- South Korea

- /

- Electrical

- /

- KOSE:A298040

Top Growth Companies With High Insider Ownership On KRX

Reviewed by Simply Wall St

Over the last 7 days, the South Korean market has dropped 5.7%, driven by declines in every sector, and it is also down 3.9% over the past year. However, with earnings expected to grow by 29% per annum over the next few years, identifying growth companies with high insider ownership could be particularly advantageous in navigating these market conditions.

Top 10 Growth Companies With High Insider Ownership In South Korea

| Name | Insider Ownership | Earnings Growth |

| People & Technology (KOSDAQ:A137400) | 16.5% | 35.6% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.5% | 52.1% |

| Bioneer (KOSDAQ:A064550) | 17.5% | 97.6% |

| Park Systems (KOSDAQ:A140860) | 33% | 35.7% |

| Oscotec (KOSDAQ:A039200) | 26.3% | 122% |

| ALTEOGEN (KOSDAQ:A196170) | 26.6% | 99.5% |

| Vuno (KOSDAQ:A338220) | 19.5% | 110.9% |

| HANA Micron (KOSDAQ:A067310) | 21.3% | 106.2% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

| Techwing (KOSDAQ:A089030) | 18.7% | 83.6% |

Let's review some notable picks from our screened stocks.

CLASSYS (KOSDAQ:A214150)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: CLASSYS Inc. is a global provider of medical aesthetics devices, with a market cap of ₩3.51 billion.

Operations: The company generates revenue primarily from its Surgical & Medical Equipment segment, amounting to ₩204.37 million.

Insider Ownership: 10.1%

Earnings Growth Forecast: 22.5% p.a.

CLASSYS, a South Korean growth company with high insider ownership, is forecast to achieve a return on equity of 28.1% in three years and is trading at 15.4% below its estimated fair value. While earnings are expected to grow significantly at 22.5% annually, they will lag behind the broader KR market's growth rate of 28.7%. Revenue is projected to increase by 19.3% per year, outpacing the market's average of 10.3%. Recent presentations at major global conferences highlight ongoing investor engagement and transparency efforts.

- Take a closer look at CLASSYS' potential here in our earnings growth report.

- Our comprehensive valuation report raises the possibility that CLASSYS is priced higher than what may be justified by its financials.

PharmaResearch (KOSDAQ:A214450)

Simply Wall St Growth Rating: ★★★★★☆

Overview: PharmaResearch Co., Ltd., along with its subsidiaries, operates as a biopharmaceutical company primarily in South Korea and has a market cap of ₩1.91 trillion.

Operations: PharmaResearch generates its revenue primarily from its Pharmaceuticals segment, amounting to ₩296.59 billion.

Insider Ownership: 38.9%

Earnings Growth Forecast: 22.2% p.a.

PharmaResearch, a South Korean growth company with high insider ownership, is forecast to see revenue growth of 22.1% annually, outpacing the KR market's 10.3%. Earnings grew by 63.2% last year and are expected to rise significantly by 22.2% per year over the next three years, though slower than the market's 28.7%. Despite recent share price volatility, it trades at a good value—55.8% below its estimated fair value—with analysts predicting a stock price increase of 32.1%.

- Click to explore a detailed breakdown of our findings in PharmaResearch's earnings growth report.

- The valuation report we've compiled suggests that PharmaResearch's current price could be quite moderate.

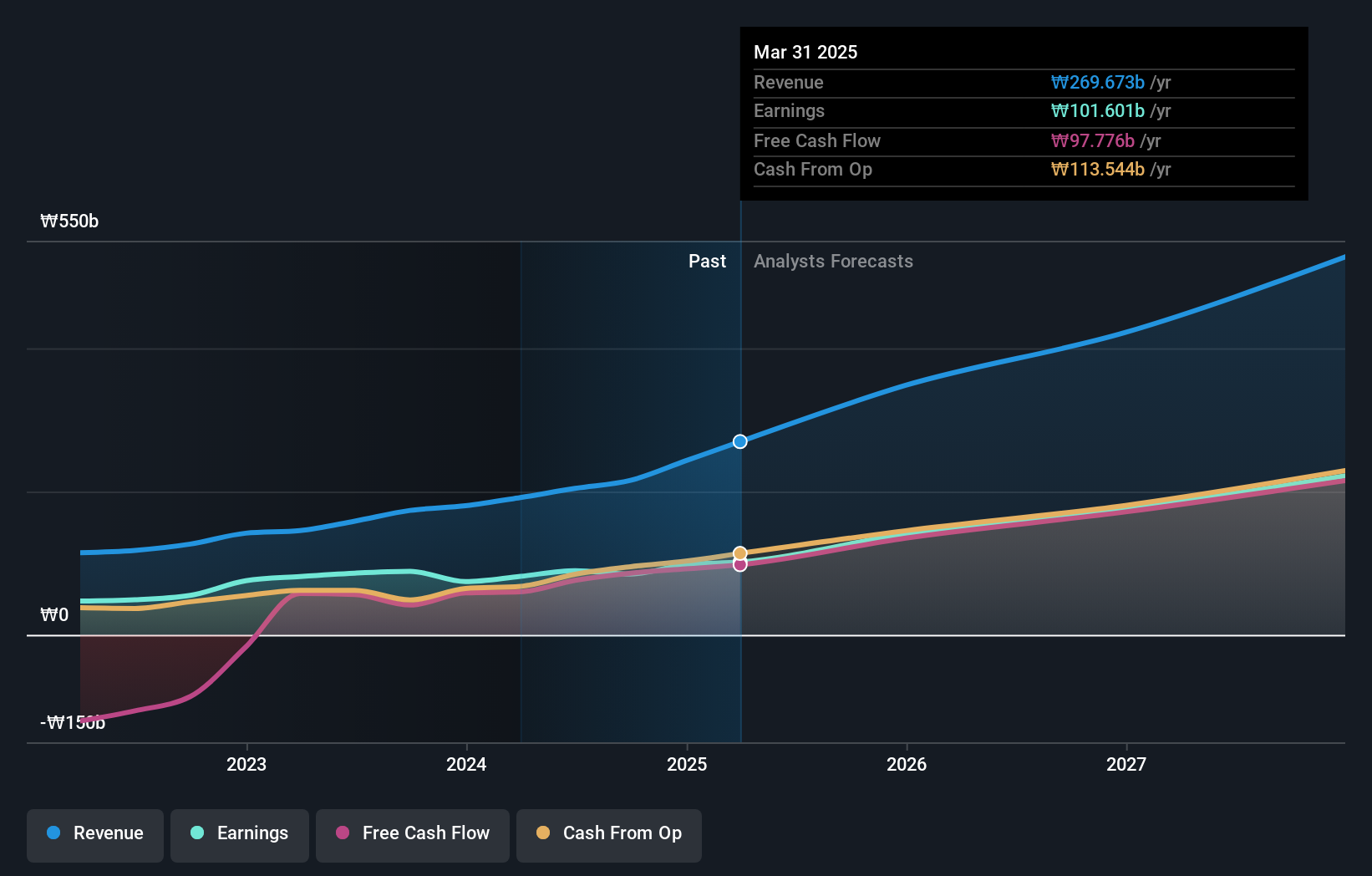

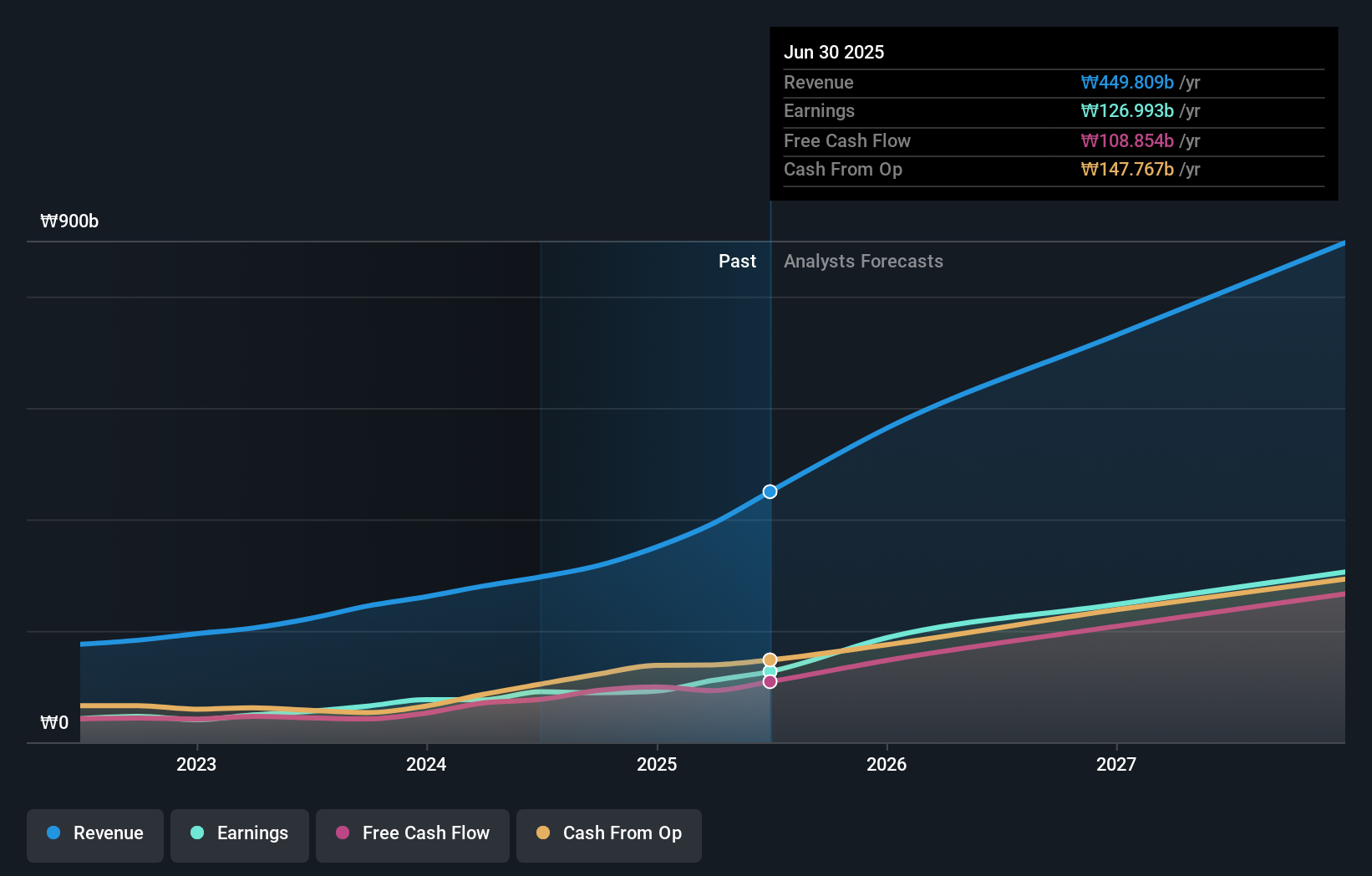

Hyosung Heavy Industries (KOSE:A298040)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hyosung Heavy Industries Corporation manufactures and sells heavy electrical equipment in South Korea and internationally, with a market cap of ₩2.57 trillion.

Operations: The company's revenue segments include Heavy Industry at ₩3.35 trillion and Construction at ₩1.78 trillion.

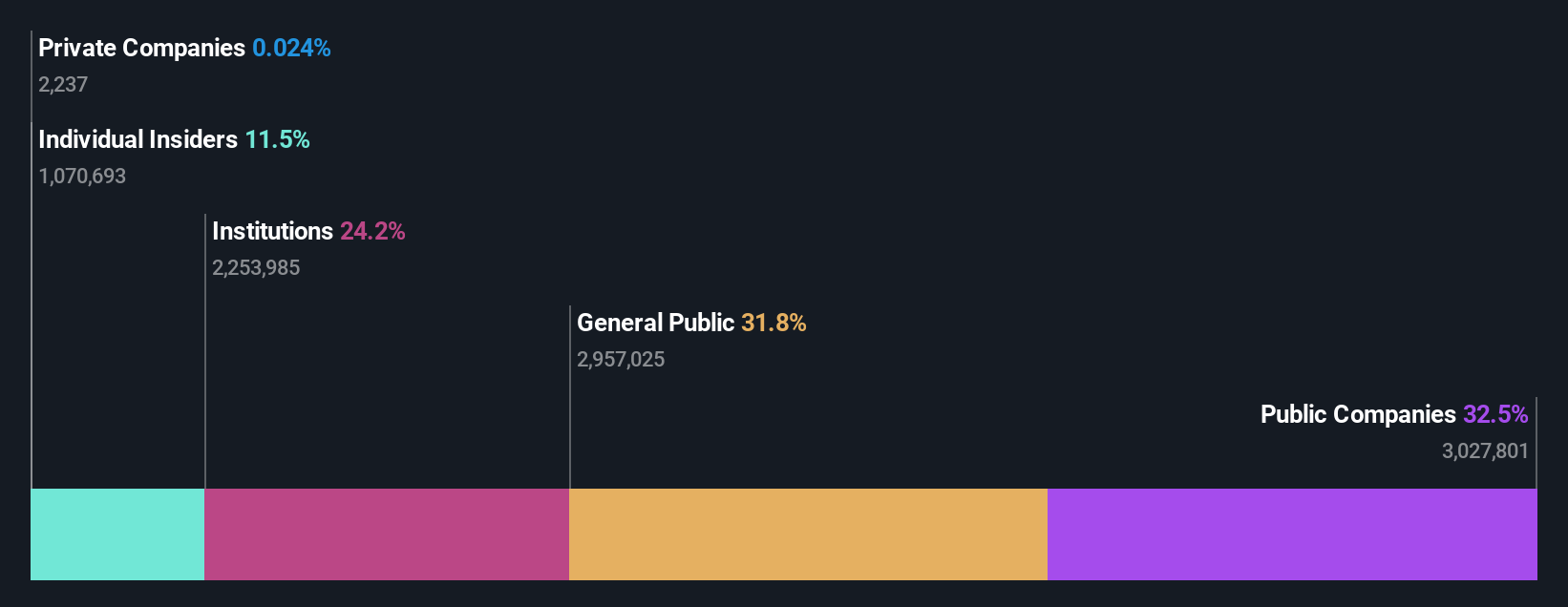

Insider Ownership: 16.4%

Earnings Growth Forecast: 34.7% p.a.

Hyosung Heavy Industries, with significant insider ownership, trades at 60.7% below its estimated fair value. Despite high share price volatility, earnings grew by 117.9% last year and are forecast to rise significantly by 34.66% annually over the next three years, outpacing the KR market's 28.7%. Revenue is expected to grow at 10.7% per year, slightly above the market average of 10.3%, while analysts predict a stock price increase of 48.7%.

- Unlock comprehensive insights into our analysis of Hyosung Heavy Industries stock in this growth report.

- Our valuation report unveils the possibility Hyosung Heavy Industries' shares may be trading at a discount.

Taking Advantage

- Reveal the 88 hidden gems among our Fast Growing KRX Companies With High Insider Ownership screener with a single click here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hyosung Heavy Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A298040

Hyosung Heavy Industries

Manufactures and sells heavy electrical equipment in South Korea and internationally.

Undervalued with high growth potential.