- South Korea

- /

- Personal Products

- /

- KOSDAQ:A018290

Revenues Tell The Story For VT Co., Ltd. (KOSDAQ:018290) As Its Stock Soars 27%

Despite an already strong run, VT Co., Ltd. (KOSDAQ:018290) shares have been powering on, with a gain of 27% in the last thirty days. The last 30 days were the cherry on top of the stock's 323% gain in the last year, which is nothing short of spectacular.

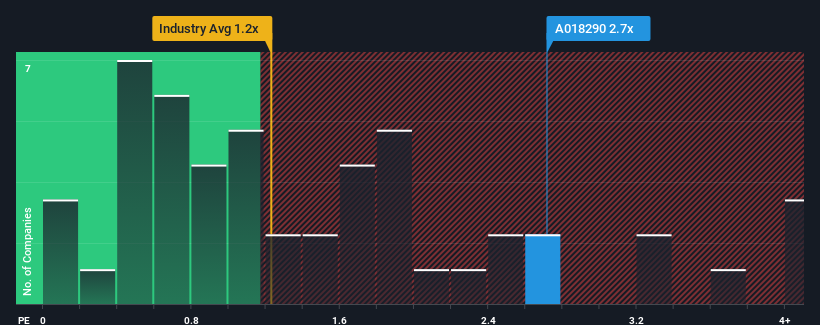

Following the firm bounce in price, given close to half the companies operating in Korea's Personal Products industry have price-to-sales ratios (or "P/S") below 1.2x, you may consider VT as a stock to potentially avoid with its 2.7x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

View our latest analysis for VT

What Does VT's P/S Mean For Shareholders?

With revenue growth that's exceedingly strong of late, VT has been doing very well. The P/S ratio is probably high because investors think this strong revenue growth will be enough to outperform the broader industry in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Although there are no analyst estimates available for VT, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is VT's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as high as VT's is when the company's growth is on track to outshine the industry.

Retrospectively, the last year delivered an exceptional 51% gain to the company's top line. The latest three year period has also seen an excellent 198% overall rise in revenue, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing revenue over that time.

When compared to the industry's one-year growth forecast of 18%, the most recent medium-term revenue trajectory is noticeably more alluring

In light of this, it's understandable that VT's P/S sits above the majority of other companies. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

What We Can Learn From VT's P/S?

The large bounce in VT's shares has lifted the company's P/S handsomely. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that VT maintains its high P/S on the strength of its recent three-year growth being higher than the wider industry forecast, as expected. At this stage investors feel the potential continued revenue growth in the future is great enough to warrant an inflated P/S. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

We don't want to rain on the parade too much, but we did also find 2 warning signs for VT that you need to be mindful of.

If these risks are making you reconsider your opinion on VT, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A018290

Outstanding track record with flawless balance sheet.

Market Insights

Community Narratives