Advertisement

- South Korea

- /

- Semiconductors

- /

- KOSDAQ:A080580

OKins Electronics Co.,Ltd. (KOSDAQ:080580) Stocks Pounded By 25% But Not Lagging Market On Growth Or Pricing

OKins Electronics Co.,Ltd. (KOSDAQ:080580) shareholders that were waiting for something to happen have been dealt a blow with a 25% share price drop in the last month. The last month has meant the stock is now only up 8.6% during the last year.

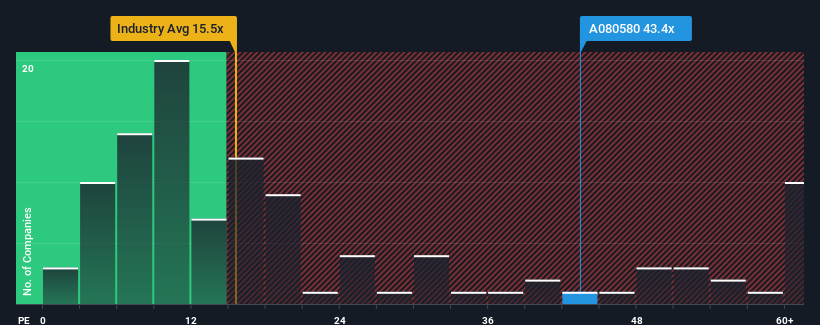

Although its price has dipped substantially, given close to half the companies in Korea have price-to-earnings ratios (or "P/E's") below 11x, you may still consider OKins ElectronicsLtd as a stock to avoid entirely with its 43.4x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

With earnings growth that's exceedingly strong of late, OKins ElectronicsLtd has been doing very well. The P/E is probably high because investors think this strong earnings growth will be enough to outperform the broader market in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for OKins ElectronicsLtd

How Is OKins ElectronicsLtd's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as steep as OKins ElectronicsLtd's is when the company's growth is on track to outshine the market decidedly.

Taking a look back first, we see that the company grew earnings per share by an impressive 183% last year. Pleasingly, EPS has also lifted 206% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

This is in contrast to the rest of the market, which is expected to grow by 34% over the next year, materially lower than the company's recent medium-term annualised growth rates.

In light of this, it's understandable that OKins ElectronicsLtd's P/E sits above the majority of other companies. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Bottom Line On OKins ElectronicsLtd's P/E

Even after such a strong price drop, OKins ElectronicsLtd's P/E still exceeds the rest of the market significantly. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of OKins ElectronicsLtd revealed its three-year earnings trends are contributing to its high P/E, given they look better than current market expectations. Right now shareholders are comfortable with the P/E as they are quite confident earnings aren't under threat. If recent medium-term earnings trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 3 warning signs for OKins ElectronicsLtd (of which 1 is concerning!) you should know about.

You might be able to find a better investment than OKins ElectronicsLtd. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A080580

OKins ElectronicsLtd

Okins Electronics Co.,Ltd. manufactures and sells semiconductor inspection sockets.

Mediocre balance sheet with very low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor