Advertisement

- South Korea

- /

- Metals and Mining

- /

- KOSE:A005490

Should You Buy POSCO (KRX:005490) For Its Upcoming Dividend?

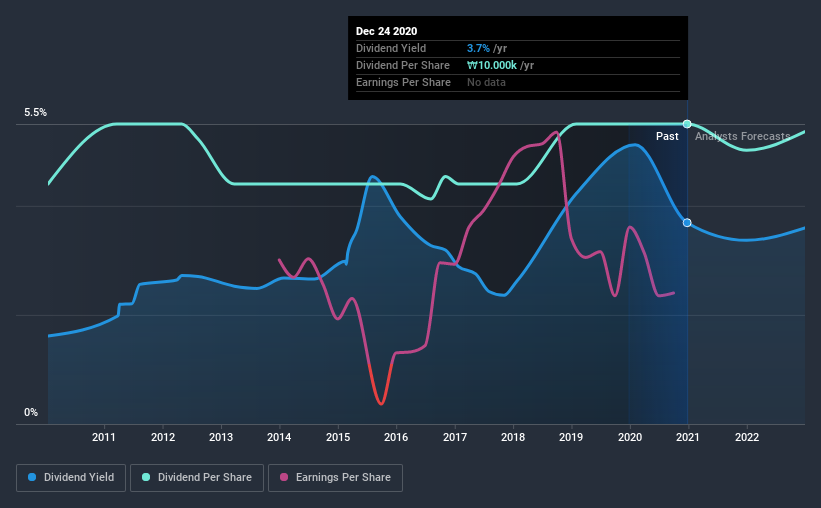

Readers hoping to buy POSCO (KRX:005490) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. Ex-dividend means that investors that purchase the stock on or after the 29th of December will not receive this dividend, which will be paid on the 27th of April.

POSCO's next dividend payment will be ₩4,000 per share, and in the last 12 months, the company paid a total of ₩10,000 per share. Looking at the last 12 months of distributions, POSCO has a trailing yield of approximately 3.7% on its current stock price of ₩271000. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. As a result, readers should always check whether POSCO has been able to grow its dividends, or if the dividend might be cut.

Check out our latest analysis for POSCO

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. POSCO is paying out an acceptable 63% of its profit, a common payout level among most companies. A useful secondary check can be to evaluate whether POSCO generated enough free cash flow to afford its dividend. The good news is it paid out just 15% of its free cash flow in the last year.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings fall far enough, the company could be forced to cut its dividend. With that in mind, we're encouraged by the steady growth at POSCO, with earnings per share up 9.5% on average over the last five years. While earnings have been growing at a credible rate, the company is paying out a majority of its earnings to shareholders. Therefore it's unlikely that the company will be able to reinvest heavily in its business, which could presage slower growth in the future.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the last 10 years, POSCO has lifted its dividend by approximately 2.3% a year on average. We're glad to see dividends rising alongside earnings over a number of years, which may be a sign the company intends to share the growth with shareholders.

To Sum It Up

Is POSCO worth buying for its dividend? Earnings per share growth has been modest and POSCO paid out over half of its profits and less than half of its free cash flow, although both payout ratios are within normal limits. To summarise, POSCO looks okay on this analysis, although it doesn't appear a stand-out opportunity.

On that note, you'll want to research what risks POSCO is facing. Our analysis shows 4 warning signs for POSCO and you should be aware of them before buying any shares.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade POSCO, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A005490

POSCO Holdings

Operates as an integrated steel producer in Korea and internationally.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor