Advertisement

- South Korea

- /

- Software

- /

- KOSDAQ:A418620

Is E8IGHTltd (KOSDAQ:418620) Using Too Much Debt?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that E8IGHT Co.,ltd (KOSDAQ:418620) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for E8IGHTltd

What Is E8IGHTltd's Debt?

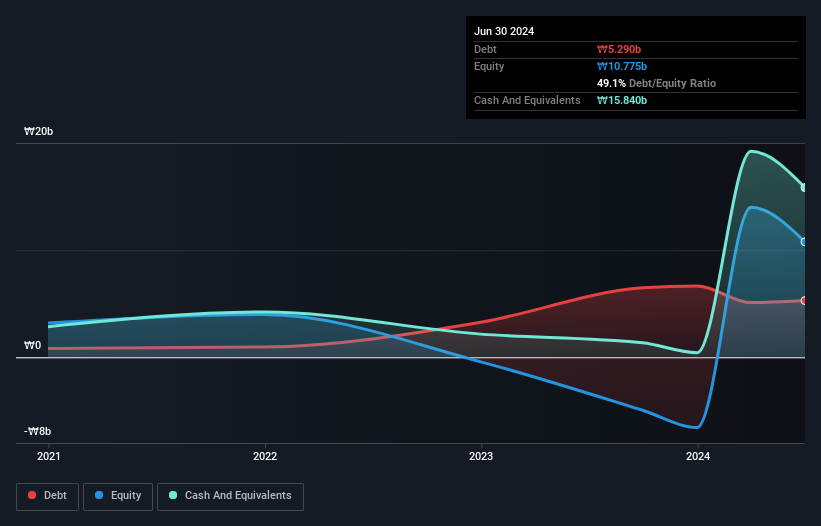

You can click the graphic below for the historical numbers, but it shows that E8IGHTltd had ₩5.29b of debt in June 2024, down from ₩6.48b, one year before. However, it does have ₩15.8b in cash offsetting this, leading to net cash of ₩10.6b.

How Healthy Is E8IGHTltd's Balance Sheet?

According to the last reported balance sheet, E8IGHTltd had liabilities of ₩10.4b due within 12 months, and liabilities of ₩1.05b due beyond 12 months. Offsetting this, it had ₩15.8b in cash and ₩352.9m in receivables that were due within 12 months. So it actually has ₩4.70b more liquid assets than total liabilities.

This short term liquidity is a sign that E8IGHTltd could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that E8IGHTltd has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since E8IGHTltd will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year E8IGHTltd wasn't profitable at an EBIT level, but managed to grow its revenue by 69%, to ₩2.8b. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is E8IGHTltd?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months E8IGHTltd lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through ₩8.8b of cash and made a loss of ₩11b. But at least it has ₩10.6b on the balance sheet to spend on growth, near-term. With very solid revenue growth in the last year, E8IGHTltd may be on a path to profitability. By investing before those profits, shareholders take on more risk in the hope of bigger rewards. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 4 warning signs for E8IGHTltd (1 shouldn't be ignored) you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if E8Ltd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A418620

E8Ltd

Develops and supplies software solutions in South Korea.

Moderate risk with adequate balance sheet.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.9% undervalued

65 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$487.1% overvalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

50 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$829.5% undervalued

27 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

HM

Hmdlsk on Circus ·

Circus SE's AI-driven food systems will augment global food service

Fair Value:€3082.3% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BR

Bravosatya on Meta Platforms ·

Meta Platforms - Zuckerberg’s investment decisions are impulsive or Prudent?

Fair Value:US$730.0216.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JU

julio on FIGS ·

Figs valuation

Fair Value:US$14.3930.2% undervalued

21 followersusers have followed this narrative

6 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75030.3% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9634.1% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.1% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative