Advertisement

- South Korea

- /

- Entertainment

- /

- KOSDAQ:A253450

High Growth Tech Stocks To Explore In February 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate the complexities of tariff uncertainties and fluctuating economic indicators, major indices like the S&P 500 have shown resilience despite recent declines, while manufacturing activity in the U.S. has expanded for the first time in over two years. In this environment, identifying high-growth tech stocks requires a keen understanding of how these companies can leverage innovation and adaptability to thrive amidst broader market challenges.

Top 10 High Growth Tech Companies

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| eWeLLLtd | 26.41% | 28.82% | ★★★★★★ |

| Ascelia Pharma | 68.22% | 59.79% | ★★★★★★ |

| Alnylam Pharmaceuticals | 21.62% | 56.70% | ★★★★★★ |

| Fine M-TecLTD | 36.52% | 135.02% | ★★★★★★ |

| Alkami Technology | 21.99% | 102.65% | ★★★★★★ |

| Travere Therapeutics | 30.52% | 61.89% | ★★★★★★ |

| Initiator Pharma | 73.95% | 31.67% | ★★★★★★ |

| JNTC | 29.48% | 104.37% | ★★★★★★ |

| Dmall | 29.53% | 88.37% | ★★★★★★ |

| Delton Technology (Guangzhou) | 20.25% | 29.52% | ★★★★★★ |

Click here to see the full list of 1217 stocks from our High Growth Tech and AI Stocks screener.

We're going to check out a few of the best picks from our screener tool.

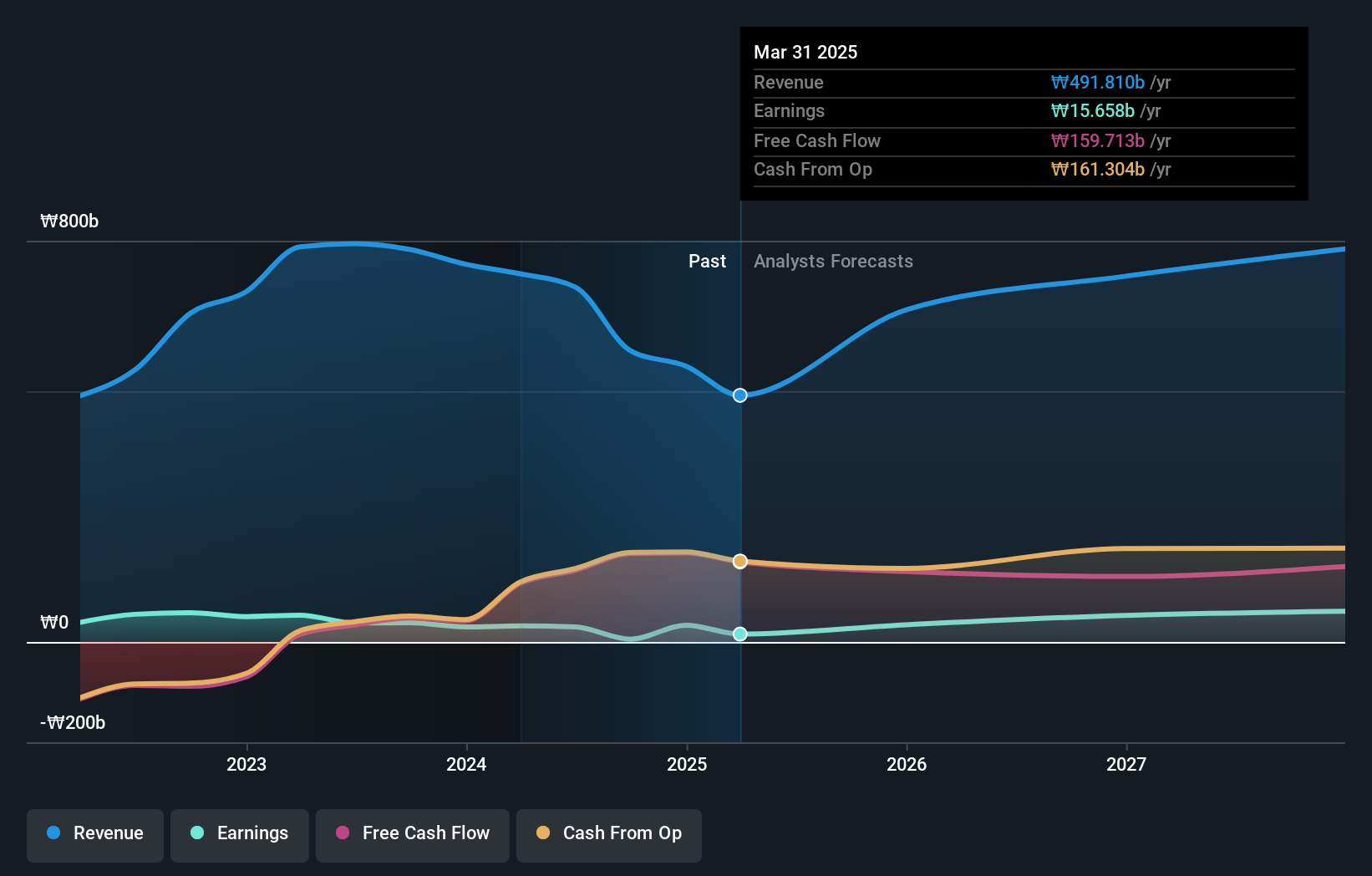

Studio Dragon (KOSDAQ:A253450)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Studio Dragon Corporation is a drama studio that produces and distributes drama content globally, with a market cap of ₩1.15 billion.

Operations: The company generates revenue primarily through television programming and distribution, amounting to approximately ₩580.61 billion.

Studio Dragon's financial landscape presents a mixed bag of robust earnings growth juxtaposed with challenges in revenue acceleration and profit margins. With an impressive annual earnings increase projected at 33.6%, the company outpaces the broader Korean market's growth rate of 27%. However, its revenue growth at 12.1% annually, though surpassing the market average of 9.1%, does not reach the high-growth threshold of 20% typically seen in leading tech sectors. Additionally, recent one-off losses totaling ₩15.1 billion have notably impacted financial outcomes, reflecting a dip in net profit margins from last year’s 4.9% to just 1%. Despite these hurdles, Studio Dragon’s consistent investment in R&D and strategic presence at key industry events like the Daishin Securities Corporate Day highlight its ongoing commitment to innovation and sector leadership.

- Click here to discover the nuances of Studio Dragon with our detailed analytical health report.

Review our historical performance report to gain insights into Studio Dragon's's past performance.

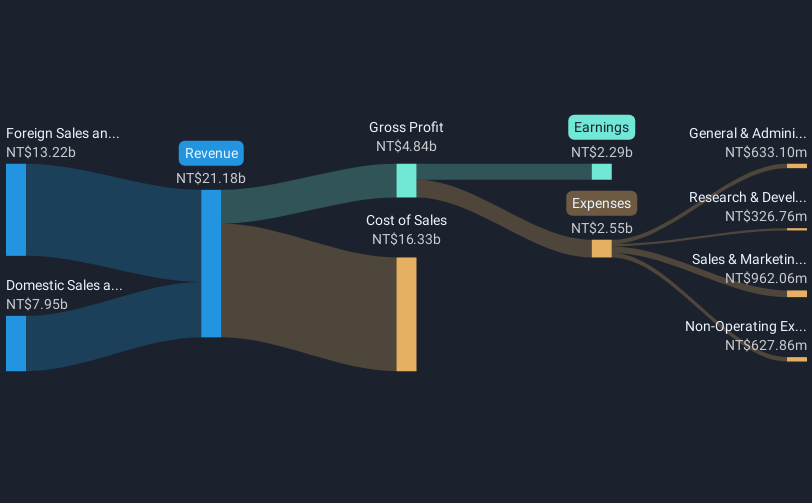

Taiwan Union Technology (TPEX:6274)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Taiwan Union Technology Corporation specializes in the production and distribution of copper foil substrates, adhesive sheets, and multi-layer laminated boards both domestically and internationally, with a market cap of NT$45.12 billion.

Operations: The company generates revenue through its Foreign Sales and Manufacturing Sector, contributing NT$13.22 billion, and its Domestic Sales and Manufacturing Sector, adding NT$7.95 billion. The focus is on manufacturing copper foil substrates, adhesive sheets, and multi-layer laminated boards for both domestic and international markets.

Taiwan Union Technology is navigating a dynamic landscape with its robust earnings growth at 23.4% annually, outstripping the Taiwanese market's average of 17.6%. This performance is underpinned by a significant R&D commitment, which has seen expenses grow to represent a substantial portion of revenue, aligning with the company's strategic focus on innovation in electronics. Recent executive changes, including the appointment of Lin Hsiao-Chiao as CFO—a seasoned leader from LuxNet Corporation—suggest a strategic pivot that could further influence financial strategies and market positioning. These factors collectively underscore Taiwan Union’s potential to adapt and thrive amidst evolving industry demands.

- Unlock comprehensive insights into our analysis of Taiwan Union Technology stock in this health report.

Evaluate Taiwan Union Technology's historical performance by accessing our past performance report.

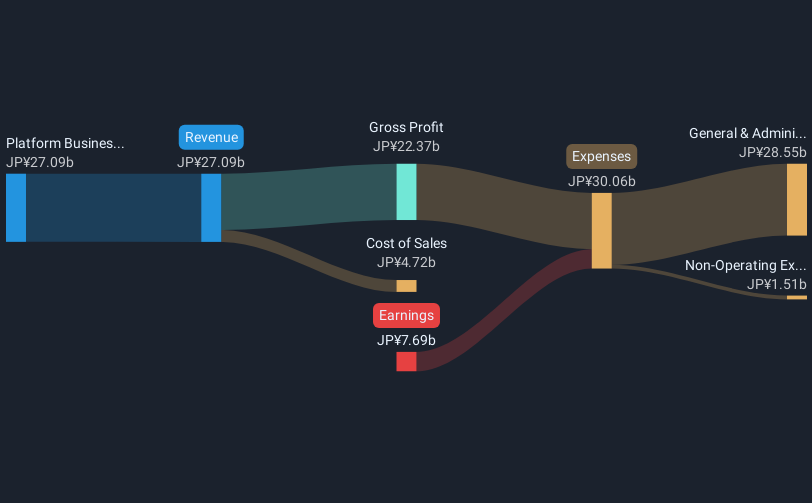

freee K.K (TSE:4478)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: freee K.K. provides cloud-based accounting and HR software solutions in Japan, with a market cap of ¥198.74 billion.

Operations: The company generates revenue primarily through its Platform Business, which reported ¥27.09 billion. The focus is on delivering cloud-based solutions for accounting and HR needs in Japan.

Freee K.K. is poised for significant transformation, with its revenue projected to expand by 18.5% annually, outpacing the Japanese market's growth of 4.2%. This growth trajectory is complemented by an anticipated surge in earnings, expected to increase by 71.35% per year as the company moves towards profitability within three years. Notably, Freee K.K.'s commitment to innovation is evident in its R&D strategy; however, specific financial figures for R&D expenses were not provided. The recent decision during a board meeting to issue new restricted shares highlights strategic initiatives aimed at bolstering this growth and innovation focus.

Make It Happen

- Get an in-depth perspective on all 1217 High Growth Tech and AI Stocks by using our screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A253450

Studio Dragon

A drama studio, produces and provides drama contents worldwide.

Excellent balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|43.0% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|18.3% undervalued

BL

Community Contributor