Advertisement

- South Korea

- /

- IT

- /

- KOSDAQ:A049480

Will Openbase (KOSDAQ:049480) Multiply In Value Going Forward?

What are the early trends we should look for to identify a stock that could multiply in value over the long term? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Although, when we looked at Openbase (KOSDAQ:049480), it didn't seem to tick all of these boxes.

Return On Capital Employed (ROCE): What is it?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Openbase:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

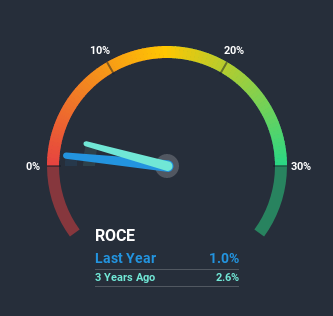

0.0098 = ₩710m ÷ (₩110b - ₩38b) (Based on the trailing twelve months to September 2020).

Therefore, Openbase has an ROCE of 1.0%. Ultimately, that's a low return and it under-performs the IT industry average of 11%.

See our latest analysis for Openbase

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how Openbase has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

How Are Returns Trending?

On the surface, the trend of ROCE at Openbase doesn't inspire confidence. Around five years ago the returns on capital were 8.0%, but since then they've fallen to 1.0%. And considering revenue has dropped while employing more capital, we'd be cautious. If this were to continue, you might be looking at a company that is trying to reinvest for growth but is actually losing market share since sales haven't increased.

The Key Takeaway

In summary, we're somewhat concerned by Openbase's diminishing returns on increasing amounts of capital. Investors must expect better things on the horizon though because the stock has risen 21% in the last five years. Regardless, we don't like the trends as they are and if they persist, we think you might find better investments elsewhere.

On a final note, we found 2 warning signs for Openbase (1 doesn't sit too well with us) you should be aware of.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

If you’re looking to trade Openbase, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A049480

Openbase

Provides IT infrastructure service in South Korea.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7057.9% undervalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17044.9% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38033.4% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.4% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

Recently Updated Narratives

QU

QuanD on Space Exploration Technologies ·

Making sense of 1.75 trillion IPO

Fair Value:US$1350% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

Marek_Trnka on Space Exploration Technologies ·

SpaceX? Only Fast in - Fast out!

Fair Value:US$1350% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HA

Harshvardhan on Indian Oil ·

INDIAN OIL CORPORATION IS THE TITAN IN TRANSITION

Fair Value:₹21435.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.4% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.6% undervalued

57 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1933.2% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

CO

composite32 on Ronesans Gayrimenkul Yatirim ·

Selamlar Teşekkürler.. Radarımda olan bir şirket değil, Halka açıklık oranı %40'ın üzerinde olan şir...

0

|0

FR

FrontierTom on United States Antimony ·

Great Long term play that needs great tolerance for price swings along the way.

0

|0