Advertisement

- South Korea

- /

- Food

- /

- KOSE:A003230

Samyang Foods Co., Ltd.'s (KRX:003230) 34% Jump Shows Its Popularity With Investors

Despite an already strong run, Samyang Foods Co., Ltd. (KRX:003230) shares have been powering on, with a gain of 34% in the last thirty days. The last 30 days were the cherry on top of the stock's 528% gain in the last year, which is nothing short of spectacular.

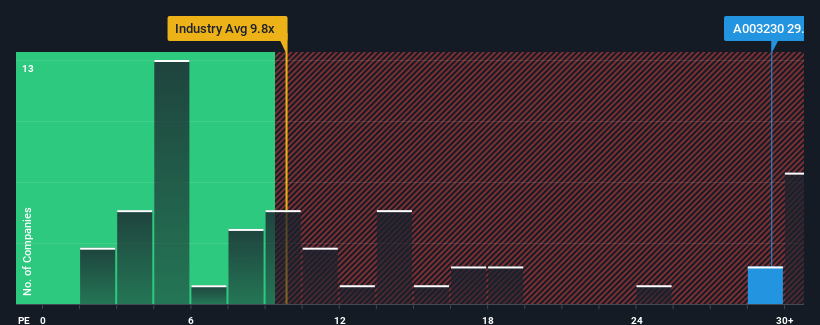

After such a large jump in price, Samyang Foods' price-to-earnings (or "P/E") ratio of 29.4x might make it look like a strong sell right now compared to the market in Korea, where around half of the companies have P/E ratios below 12x and even P/E's below 7x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Recent times have been pleasing for Samyang Foods as its earnings have risen in spite of the market's earnings going into reverse. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for Samyang Foods

What Are Growth Metrics Telling Us About The High P/E?

The only time you'd be truly comfortable seeing a P/E as steep as Samyang Foods' is when the company's growth is on track to outshine the market decidedly.

Taking a look back first, we see that the company grew earnings per share by an impressive 104% last year. Pleasingly, EPS has also lifted 197% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Shifting to the future, estimates from the six analysts covering the company suggest earnings should grow by 24% each year over the next three years. With the market only predicted to deliver 20% each year, the company is positioned for a stronger earnings result.

With this information, we can see why Samyang Foods is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

Samyang Foods' P/E is flying high just like its stock has during the last month. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Samyang Foods' analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

Plus, you should also learn about this 1 warning sign we've spotted with Samyang Foods.

You might be able to find a better investment than Samyang Foods. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A003230

Samyang Foods

Engages in the food business in South Korea and internationally.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor