- South Korea

- /

- Metals and Mining

- /

- KOSE:A010130

Korea Zinc Company, Ltd.'s (KRX:010130) Stock Been Rising: Are Strong Financials Guiding The Market?

Korea Zinc Company's (KRX:010130) stock is up by 6.6% over the past three months. Since the market usually pay for a company’s long-term financial health, we decided to study the company’s fundamentals to see if they could be influencing the market. Specifically, we decided to study Korea Zinc Company's ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

See our latest analysis for Korea Zinc Company

How Is ROE Calculated?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Korea Zinc Company is:

8.1% = ₩565b ÷ ₩7.0t (Based on the trailing twelve months to September 2020).

The 'return' is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each ₩1 of shareholders' capital it has, the company made ₩0.08 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Korea Zinc Company's Earnings Growth And 8.1% ROE

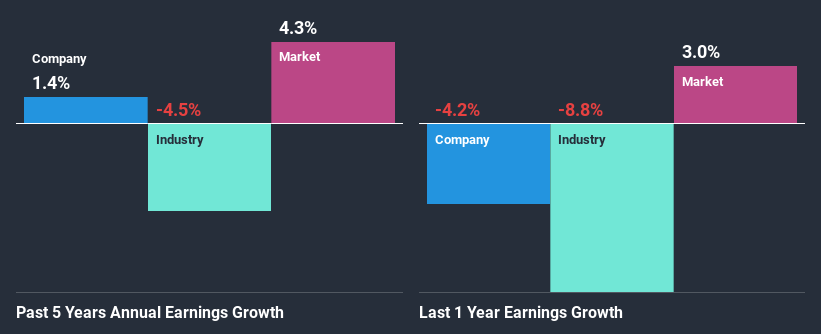

At first glance, Korea Zinc Company's ROE doesn't look very promising. However, the fact that the its ROE is quite higher to the industry average of 3.7% doesn't go unnoticed by us. Having said that, Korea Zinc Company's net income growth over the past five years is more or less flat. Remember, the company's ROE is a bit low to begin with, just that it is higher than the industry average. Therefore, the low to flat growth in earnings could also be the result of this.

Given that the industry shrunk its earnings at a rate of 4.5% in the same period, the net income growth of the company is quite impressive.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. Is A010130 fairly valued? This infographic on the company's intrinsic value has everything you need to know.

Is Korea Zinc Company Using Its Retained Earnings Effectively?

In spite of a normal three-year median payout ratio of 38% (or a retention ratio of 62%), Korea Zinc Company hasn't seen much growth in its earnings. So there could be some other explanation in that regard. For instance, the company's business may be deteriorating.

In addition, Korea Zinc Company has been paying dividends over a period of at least ten years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth. Our latest analyst data shows that the future payout ratio of the company over the next three years is expected to be approximately 42%. Accordingly, forecasts suggest that Korea Zinc Company's future ROE will be 8.4% which is again, similar to the current ROE.

Summary

In total, we are pretty happy with Korea Zinc Company's performance. Specifically, we like that it has been reinvesting a high portion of its profits at a moderate rate of return, resulting in earnings expansion. Having said that, looking at the current analyst estimates, we found that the company's earnings are expected to gain momentum. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

When trading Korea Zinc Company or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Korea Zinc Company might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A010130

Korea Zinc Company

Operates as a general non-ferrous metal smelting company primarily in South Korea.

Excellent balance sheet with acceptable track record.