Advertisement

- South Korea

- /

- Healthtech

- /

- KOSDAQ:A311690

Does CJ Bioscience (KOSDAQ:311690) Have A Healthy Balance Sheet?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies CJ Bioscience, Inc. (KOSDAQ:311690) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

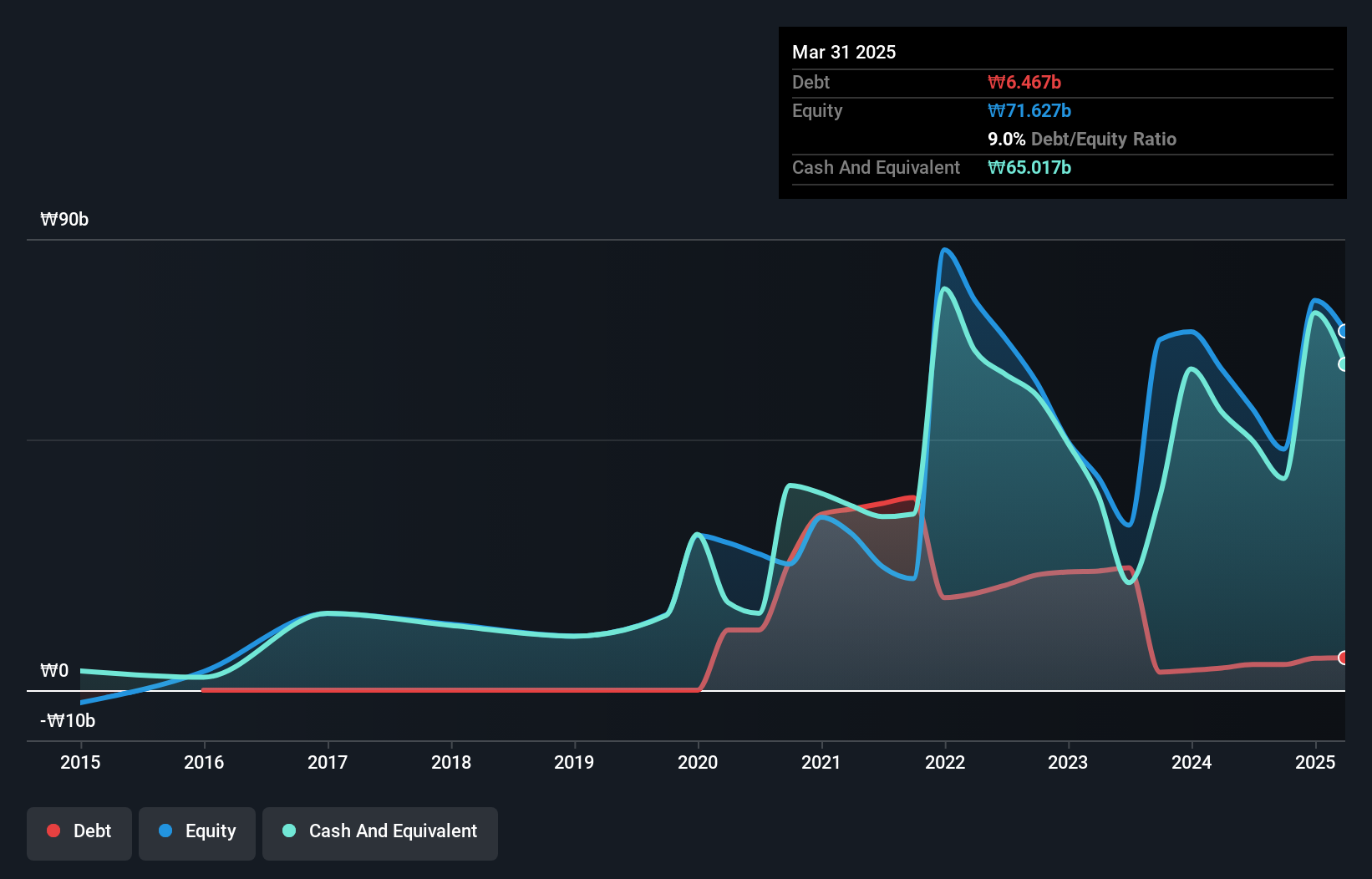

How Much Debt Does CJ Bioscience Carry?

The image below, which you can click on for greater detail, shows that at March 2025 CJ Bioscience had debt of ₩6.47b, up from ₩4.42b in one year. However, its balance sheet shows it holds ₩65.0b in cash, so it actually has ₩58.5b net cash.

A Look At CJ Bioscience's Liabilities

We can see from the most recent balance sheet that CJ Bioscience had liabilities of ₩13.7b falling due within a year, and liabilities of ₩3.28b due beyond that. Offsetting this, it had ₩65.0b in cash and ₩915.0m in receivables that were due within 12 months. So it can boast ₩49.0b more liquid assets than total liabilities.

This luscious liquidity implies that CJ Bioscience's balance sheet is sturdy like a giant sequoia tree. Having regard to this fact, we think its balance sheet is as strong as an ox. Succinctly put, CJ Bioscience boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is CJ Bioscience's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Check out our latest analysis for CJ Bioscience

In the last year CJ Bioscience had a loss before interest and tax, and actually shrunk its revenue by 38%, to ₩3.4b. To be frank that doesn't bode well.

So How Risky Is CJ Bioscience?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that CJ Bioscience had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through ₩30b of cash and made a loss of ₩32b. However, it has net cash of ₩58.5b, so it has a bit of time before it will need more capital. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. We've identified 3 warning signs with CJ Bioscience (at least 2 which can't be ignored) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A311690

CJ Bioscience

Provides microbiome solutions to address unmet medical needs in South Korea and internationally.

Flawless balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor