Advertisement

- South Korea

- /

- Medical Equipment

- /

- KOSDAQ:A205470

Humasis (KOSDAQ:205470) Has Debt But No Earnings; Should You Worry?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Humasis Co. Ltd. (KOSDAQ:205470) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Humasis

How Much Debt Does Humasis Carry?

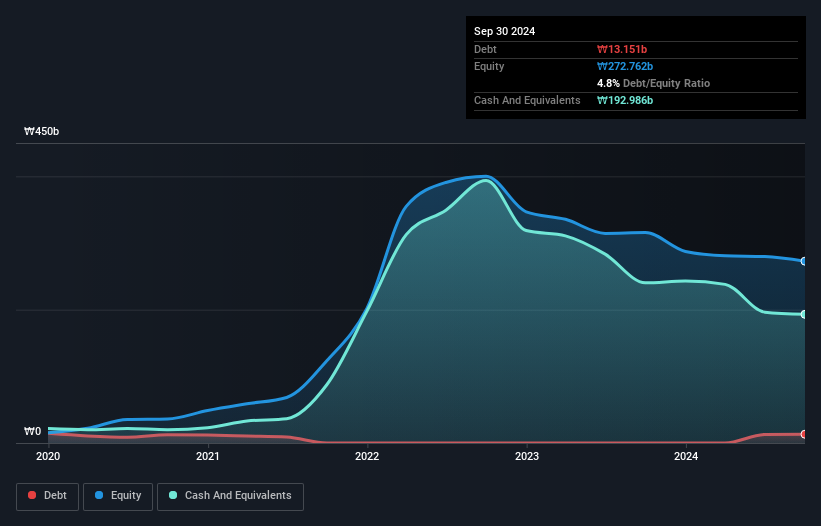

The image below, which you can click on for greater detail, shows that at September 2024 Humasis had debt of ₩13.2b, up from none in one year. However, its balance sheet shows it holds ₩193.0b in cash, so it actually has ₩179.8b net cash.

How Strong Is Humasis' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Humasis had liabilities of ₩80.3b due within 12 months and liabilities of ₩1.44b due beyond that. On the other hand, it had cash of ₩193.0b and ₩8.82b worth of receivables due within a year. So it can boast ₩120.1b more liquid assets than total liabilities.

This surplus liquidity suggests that Humasis' balance sheet could take a hit just as well as Homer Simpson's head can take a punch. With this in mind one could posit that its balance sheet means the company is able to handle some adversity. Simply put, the fact that Humasis has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Humasis's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Humasis's revenue was pretty flat, and it made a negative EBIT. While that's not too bad, we'd prefer see growth.

So How Risky Is Humasis?

While Humasis lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow ₩20b. So taking that on face value, and considering the net cash situation, we don't think that the stock is too risky in the near term. There's no doubt the next few years will be crucial to how the business matures. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example - Humasis has 2 warning signs we think you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Humasis might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A205470

Humasis

Manufactures and sells pharmaceuticals and medical devices in South Korea and internationally.

Excellent balance sheet very low.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor