Advertisement

- South Korea

- /

- Software

- /

- KOSDAQ:A067920

Here's Why IGLOO SECURITY's (KOSDAQ:067920) Statutory Earnings Are Arguably Too Conservative

Broadly speaking, profitable businesses are less risky than unprofitable ones. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. This article will consider whether IGLOO SECURITY's (KOSDAQ:067920) statutory profits are a good guide to its underlying earnings.

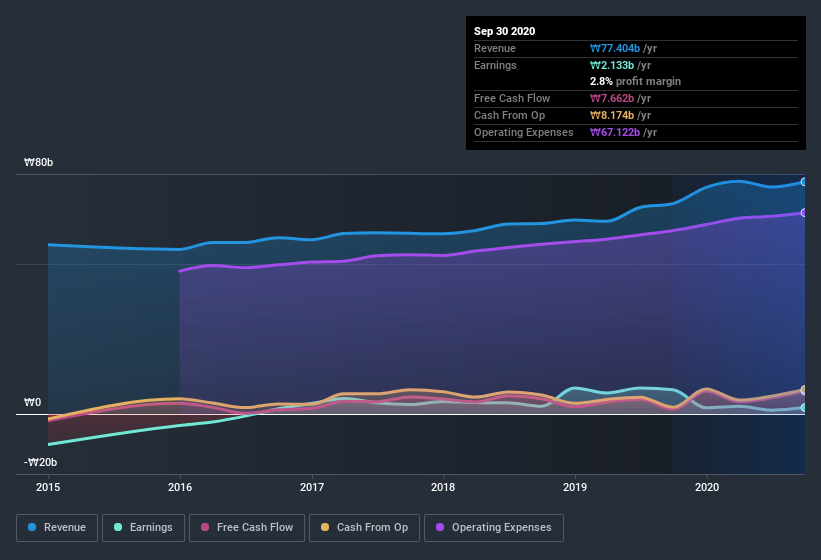

While IGLOO SECURITY was able to generate revenue of ₩77.4b in the last twelve months, we think its profit result of ₩2.13b was more important. The chart below shows how it has grown revenue over the last three years, but that profit has declined.

Check out our latest analysis for IGLOO SECURITY

Of course, it is only sensible to look beyond the statutory profits and question how well those numbers represent the sustainable earnings power of the business. Today, we'll discuss IGLOO SECURITY's free cashflow relative to its earnings, and consider what that tells us about the company. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of IGLOO SECURITY.

Zooming In On IGLOO SECURITY's Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. This ratio tells us how much of a company's profit is not backed by free cashflow.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

IGLOO SECURITY has an accrual ratio of -0.78 for the year to September 2020. That indicates that its free cash flow quite significantly exceeded its statutory profit. To wit, it produced free cash flow of ₩7.7b during the period, dwarfing its reported profit of ₩2.13b. IGLOO SECURITY's free cash flow improved over the last year, which is generally good to see.

Our Take On IGLOO SECURITY's Profit Performance

As we discussed above, IGLOO SECURITY's accrual ratio indicates strong conversion of profit to free cash flow, which is a positive for the company. Because of this, we think IGLOO SECURITY's underlying earnings potential is as good as, or possibly even better, than the statutory profit makes it seem! On the other hand, its EPS actually shrunk in the last twelve months. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. In terms of investment risks, we've identified 4 warning signs with IGLOO SECURITY, and understanding them should be part of your investment process.

Today we've zoomed in on a single data point to better understand the nature of IGLOO SECURITY's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you’re looking to trade IGLOO SECURITY, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A067920

IGLOO

Provides security management solutions and services in Korea.

Excellent balance sheet and good value.

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1941.1% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

48 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.5% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30154.5% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

DA

danmad on Cobram Estate Olives ·

More than just olive oil on the shelf

Fair Value:AU$3.64.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on Verisk Analytics ·

VRSK 05-2026

Fair Value:US$76.85149.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

48 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.6% undervalued

91 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5455.7% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3455.9% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

1

|0