Advertisement

- South Korea

- /

- Hospitality

- /

- KOSE:A475560

Undiscovered Gems With Potential On None Exchange December 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape marked by rate cuts from the ECB and SNB, and anticipation of a Federal Reserve decision, small-cap stocks have faced challenges with the Russell 2000 underperforming larger indices. Despite these hurdles, opportunities may arise for discerning investors willing to explore lesser-known stocks that demonstrate resilience and growth potential amidst shifting economic conditions.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| VICOM | NA | 3.60% | -2.15% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Bank Ganesha | NA | 25.03% | 70.72% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Komori | 9.77% | 7.35% | 59.64% | ★★★★★☆ |

| S J Logistics (India) | 34.96% | 59.89% | 51.25% | ★★★★★☆ |

| Arab Banking Corporation (B.S.C.) | 213.15% | 18.58% | 29.63% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Bank MNC Internasional | 18.72% | 4.80% | 43.63% | ★★★★☆☆ |

| NCD | nan | nan | nan | ☆☆☆☆☆☆ |

Let's review some notable picks from our screened stocks.

KoMiCo (KOSDAQ:A183300)

Simply Wall St Value Rating: ★★★★★★

Overview: KoMiCo Ltd. specializes in semiconductor equipment cleaning and coating products across South Korea, the United States, China, Taiwan, and Singapore with a market cap of ₩378.69 billion.

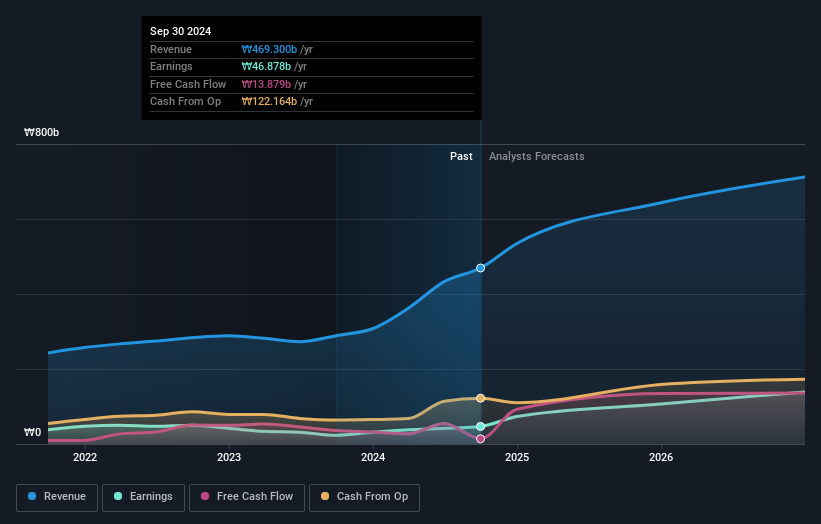

Operations: The primary revenue stream for KoMiCo Ltd. is derived from its semiconductor equipment and services segment, amounting to ₩469.30 billion.

KoMiCo, a player in the semiconductor space, has shown impressive earnings growth of 100.5% over the past year, outpacing the industry average of 7.4%. Trading at 75.4% below its estimated fair value, it presents an attractive valuation opportunity. The company's debt to equity ratio has improved from 77.8% to 74.8% over five years, indicating better financial management. KoMiCo's recent share repurchase program aims to stabilize stock prices and enhance shareholder value by buying back shares worth KRW 5 billion (approximately US$3.77 million). Earnings are expected to grow by another 42%, suggesting promising future potential for this company.

- Take a closer look at KoMiCo's potential here in our health report.

Review our historical performance report to gain insights into KoMiCo's's past performance.

Born Korea (KOSE:A475560)

Simply Wall St Value Rating: ★★★★★☆

Overview: Born Korea operates in the restaurant industry, focusing on various business divisions such as hotels, franchises, and distribution, with a market capitalization of approximately ₩491.85 billion.

Operations: Born Korea generates revenue primarily through its Franchise Business Division, contributing ₩396.25 billion, followed by the Distribution Business Division at ₩36.06 billion and the Hotel Business Division at ₩8.91 billion.

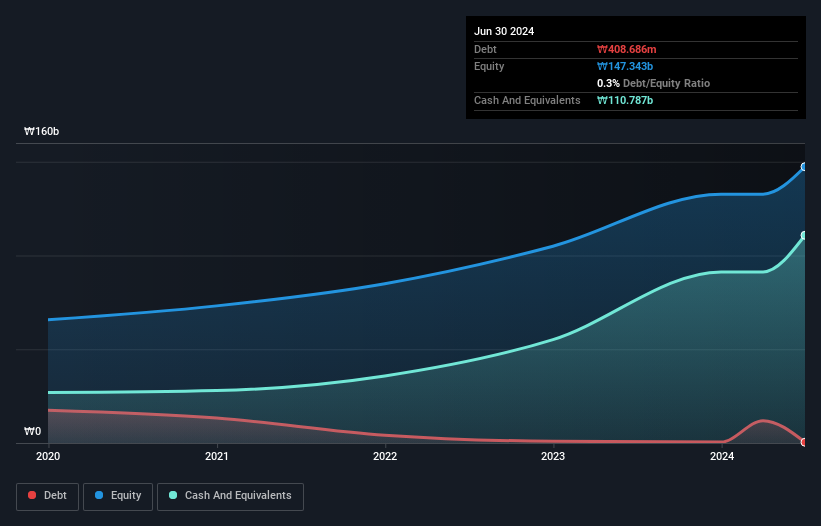

Born Korea, a recently public company with an IPO raising KRW 102 billion, shows promising growth in the hospitality sector. Its earnings surged by 39.5% over the past year, outpacing the industry's -17.7%. The firm trades at 24.8% below its estimated fair value and maintains high-quality earnings with more cash than total debt, indicating robust financial health. Despite its shares being highly illiquid, Born Korea remains free cash flow positive and comfortably covers interest payments with profits. This combination of strong earnings growth and undervaluation positions it as an intriguing prospect for investors seeking emerging opportunities in this space.

- Unlock comprehensive insights into our analysis of Born Korea stock in this health report.

Understand Born Korea's track record by examining our Past report.

Zhejiang Liming Intelligent ManufacturingLtd (SHSE:603048)

Simply Wall St Value Rating: ★★★★★☆

Overview: Zhejiang Liming Intelligent Manufacturing Co., Ltd. operates in the manufacturing sector, focusing on producing car parts, with a market capitalization of CN¥2.46 billion.

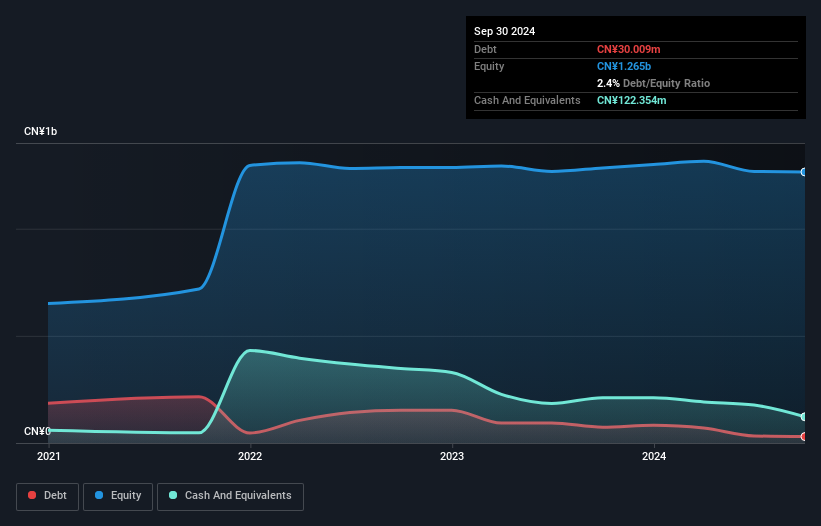

Operations: Liming Intelligent Manufacturing generates revenue primarily from its car parts segment, totaling CN¥638.68 million.

Zhejiang Liming Intelligent Manufacturing, a smaller player in the auto components industry, has shown significant earnings growth of 75% over the past year, outpacing the industry's 10.5%. Despite this impressive short-term performance, its earnings have seen a decrease of 34.8% annually over five years. The company is financially stable with more cash than total debt and successfully covers interest payments with its profits. Recently, it completed a share buyback program acquiring 812,400 shares for CNY 10 million. A notable one-off gain of CNY 13.7 million has impacted recent financial results as of September end.

Seize The Opportunity

- Investigate our full lineup of 4625 Undiscovered Gems With Strong Fundamentals right here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Born Korea might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A475560

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.9% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.1% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|36.0% overvalued

DA

Community Contributor