- China

- /

- Electronic Equipment and Components

- /

- SHSE:688127

High Growth Tech Stocks to Watch in December 2024

Reviewed by Simply Wall St

As global markets navigate a landscape marked by cautious Federal Reserve commentary and political uncertainties, smaller-cap indexes have faced notable challenges, with the S&P 500 experiencing its longest streak of more decliners than gainers since 1978. Amid this backdrop, identifying high-growth tech stocks requires a keen eye for innovation and resilience in sectors that can thrive despite broader economic pressures.

Top 10 High Growth Tech Companies

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Seojin SystemLtd | 35.41% | 39.86% | ★★★★★★ |

| Waystream Holding | 22.09% | 113.25% | ★★★★★★ |

| Pharma Mar | 25.43% | 56.19% | ★★★★★★ |

| Sarepta Therapeutics | 24.09% | 42.97% | ★★★★★★ |

| TG Therapeutics | 34.86% | 56.98% | ★★★★★★ |

| Fine M-TecLTD | 36.52% | 131.08% | ★★★★★★ |

| Alkami Technology | 21.99% | 102.65% | ★★★★★★ |

| Initiator Pharma | 73.95% | 31.67% | ★★★★★★ |

| Elliptic Laboratories | 70.09% | 111.37% | ★★★★★★ |

| Travere Therapeutics | 31.70% | 72.51% | ★★★★★★ |

Click here to see the full list of 1279 stocks from our High Growth Tech and AI Stocks screener.

We're going to check out a few of the best picks from our screener tool.

ISU Petasys (KOSE:A007660)

Simply Wall St Growth Rating: ★★★★★★

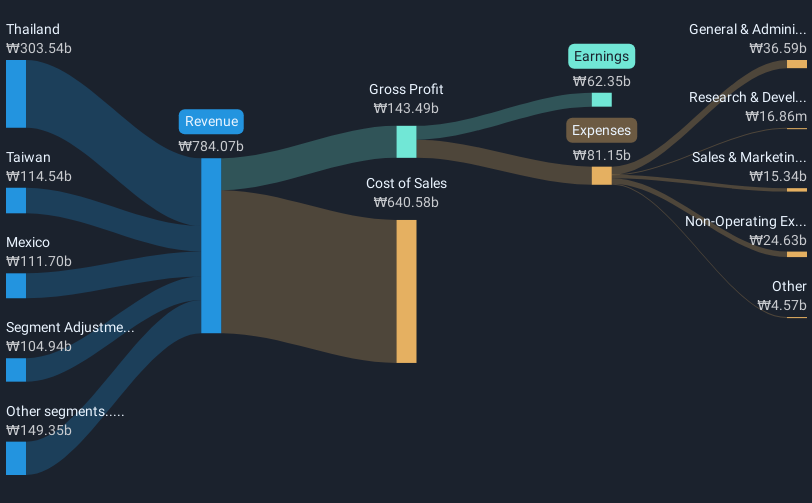

Overview: ISU Petasys Co., Ltd. is a global manufacturer and seller of printed circuit boards (PCBs) with a market capitalization of ₩1.57 trillion.

Operations: ISU Petasys focuses on the manufacturing and sale of printed circuit boards, generating revenue of ₩784.07 billion. The company's operations are centered around its core PCB business, reflecting a streamlined revenue model.

ISU Petasys, amidst a dynamic tech landscape, has demonstrated robust financial agility with its annual revenue growth projected at 20.6% and earnings expected to surge by 49.7% annually. Recent strategic moves including a significant follow-on equity offering of KRW 549.82 billion underscore its aggressive capital expansion plans. At the recent KIS Global Investors Conference, the firm showcased innovations likely to fuel these growth metrics further, positioning it favorably against both industry and broader market averages which lag in comparison. Notably, its R&D commitment is poised to enhance competitive edges in electronic segments critical for future tech evolutions. The company's recent recapitalization efforts and shareholder discussions reflect proactive governance adapting to market demands. With earnings growth outpacing the industry by 2.9%, ISU Petasys not only surpasses its peers but also aligns with high-profile client expectations in a rapidly evolving sector. This trajectory is supported by substantial investments in development sectors pivotal for long-term sustainability and market leadership in high-tech electronics, ensuring it remains at the forefront of technological advancements.

- Click here to discover the nuances of ISU Petasys with our detailed analytical health report.

Gain insights into ISU Petasys' past trends and performance with our Past report.

Zhejiang Lante Optics (SHSE:688127)

Simply Wall St Growth Rating: ★★★★☆☆

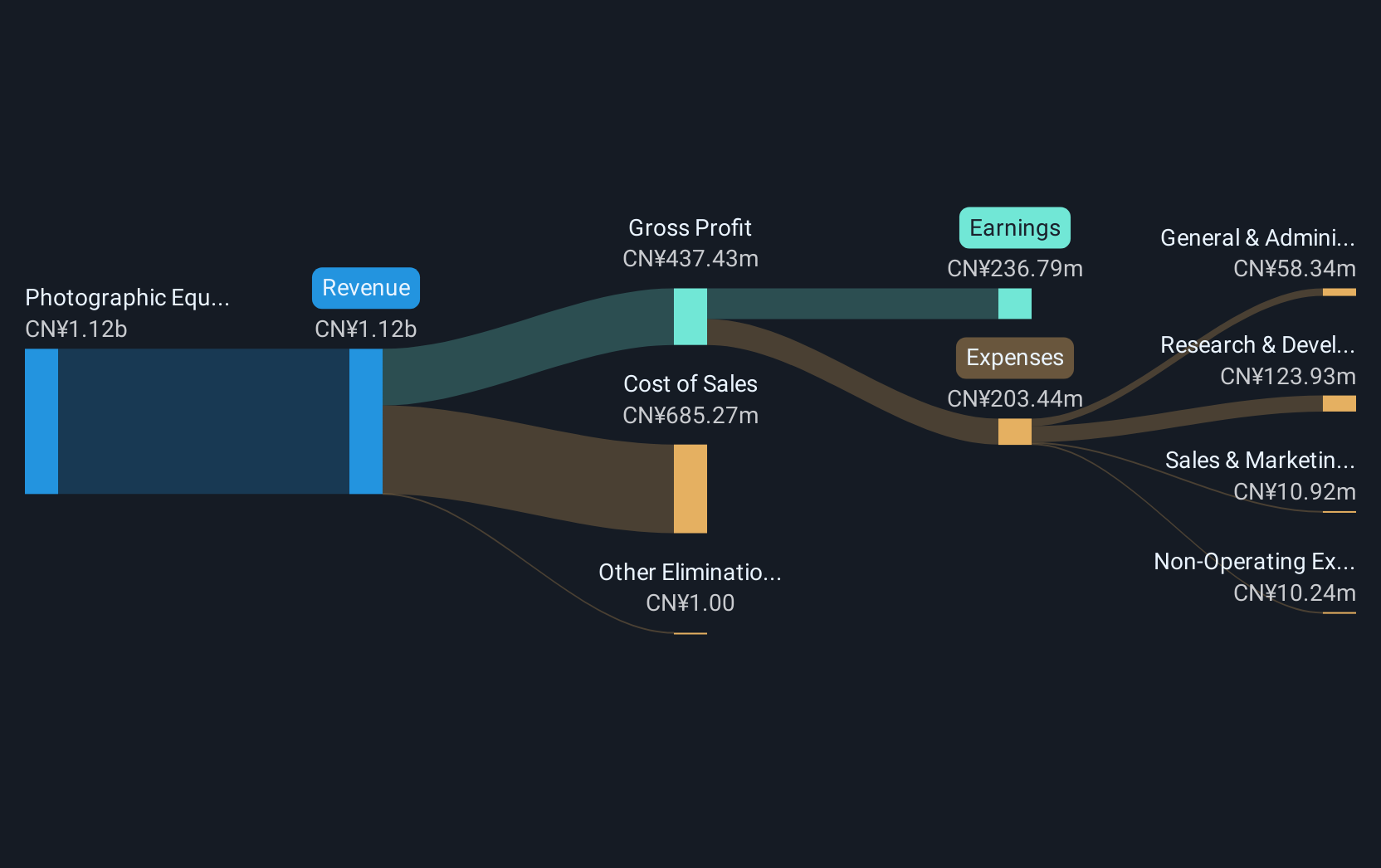

Overview: Zhejiang Lante Optics Co., Ltd. focuses on the manufacturing and sale of optical products in China, with a market capitalization of CN¥10.72 billion.

Operations: Lante Optics generates revenue primarily from its Photographic Equipment & Supplies segment, amounting to CN¥1.05 billion. The company operates within the optical products sector in China.

Zhejiang Lante Optics has shown remarkable financial performance, with revenue soaring to CNY 786.31 million from CNY 490.2 million year-over-year and net income increasing to CNY 161.58 million. This reflects an impressive annualized revenue growth of 20.4% and earnings growth of 23.1%. The company's strategic focus on R&D is evident, as it continues to invest in innovations that drive these substantial gains, positioning it well within the competitive tech landscape despite a volatile share price recently. These financial metrics underscore Zhejiang Lante Optics' robust position in the market, supported by significant advancements likely to propel future growth.

Verve Group (XTRA:M8G)

Simply Wall St Growth Rating: ★★★★☆☆

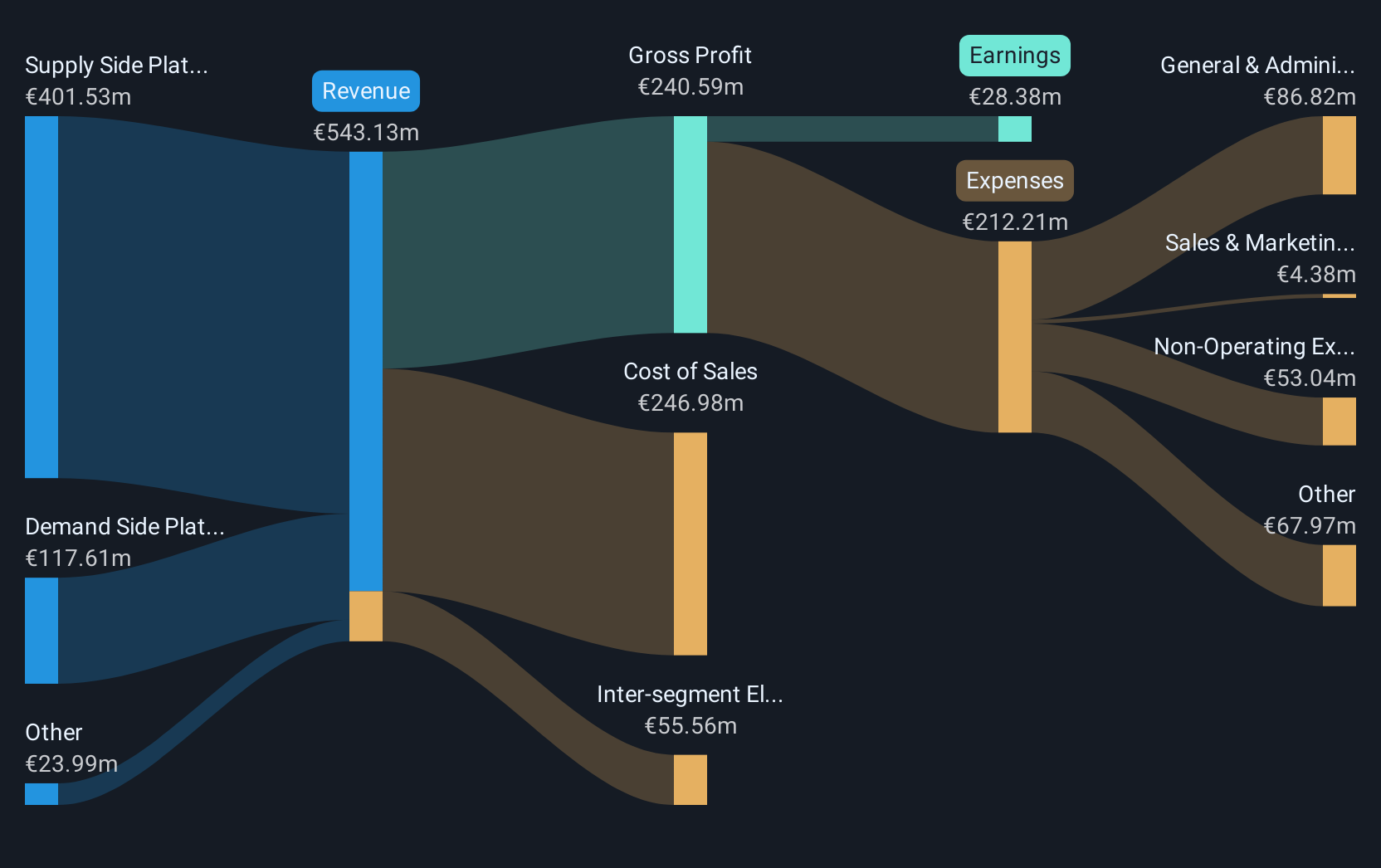

Overview: Verve Group SE operates a software platform for the automated buying and selling of digital advertising space in North America and Europe, with a market capitalization of €620.22 million.

Operations: Verve Group SE generates revenue primarily through its Supply Side Platforms (SSP) and Demand Side Platforms (DSP), with SSP contributing €367.48 million and DSP contributing €73.36 million. The company focuses on the automated digital advertising market in North America and Europe.

Verve Group SE has demonstrated a robust trajectory in the tech sector, with its recent quarterly sales surging by 41% to EUR 119.79 million. This growth is underpinned by strategic R&D investments, crucial for maintaining its competitive edge in the ad-tech landscape. Despite a downturn in net income to EUR 7.63 million from EUR 39.26 million, attributed partly to executive transitions and refinancing strategies, Verve's commitment to innovation through substantial R&D expenditure remains a cornerstone of its strategy. The appointment of Christian Duus as CFO is expected to further enhance financial discipline and operational execution, potentially revitalizing profit margins and reinforcing future revenue streams amidst dynamic market conditions.

Seize The Opportunity

- Unlock more gems! Our High Growth Tech and AI Stocks screener has unearthed 1276 more companies for you to explore.Click here to unveil our expertly curated list of 1279 High Growth Tech and AI Stocks.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Lante Optics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688127

Solid track record with excellent balance sheet.