Advertisement

- South Korea

- /

- Chemicals

- /

- KOSE:A298020

Should You Buy Hyosung TNC Corporation (KRX:298020) For Its Upcoming Dividend?

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Hyosung TNC Corporation (KRX:298020) is about to go ex-dividend in just 3 days. The ex-dividend date is one business day before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. Therefore, if you purchase Hyosung TNC's shares on or after the 27th of December, you won't be eligible to receive the dividend, when it is paid on the 2nd of April.

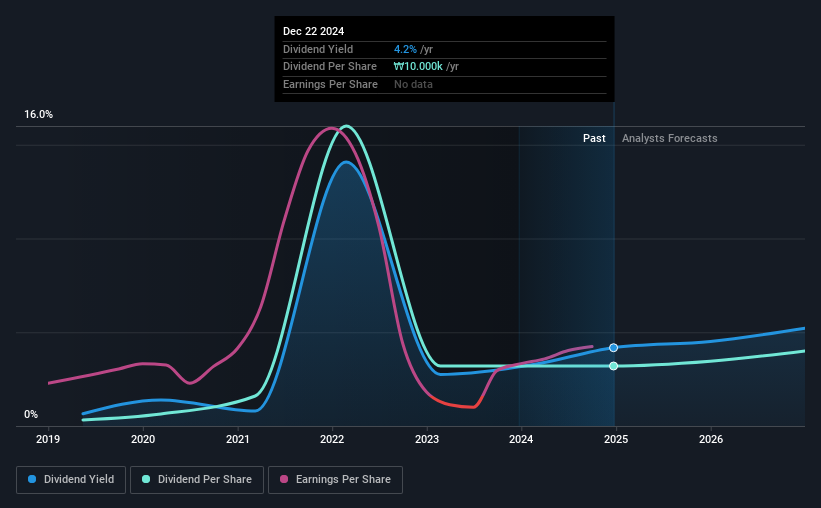

The company's next dividend payment will be ₩10000.00 per share, and in the last 12 months, the company paid a total of ₩10,000 per share. Looking at the last 12 months of distributions, Hyosung TNC has a trailing yield of approximately 4.2% on its current stock price of ₩239500.00. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! We need to see whether the dividend is covered by earnings and if it's growing.

Check out our latest analysis for Hyosung TNC

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Hyosung TNC paid out a comfortable 30% of its profit last year. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. It distributed 31% of its free cash flow as dividends, a comfortable payout level for most companies.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If earnings fall far enough, the company could be forced to cut its dividend. That's why it's comforting to see Hyosung TNC's earnings have been skyrocketing, up 31% per annum for the past five years. Hyosung TNC is paying out less than half its earnings and cash flow, while simultaneously growing earnings per share at a rapid clip. Companies with growing earnings and low payout ratios are often the best long-term dividend stocks, as the company can both grow its earnings and increase the percentage of earnings that it pays out, essentially multiplying the dividend.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the last six years, Hyosung TNC has lifted its dividend by approximately 47% a year on average. Both per-share earnings and dividends have both been growing rapidly in recent times, which is great to see.

The Bottom Line

From a dividend perspective, should investors buy or avoid Hyosung TNC? Hyosung TNC has grown its earnings per share while simultaneously reinvesting in the business. Unfortunately it's cut the dividend at least once in the past six years, but the conservative payout ratio makes the current dividend look sustainable. It's a promising combination that should mark this company worthy of closer attention.

On that note, you'll want to research what risks Hyosung TNC is facing. In terms of investment risks, we've identified 3 warning signs with Hyosung TNC and understanding them should be part of your investment process.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Hyosung TNC might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A298020

Hyosung TNC

Manufactures and sells fiber in South Korea and internationally.

Very undervalued with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor