Advertisement

- South Korea

- /

- Food

- /

- KOSE:A006980

Is It Smart To Buy Woosung Feed Co., Ltd. (KRX:006980) Before It Goes Ex-Dividend?

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Woosung Feed Co., Ltd. (KRX:006980) is about to trade ex-dividend in the next four days. You can purchase shares before the 29th of December in order to receive the dividend, which the company will pay on the 6th of April.

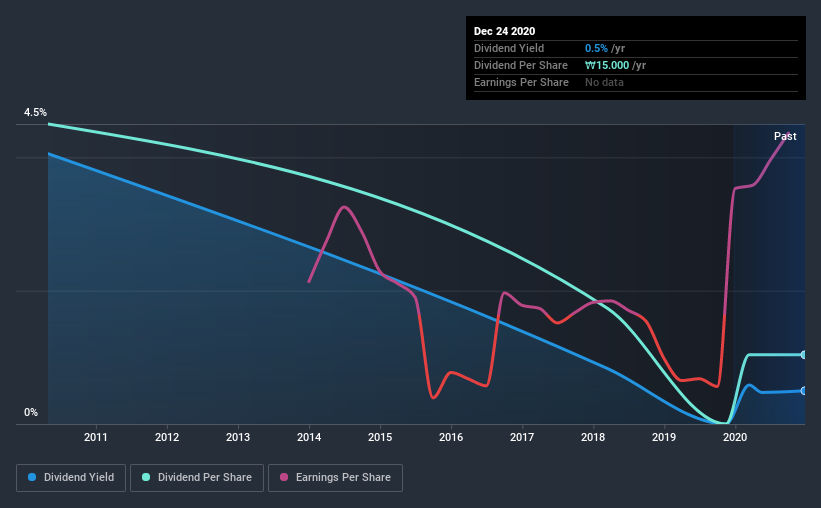

Woosung Feed's next dividend payment will be ₩15.00 per share, on the back of last year when the company paid a total of ₩15.00 to shareholders. Based on the last year's worth of payments, Woosung Feed has a trailing yield of 0.5% on the current stock price of ₩3005. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to investigate whether Woosung Feed can afford its dividend, and if the dividend could grow.

Check out our latest analysis for Woosung Feed

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Woosung Feed paid out just 2.3% of its profit last year, which we think is conservatively low and leaves plenty of margin for unexpected circumstances. A useful secondary check can be to evaluate whether Woosung Feed generated enough free cash flow to afford its dividend. Woosung Feed paid a dividend despite reporting negative free cash flow over the last twelve months. This may be due to heavy investment in the business, but this is still suboptimal from a dividend sustainability perspective.

Click here to see how much of its profit Woosung Feed paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. It's encouraging to see Woosung Feed has grown its earnings rapidly, up 33% a year for the past five years.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Woosung Feed has seen its dividend decline 14% per annum on average over the past 10 years, which is not great to see. It's unusual to see earnings per share increasing at the same time as dividends per share have been in decline. We'd hope it's because the company is reinvesting heavily in its business, but it could also suggest business is lumpy.

To Sum It Up

Should investors buy Woosung Feed for the upcoming dividend? We're glad to see the company has been improving its earnings per share while also paying out a low percentage of income. However, it's not great to see it paying out what we see as an uncomfortably high percentage of its cash flow. It might be worth researching if the company is reinvesting in growth projects that could grow earnings and dividends in the future, but for now we're not all that optimistic on its dividend prospects.

With that in mind, a critical part of thorough stock research is being aware of any risks that stock currently faces. Every company has risks, and we've spotted 2 warning signs for Woosung Feed you should know about.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Woosung Feed, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Woosung might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A006980

Woosung

Woosung Co., Ltd., together with its subsidiaries, mixed feed, real estate rental, and trading businesses in South Korea and internationally.

Proven track record with slight risk.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor