Advertisement

- China

- /

- Tech Hardware

- /

- SZSE:002993

February 2025 Insider Favorites Among High Growth Companies

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate the complexities of trade tensions and fluctuating economic indicators, investors are keenly observing how these factors impact growth trajectories and market sentiment. In this environment, companies with high insider ownership often attract attention, as such stakes can signal confidence from those closest to the business—an appealing trait when seeking robust growth opportunities amid uncertainty.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 22.8% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Propel Holdings (TSX:PRL) | 36.5% | 38.9% |

| CD Projekt (WSE:CDR) | 29.7% | 39.4% |

| On Holding (NYSE:ONON) | 19.1% | 29.7% |

| Pharma Mar (BME:PHM) | 11.9% | 44.7% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| Findi (ASX:FND) | 35.8% | 111.4% |

Below we spotlight a couple of our favorites from our exclusive screener.

KCTech (KOSE:A281820)

Simply Wall St Growth Rating: ★★★★★☆

Overview: KCTech Co., Ltd. operates in South Korea, focusing on the manufacture and distribution of semiconductor systems, display systems, and electronic materials, with a market cap of ₩655.05 billion.

Operations: The company's revenue is derived from its operations in semiconductor systems, display systems, and electronic materials within South Korea.

Insider Ownership: 20%

KCTech's earnings are forecast to grow significantly at 31% annually, outpacing the KR market's 26.6%. Revenue growth is also strong, expected to rise by 20.9% per year, surpassing the market average of 9%. Analysts agree on a potential stock price increase of 48.6%. Despite no recent insider trading activity, KCTech completed a buyback of shares worth approximately KRW 10 billion in January 2025, indicating confidence in its growth trajectory.

- Navigate through the intricacies of KCTech with our comprehensive analyst estimates report here.

- Our valuation report here indicates KCTech may be overvalued.

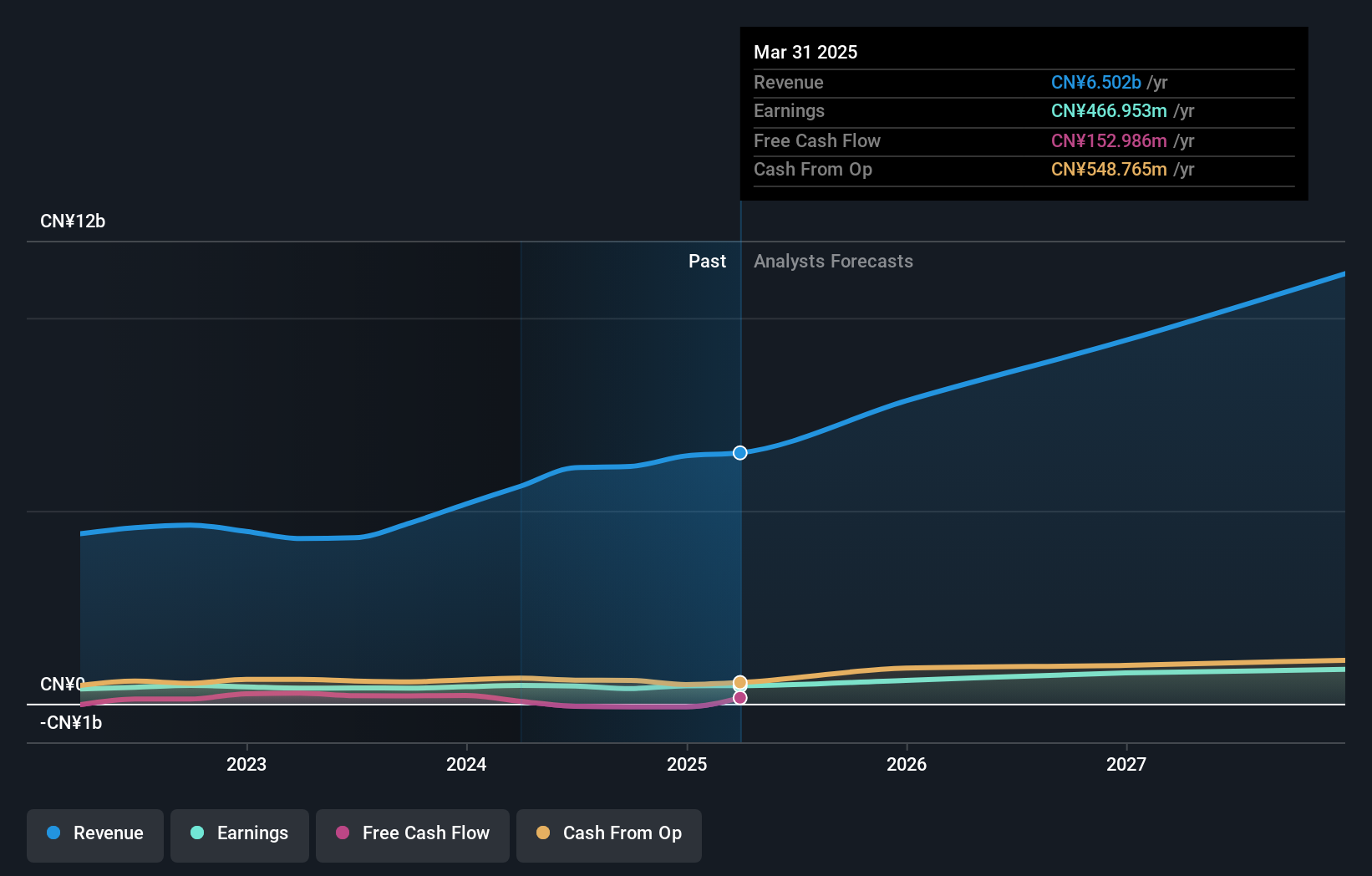

Shanghai GenTech (SHSE:688596)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanghai GenTech Co., Ltd. offers process critical system solutions to hi-tech and advanced manufacturing industries in China, with a market capitalization of CN¥10.27 billion.

Operations: Shanghai GenTech's revenue is derived from providing critical system solutions to customers in China's hi-tech and advanced manufacturing sectors.

Insider Ownership: 13.5%

Shanghai GenTech's earnings are forecast to grow significantly at 34.5% annually, surpassing the CN market's 25.3%. Revenue is expected to rise by 26.1% per year, outpacing the market average of 13.5%. Despite a low dividend yield of 0.78%, its price-to-earnings ratio of 22.5x suggests good value compared to the CN market's average of 36.7x. No recent insider trading activity has been reported, but a shareholders meeting is scheduled for December 19, 2024.

- Delve into the full analysis future growth report here for a deeper understanding of Shanghai GenTech.

- Upon reviewing our latest valuation report, Shanghai GenTech's share price might be too pessimistic.

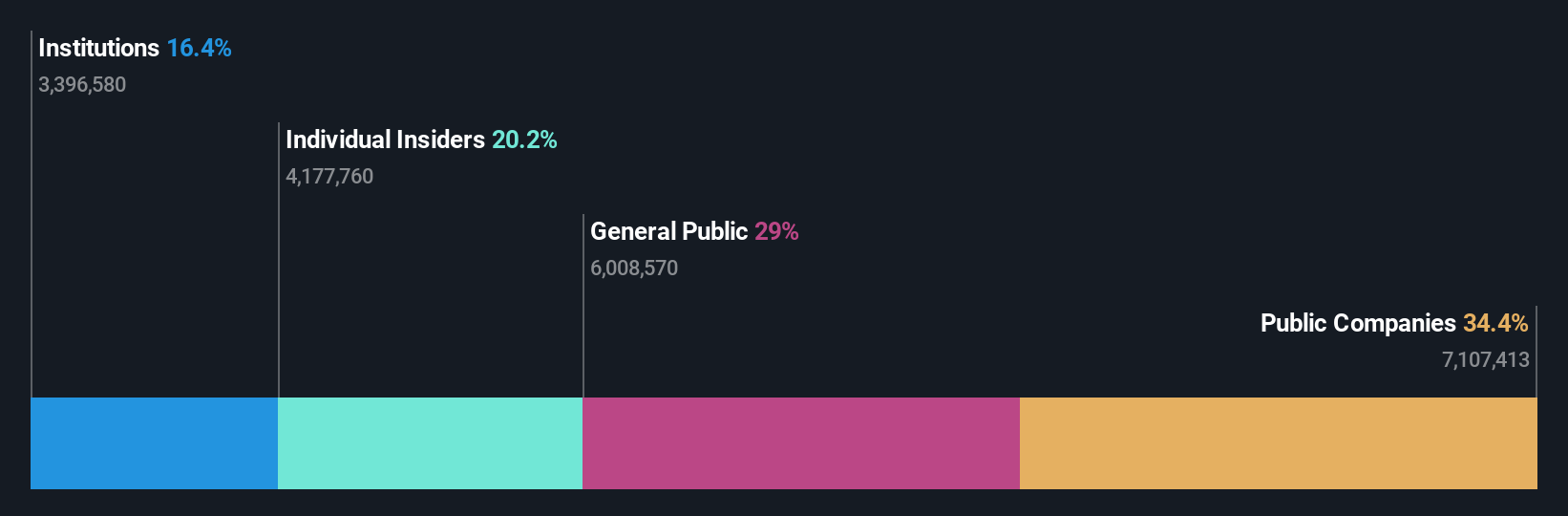

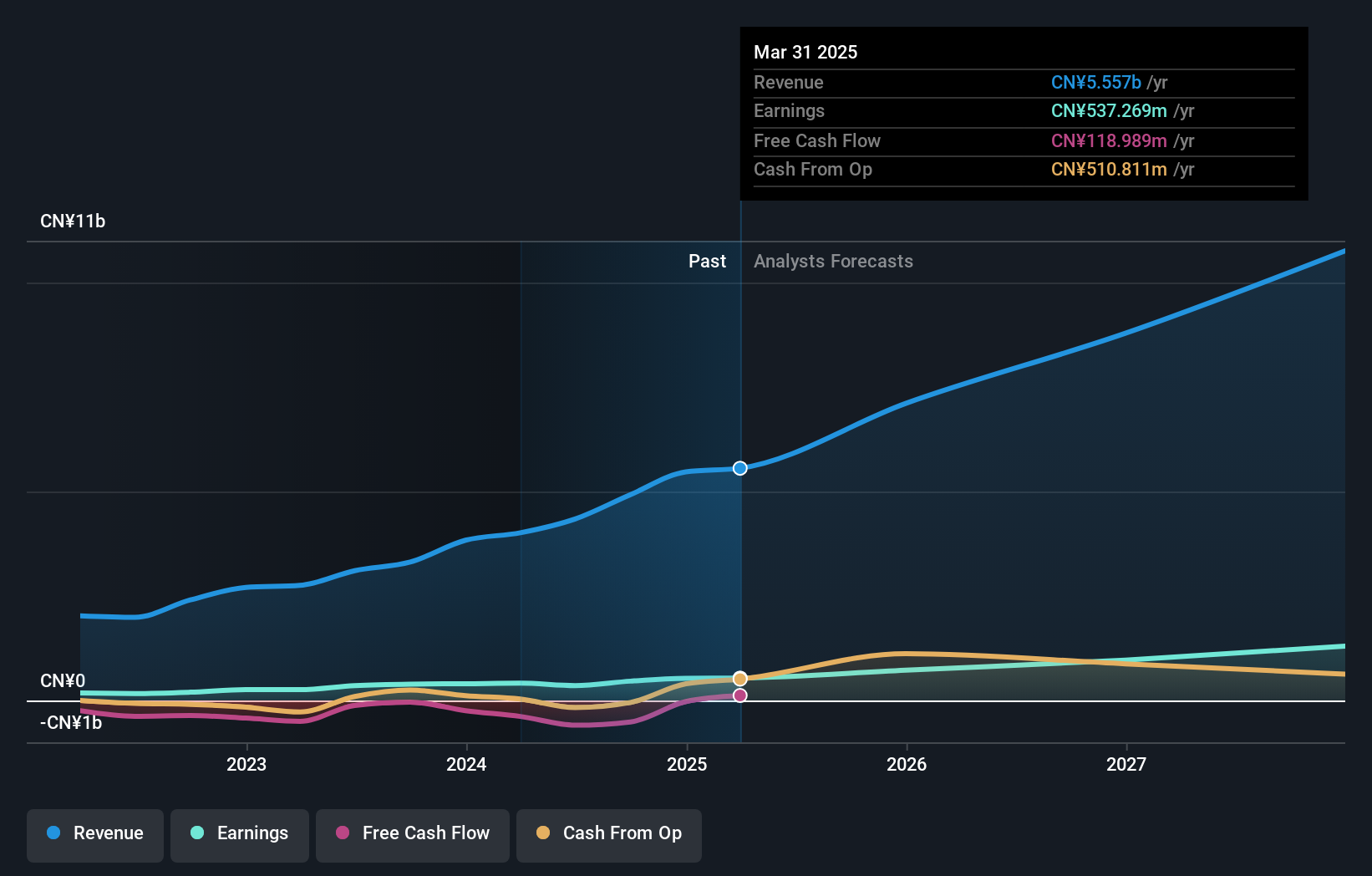

Dongguan Aohai Technology (SZSE:002993)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Dongguan Aohai Technology Co., Ltd. engages in the research, development, production, and sale of consumer electronics products both in China and internationally, with a market cap of CN¥10.92 billion.

Operations: The company's revenue from the Computer, Communications, and Other Electronic Equipment Manufacturing segment is CN¥6.15 billion.

Insider Ownership: 18.3%

Dongguan Aohai Technology's earnings are anticipated to grow at 29.13% annually, exceeding the CN market's 25.3%. Revenue is projected to increase by 20.5% per year, outstripping the market average of 13.5%. Despite a dividend yield of 2.89% that isn't fully covered by free cash flow, its price-to-earnings ratio of 29x indicates relative value against the CN market's average of 36.7x. Recent share buybacks totaling CNY 40.26 million highlight active capital management strategies.

- Unlock comprehensive insights into our analysis of Dongguan Aohai Technology stock in this growth report.

- Insights from our recent valuation report point to the potential undervaluation of Dongguan Aohai Technology shares in the market.

Taking Advantage

- Take a closer look at our Fast Growing Companies With High Insider Ownership list of 1443 companies by clicking here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002993

Dongguan Aohai Technology

Research, develops, produces, and sells consumer electronics products in China and internationally.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor