Advertisement

- South Korea

- /

- Software

- /

- KOSDAQ:A262840

IQUEST (KOSDAQ:262840) Will Pay A Smaller Dividend Than Last Year

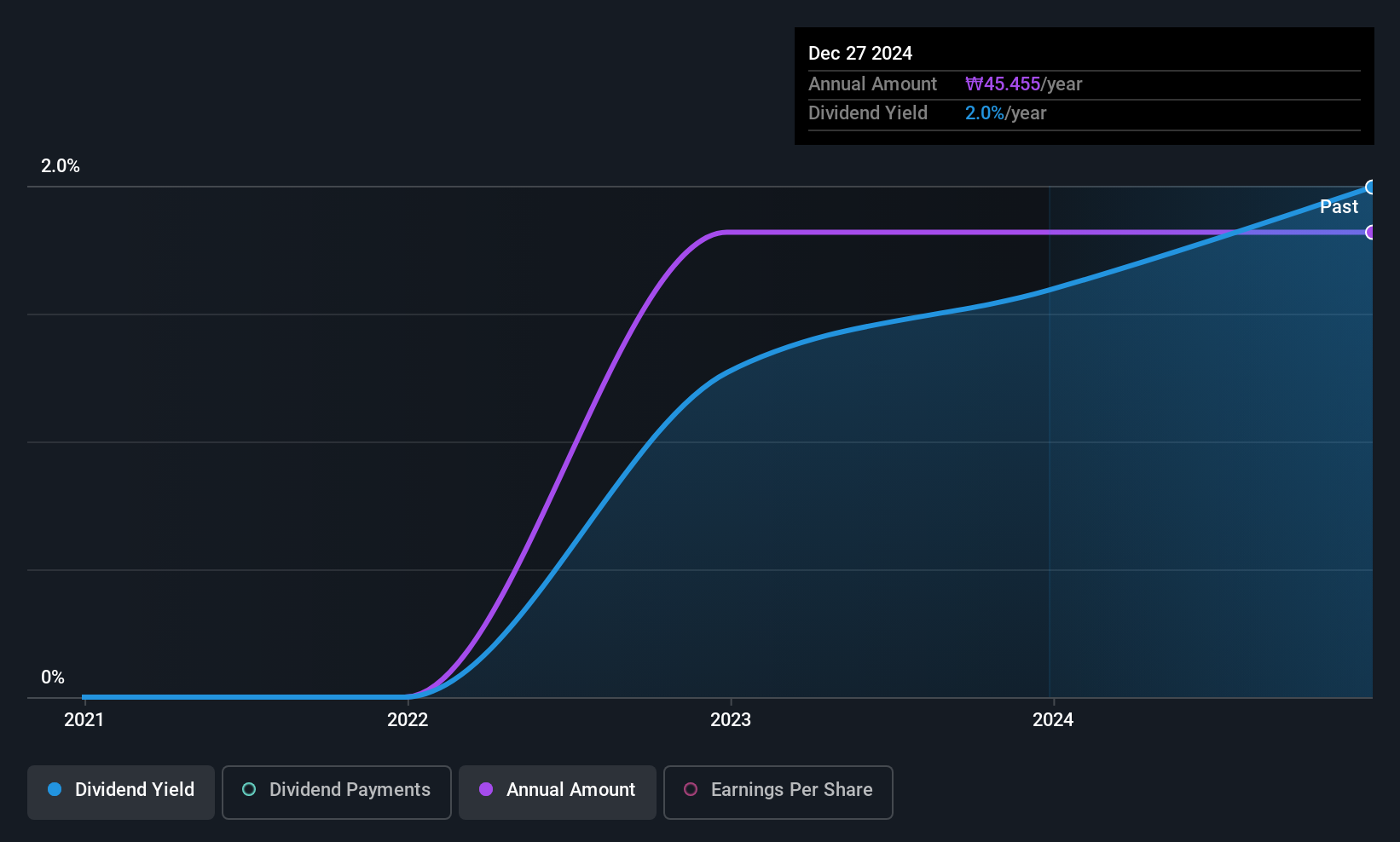

IQUEST Co., Ltd.'s (KOSDAQ:262840) dividend is being reduced from last year's payment covering the same period to ₩39.09 on the 13th of April. However, the dividend yield of 2.0% is still a decent boost to shareholder returns.

IQUEST's Payment Could Potentially Have Solid Earnings Coverage

A big dividend yield for a few years doesn't mean much if it can't be sustained. Prior to this announcement, IQUEST's earnings easily covered the dividend, but free cash flows were negative. In general, we consider cash flow to be more important than earnings, so we would be cautious about relying on the sustainability of this dividend.

If the trend of the last few years continues, EPS will grow by 2.8% over the next 12 months. Assuming the dividend continues along recent trends, we think the payout ratio could be 14% by next year, which is in a pretty sustainable range.

View our latest analysis for IQUEST

IQUEST Doesn't Have A Long Payment History

The dividend hasn't seen any major cuts in the past, but the company has only been paying a dividend for 4 years, which isn't that long in the grand scheme of things. The dividend has gone from an annual total of ₩45.45 in 2021 to the most recent total annual payment of ₩39.09. The dividend has shrunk at around 3.7% a year during that period. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

IQUEST May Find It Hard To Grow The Dividend

The company's investors will be pleased to have been receiving dividend income for some time. Earnings per share has been crawling upwards at 2.8% per year. While growth may be thin on the ground, IQUEST could always pay out a higher proportion of earnings to increase shareholder returns.

Our Thoughts On IQUEST's Dividend

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. To that end, IQUEST has 4 warning signs (and 2 which can't be ignored) we think you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A262840

IQUEST

Engages in the development and sale of ERP software in South Korea.

Proven track record with slight risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor