- South Korea

- /

- General Merchandise and Department Stores

- /

- KOSDAQ:A035080

Why It Might Not Make Sense To Buy Interpark Co., Ltd. (KOSDAQ:035080) For Its Upcoming Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Interpark Co., Ltd. (KOSDAQ:035080) is about to go ex-dividend in just three days. You can purchase shares before the 29th of December in order to receive the dividend, which the company will pay on the 10th of April.

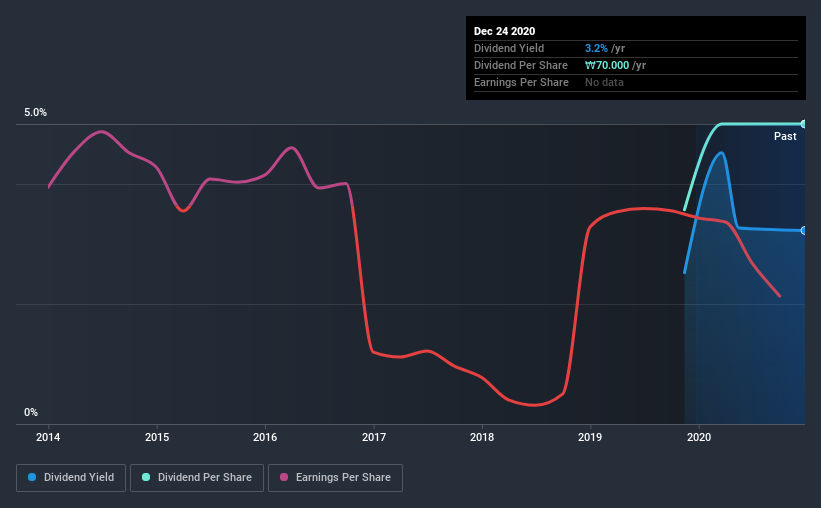

Interpark's next dividend payment will be ₩70.00 per share, on the back of last year when the company paid a total of ₩70.00 to shareholders. Looking at the last 12 months of distributions, Interpark has a trailing yield of approximately 3.2% on its current stock price of ₩2170. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to investigate whether Interpark can afford its dividend, and if the dividend could grow.

See our latest analysis for Interpark

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Interpark paid a dividend last year despite being unprofitable. This might be a one-off event, but it's not a sustainable state of affairs in the long run. With the recent loss, it's important to check if the business generated enough cash to pay its dividend. If Interpark didn't generate enough cash to pay the dividend, then it must have either paid from cash in the bank or by borrowing money, neither of which is sustainable in the long term. It paid out an unsustainably high 248% of its free cash flow as dividends over the past 12 months, which is worrying. It's pretty hard to pay out more than you earn, so we wonder how Interpark intends to continue funding this dividend, or if it could be forced to cut the payment.

Interpark does have a large net cash position on the balance sheet, which could fund large dividends for a time, if the company so chose. Still, smart investors know that it is better to assess dividends relative to the cash and profit generated by the business. Paying dividends out of cash on the balance sheet is not long-term sustainable.

Click here to see how much of its profit Interpark paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Interpark reported a loss last year, and the general trend suggests its earnings have also been declining in recent years, making us wonder if the dividend is at risk.

Given that Interpark has only been paying a dividend for a year, there's not much of a past history to draw insight from.

We update our analysis on Interpark every 24 hours, so you can always get the latest insights on its financial health, here.

The Bottom Line

From a dividend perspective, should investors buy or avoid Interpark? It's hard to get used to Interpark paying a dividend despite reporting a loss over the past year. Worse, the dividend was not well covered by cash flow. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

With that in mind though, if the poor dividend characteristics of Interpark don't faze you, it's worth being mindful of the risks involved with this business. For example, Interpark has 3 warning signs (and 1 which doesn't sit too well with us) we think you should know about.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Interpark, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A035080

Gradiant

Engages in e-commerce business in South Korea, Vietnam, China, and internationally.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Community Narratives