Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Komipharm International Co., Ltd. (KOSDAQ:041960) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Komipharm International

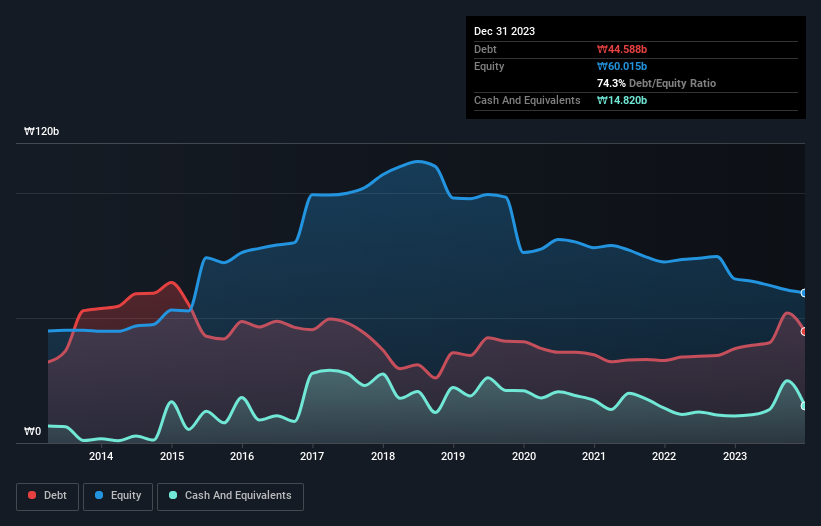

What Is Komipharm International's Debt?

You can click the graphic below for the historical numbers, but it shows that as of December 2023 Komipharm International had ₩44.6b of debt, an increase on ₩37.7b, over one year. However, it also had ₩14.8b in cash, and so its net debt is ₩29.8b.

How Healthy Is Komipharm International's Balance Sheet?

The latest balance sheet data shows that Komipharm International had liabilities of ₩52.2b due within a year, and liabilities of ₩6.35b falling due after that. On the other hand, it had cash of ₩14.8b and ₩17.9b worth of receivables due within a year. So its liabilities total ₩25.9b more than the combination of its cash and short-term receivables.

Of course, Komipharm International has a market capitalization of ₩343.4b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Komipharm International will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Komipharm International wasn't profitable at an EBIT level, but managed to grow its revenue by 7.2%, to ₩43b. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Over the last twelve months Komipharm International produced an earnings before interest and tax (EBIT) loss. Indeed, it lost ₩6.3b at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through ₩3.9b of cash over the last year. So to be blunt we think it is risky. For riskier companies like Komipharm International I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Komipharm International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A041960

Komipharm International

Manufactures and sells veterinary vaccines, veterinary pharmaceuticals and disinfectants, and bio-fertilizers internationally.

Fair value with acceptable track record.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.6% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.5% undervalued

AG

Community Contributor