Advertisement

- South Korea

- /

- Food

- /

- KOSE:A004370

Nongshim Co., Ltd. (KRX:004370) Looks Like A Good Stock, And It's Going Ex-Dividend Soon

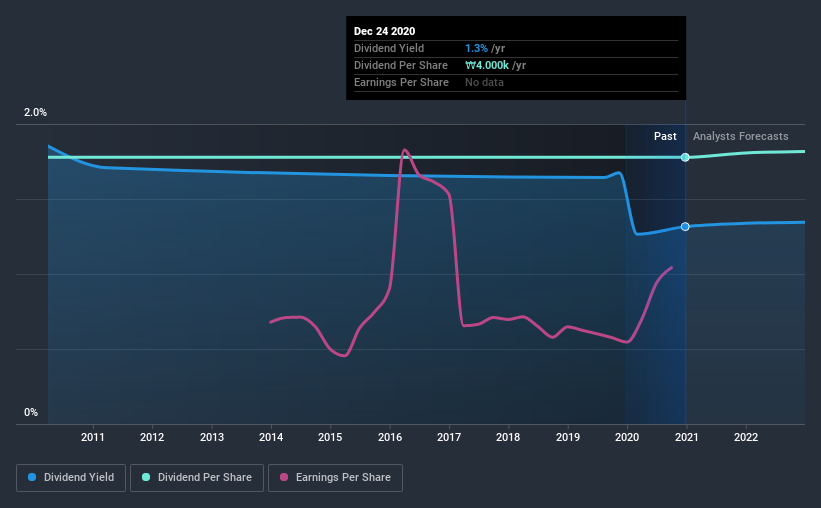

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Nongshim Co., Ltd. (KRX:004370) is about to trade ex-dividend in the next 4 days. If you purchase the stock on or after the 29th of December, you won't be eligible to receive this dividend, when it is paid on the 20th of April.

Nongshim's upcoming dividend is ₩4,000 a share, following on from the last 12 months, when the company distributed a total of ₩4,000 per share to shareholders. Calculating the last year's worth of payments shows that Nongshim has a trailing yield of 1.3% on the current share price of ₩304000. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to investigate whether Nongshim can afford its dividend, and if the dividend could grow.

Check out our latest analysis for Nongshim

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Nongshim is paying out just 17% of its profit after tax, which is comfortably low and leaves plenty of breathing room in the case of adverse events. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. It distributed 40% of its free cash flow as dividends, a comfortable payout level for most companies.

It's positive to see that Nongshim's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. For this reason, we're glad to see Nongshim's earnings per share have risen 16% per annum over the last five years. The company has managed to grow earnings at a rapid rate, while reinvesting most of the profits within the business. This will make it easier to fund future growth efforts and we think this is an attractive combination - plus the dividend can always be increased later.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Nongshim's dividend payments are effectively flat on where they were 10 years ago.

Final Takeaway

Should investors buy Nongshim for the upcoming dividend? Nongshim has been growing earnings at a rapid rate, and has a conservatively low payout ratio, implying that it is reinvesting heavily in its business; a sterling combination. Overall we think this is an attractive combination and worthy of further research.

Ever wonder what the future holds for Nongshim? See what the 16 analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

When trading Nongshim or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Nongshim might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A004370

Nongshim

Manufactures, sells, imports, and exports ramen, snacks, and beverages in Asia, the Americas, Europe, and Oceania.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative