Advertisement

- South Korea

- /

- Basic Materials

- /

- KOSE:A300720

Theon International Plus 2 Other Undiscovered Gems with Strong Fundamentals

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, global markets have experienced a mixed performance, with large-cap stocks generally faring better than their small-cap counterparts, as evidenced by the Russell 2000 Index's underperformance compared to the S&P 500. Amidst this backdrop of economic shifts and anticipated interest rate cuts from major central banks, investors are increasingly seeking opportunities in smaller companies with solid fundamentals that may not yet be widely recognized. Identifying such stocks requires a focus on robust financial health and growth potential, especially in an environment where market sentiment is volatile and economic indicators are closely monitored.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Zona Franca de Iquique | NA | 7.94% | 12.83% | ★★★★★★ |

| SALUS Ljubljana d. d | 13.55% | 13.11% | 9.95% | ★★★★★★ |

| FRoSTA | 8.18% | 4.36% | 16.00% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Standard Bank | 0.13% | 27.78% | 30.36% | ★★★★★★ |

| Aesler Grup Internasional | NA | -17.61% | -40.21% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| MAPFRE Middlesea | NA | 14.56% | 1.77% | ★★★★★☆ |

| Compañía Electro Metalúrgica | 71.27% | 12.50% | 19.90% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

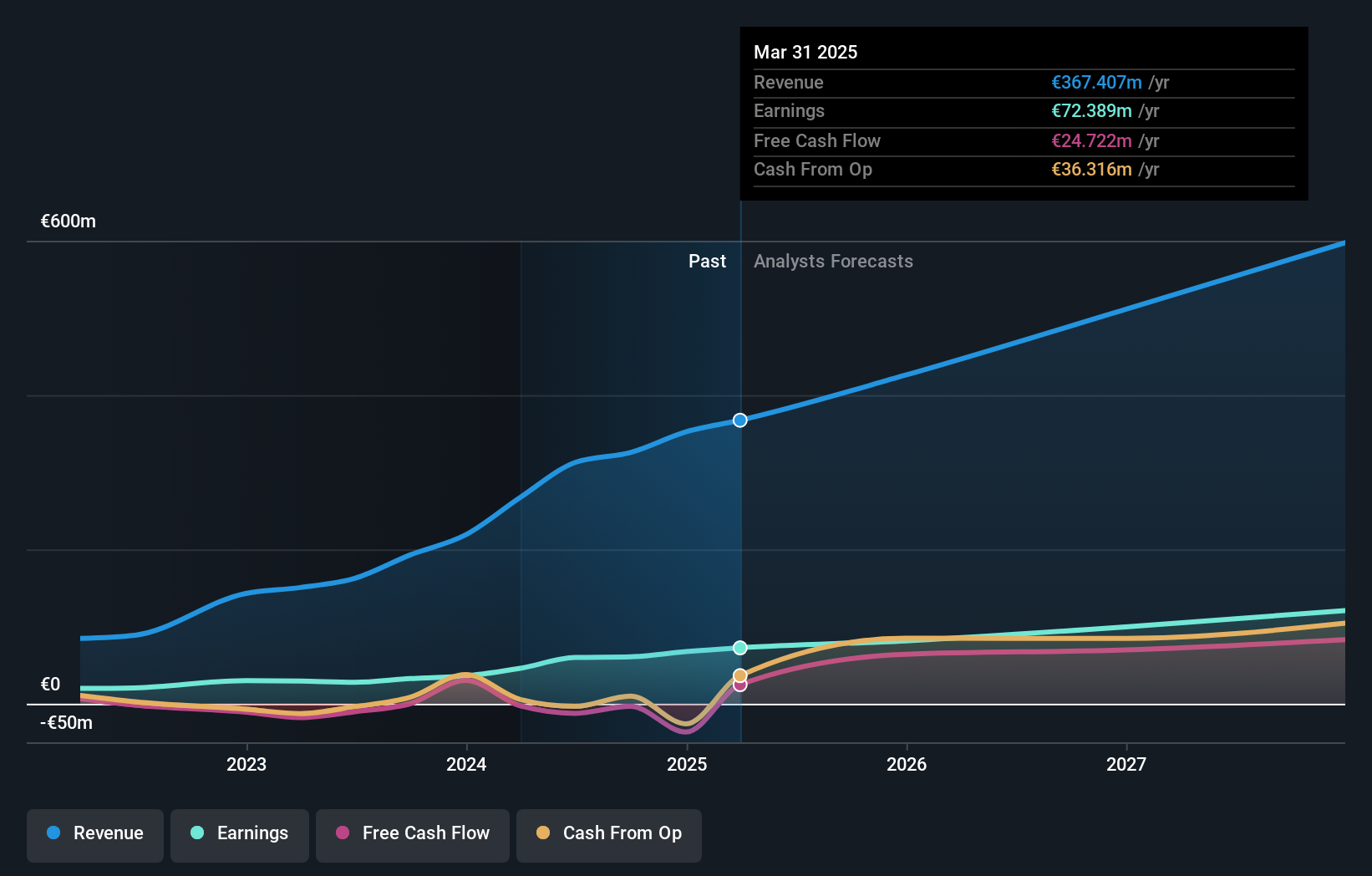

Theon International (ENXTAM:THEON)

Simply Wall St Value Rating: ★★★★★☆

Overview: Theon International Plc specializes in developing and manufacturing customizable night vision, thermal imaging, and electro-optical ISR systems for military and security applications across Europe and globally, with a market cap of €875 million.

Operations: Theon International generates revenue primarily from its optronics segment, amounting to €325.57 million. The company has a market capitalization of approximately €875 million.

Theon International, a small player in the Aerospace & Defense sector, has shown impressive financial resilience. Over the past five years, its debt-to-equity ratio significantly decreased from 270% to 32.9%, reflecting prudent financial management. Despite its volatile share price recently, Theon's earnings growth of 86.6% last year outpaced the industry average of 22.5%. The company is trading at a substantial discount of 42.7% below estimated fair value and boasts an EBIT coverage for interest payments at an astounding 89 times over—indicating strong profitability and operational efficiency amidst industry challenges.

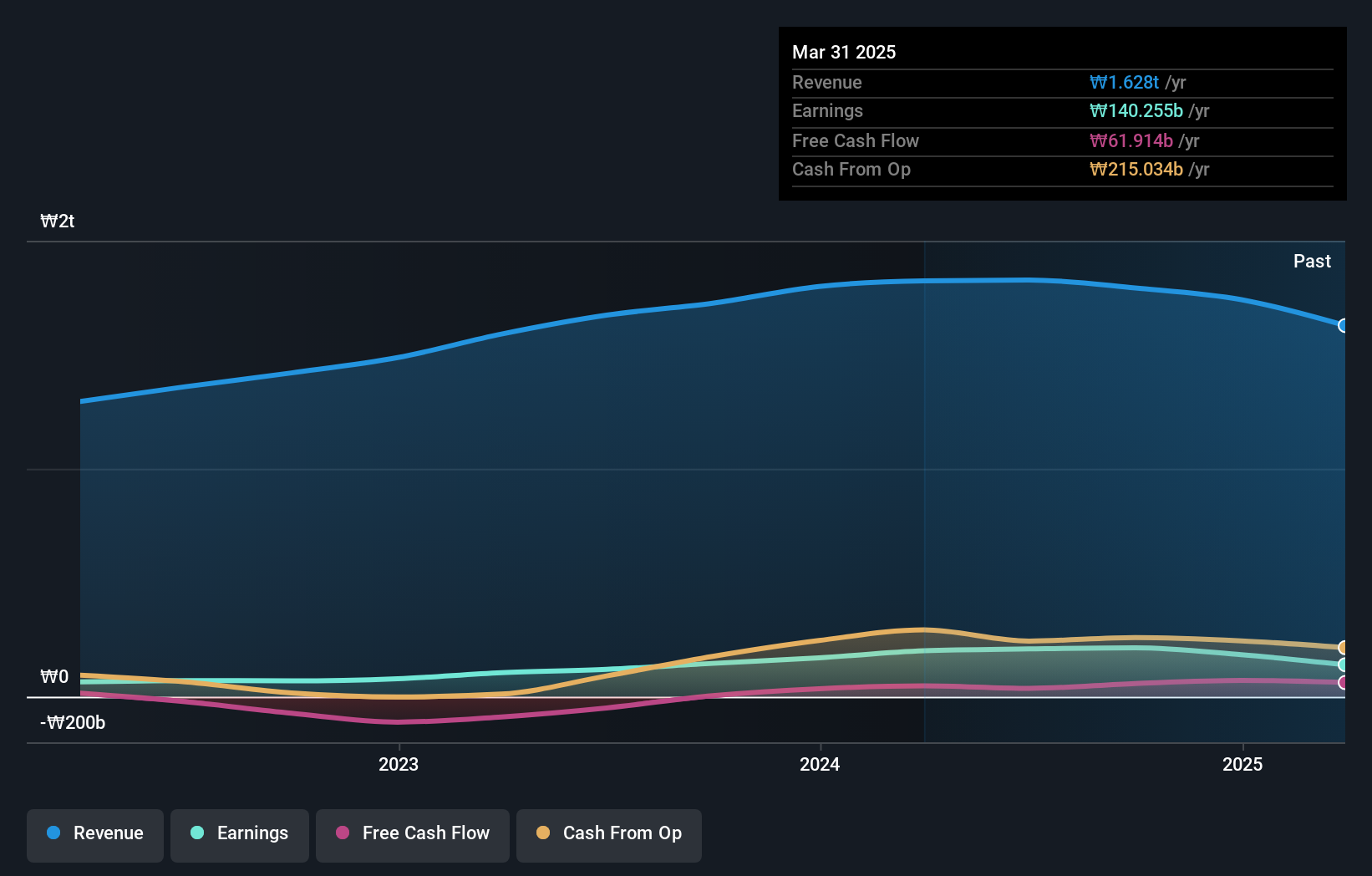

Hanil Cement (KOSE:A300720)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hanil Cement Co., Ltd. is engaged in the production and sale of cements, ready-mixed concretes, and admixtures, with a market capitalization of ₩1.10 trillion.

Operations: Hanil Cement generates revenue primarily from its Cement Sector, contributing ₩917.97 billion, and the Remital Sector, adding ₩468.26 billion. The Ready-Mixed Concrete Sector also plays a significant role with revenues of ₩277.42 billion.

Hanil Cement, a smaller player in the cement industry, demonstrates robust financial health with its interest payments well covered by EBIT at 14.2 times. The net debt to equity ratio stands at a satisfactory 20.3%, indicating prudent financial management. Over the past year, earnings have surged by 46.8%, outpacing the Basic Materials industry's growth of 16.6%. Despite fluctuations in levered free cash flow, which reached US$57 million recently after previous negative figures, Hanil appears to be trading significantly below its estimated fair value by about 91%. A recent extraordinary shareholders meeting suggests active engagement in strategic decisions moving forward.

- Take a closer look at Hanil Cement's potential here in our health report.

Explore historical data to track Hanil Cement's performance over time in our Past section.

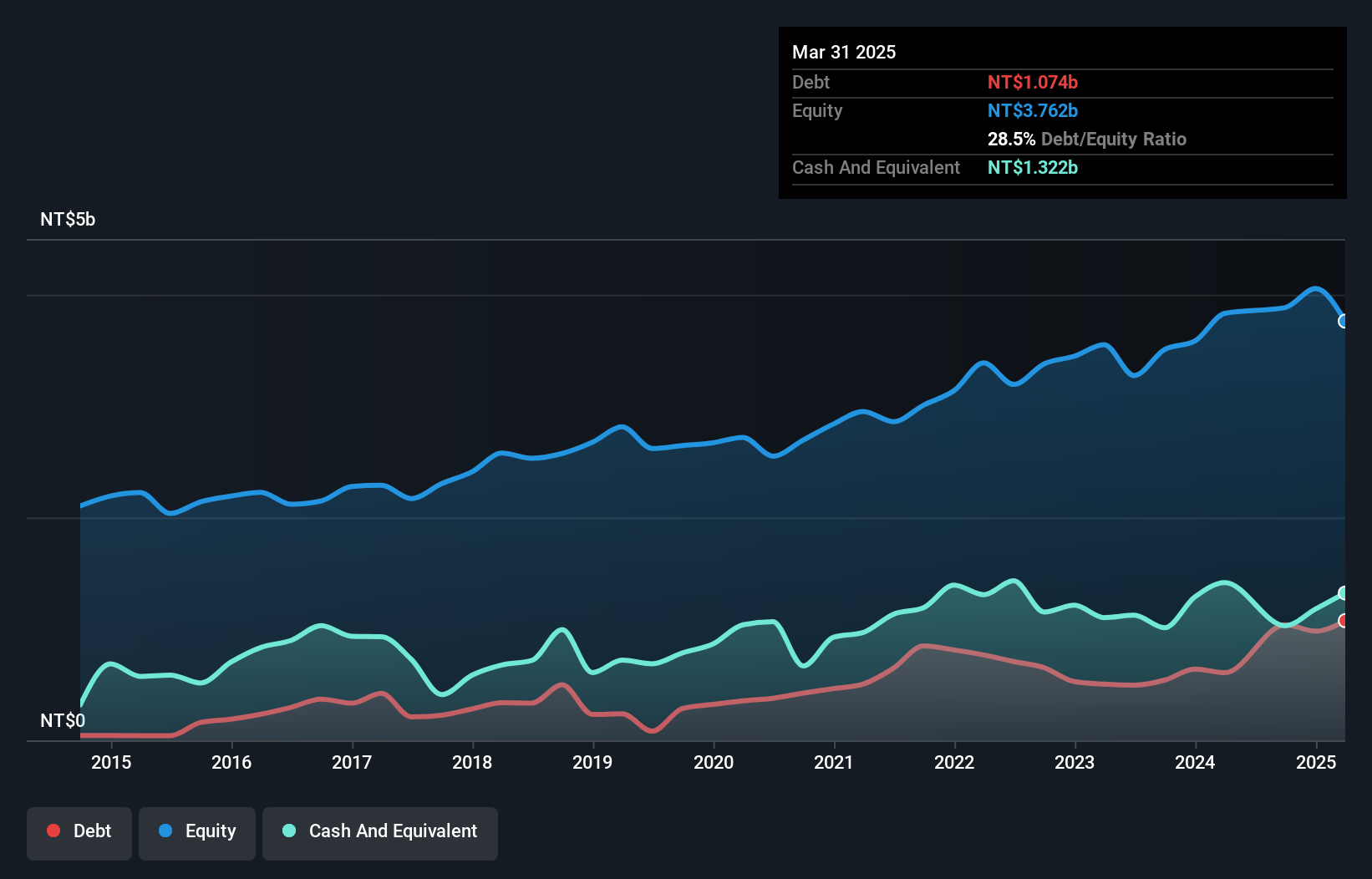

TURVO International (TWSE:2233)

Simply Wall St Value Rating: ★★★★★☆

Overview: TURVO International Co., Ltd. specializes in the development, production, and sale of precision metal parts and components with a market capitalization of approximately NT$13.17 billion.

Operations: The company's revenue primarily comes from its operations in China and Taiwan, generating NT$2.66 billion and NT$1.81 billion, respectively.

Turvo International seems to be catching attention with its robust growth and solid financials. Revenue for the third quarter hit TWD 964 million, up from TWD 897.52 million last year, while net income rose to TWD 187.36 million from TWD 155.37 million. The company is trading at a value perceived as 23% below fair estimates, suggesting potential upside for investors eyeing value opportunities. Earnings have grown by an impressive 35%, outpacing the Machinery industry's average of 14%. Despite a rise in the debt-to-equity ratio over five years, Turvo's net debt remains satisfactory at just 0.2%.

Summing It All Up

- Embark on your investment journey to our 4621 Undiscovered Gems With Strong Fundamentals selection here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hanil Cement might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A300720

Hanil Cement

Produces and sells cements, ready-mixed concretes, and admixtures.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|35.7% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|20.5% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|25.2% overvalued

DA

Community Contributor