Advertisement

- South Korea

- /

- Pharma

- /

- KOSDAQ:A102940

The 25% return this week takes Kolon Life Science's (KOSDAQ:102940) shareholders five-year gains to 62%

Generally speaking the aim of active stock picking is to find companies that provide returns that are superior to the market average. Buying under-rated businesses is one path to excess returns. For example, long term Kolon Life Science Inc. (KOSDAQ:102940) shareholders have enjoyed a 62% share price rise over the last half decade, well in excess of the market return of around 21% (not including dividends). However, more recent returns haven't been as impressive as that, with the stock returning just 25% in the last year.

Since the stock has added ₩72b to its market cap in the past week alone, let's see if underlying performance has been driving long-term returns.

See our latest analysis for Kolon Life Science

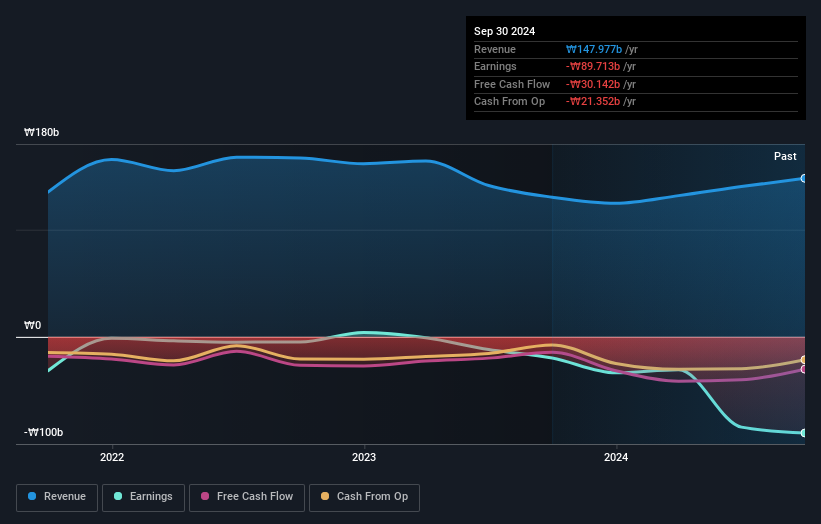

Given that Kolon Life Science didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. Shareholders of unprofitable companies usually desire strong revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

In the last 5 years Kolon Life Science saw its revenue shrink by 0.4% per year. Even though revenue hasn't increased, the stock actually gained 10%, per year, during the same period. It's probably worth checking other factors such as the profitability, to try to understand the share price action. It may not be reflecting the revenue.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

You can see how its balance sheet has strengthened (or weakened) over time in this free interactive graphic.

A Different Perspective

We're pleased to report that Kolon Life Science shareholders have received a total shareholder return of 25% over one year. That's better than the annualised return of 10% over half a decade, implying that the company is doing better recently. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. It's always interesting to track share price performance over the longer term. But to understand Kolon Life Science better, we need to consider many other factors. To that end, you should learn about the 2 warning signs we've spotted with Kolon Life Science (including 1 which makes us a bit uncomfortable) .

We will like Kolon Life Science better if we see some big insider buys. While we wait, check out this free list of undervalued stocks (mostly small caps) with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on South Korean exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Kolon Life Science might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A102940

Kolon Life Science

A biotechnology company, develops cell and gene therapy products.

Very low with worrying balance sheet.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor