Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies F&F Co., Ltd. (KRX:007700) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for F&F

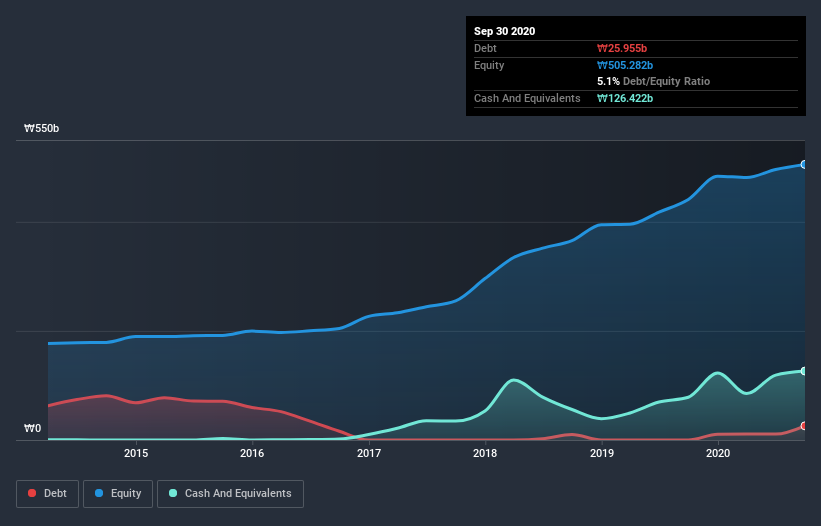

How Much Debt Does F&F Carry?

You can click the graphic below for the historical numbers, but it shows that as of September 2020 F&F had ₩26.0b of debt, an increase on none, over one year. However, its balance sheet shows it holds ₩126.4b in cash, so it actually has ₩100.5b net cash.

A Look At F&F's Liabilities

Zooming in on the latest balance sheet data, we can see that F&F had liabilities of ₩153.5b due within 12 months and liabilities of ₩38.4b due beyond that. Offsetting this, it had ₩126.4b in cash and ₩63.8b in receivables that were due within 12 months. So its total liabilities are just about perfectly matched by its shorter-term, liquid assets.

Having regard to F&F's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the ₩1.57t company is struggling for cash, we still think it's worth monitoring its balance sheet. While it does have liabilities worth noting, F&F also has more cash than debt, so we're pretty confident it can manage its debt safely.

Fortunately, F&F grew its EBIT by 2.9% in the last year, making that debt load look even more manageable. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine F&F's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. F&F may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Looking at the most recent three years, F&F recorded free cash flow of 43% of its EBIT, which is weaker than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing up

We could understand if investors are concerned about F&F's liabilities, but we can be reassured by the fact it has has net cash of ₩100.5b. And it also grew its EBIT by 2.9% over the last year. So we don't have any problem with F&F's use of debt. Over time, share prices tend to follow earnings per share, so if you're interested in F&F, you may well want to click here to check an interactive graph of its earnings per share history.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you’re looking to trade F&F, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A007700

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor