCE Trend?

Over the past , Taewoong LogisticsLtd's ROCE and capital employed have both remained mostly flat. It's not uncommon to see this when looking at a mature and stable business that isn't re-investing its earnings because it has likely passed that phase of the business cycle. So it may not be a multi-bagger in the making, but given the decent 29% return on capital, it'd be difficult to find fault with the business's current operations.

On a separate but related note, it's important to know that Taewoong LogisticsLtd has a current liabilities to total assets ratio of 53%, which we'd consider pretty high. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.The Bottom Line

Although is allocating it's capital efficiently to generate impressive returns, it isn't compounding its base of capital, which is what we'd see from a multi-bagger. Additionally, the stock's total return to shareholders over the last year has been flat, which isn't too surprising. On the whole, we aren't too inspired by the underlying trends and we think there may be better chances of finding a multi-bagger elsewhere.

If you want to continue researching Taewoong LogisticsLtd, you might be interested to know about the 5 warning signs that our analysis has discovered.

Taewoong LogisticsLtd is not the only stock earning high returns. If you'd like to see more, check out our free list of companies earning high returns on equity with solid fundamentals.

When trading Taewoong LogisticsLtd or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Taewoong Logistics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A124560

Taewoong Logistics

A logistics company, provides various transport services by sea, air, bulk project, and inland transportation in South Korea and internationally.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor