Advertisement

- South Korea

- /

- Commercial Services

- /

- KOSE:A051600

KEPCO Plant Service & Engineering Co.,Ltd.'s (KRX:051600) Has Been On A Rise But Financial Prospects Look Weak: Is The Stock Overpriced?

KEPCO Plant Service & EngineeringLtd's (KRX:051600) stock is up by a considerable 6.2% over the past month. However, we decided to pay close attention to its weak financials as we are doubtful that the current momentum will keep up, given the scenario. Specifically, we decided to study KEPCO Plant Service & EngineeringLtd's ROE in this article.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

View our latest analysis for KEPCO Plant Service & EngineeringLtd

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for KEPCO Plant Service & EngineeringLtd is:

12% = ₩121b ÷ ₩1.0t (Based on the trailing twelve months to September 2020).

The 'return' is the amount earned after tax over the last twelve months. So, this means that for every ₩1 of its shareholder's investments, the company generates a profit of ₩0.12.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

KEPCO Plant Service & EngineeringLtd's Earnings Growth And 12% ROE

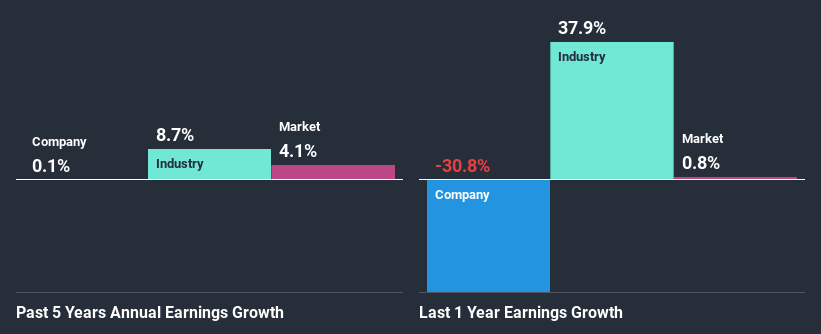

At first glance, KEPCO Plant Service & EngineeringLtd's ROE doesn't look very promising. However, given that the company's ROE is similar to the average industry ROE of 12%, we may spare it some thought. Having said that, KEPCO Plant Service & EngineeringLtd's net income growth over the past five years is more or less flat. Bear in mind, the company's ROE is not very high. So that could also be one of the reasons behind the company's flat growth in earnings.

As a next step, we compared KEPCO Plant Service & EngineeringLtd's net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 8.7% in the same period.

Earnings growth is a huge factor in stock valuation. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. Has the market priced in the future outlook for A051600? You can find out in our latest intrinsic value infographic research report.

Is KEPCO Plant Service & EngineeringLtd Using Its Retained Earnings Effectively?

With a high three-year median payout ratio of 54% (implying that the company keeps only 46% of its income) of its business to reinvest into its business), most of KEPCO Plant Service & EngineeringLtd's profits are being paid to shareholders, which explains the absence of growth in earnings.

Moreover, KEPCO Plant Service & EngineeringLtd has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 50%. Accordingly, forecasts suggest that KEPCO Plant Service & EngineeringLtd's future ROE will be 13% which is again, similar to the current ROE.

Conclusion

On the whole, KEPCO Plant Service & EngineeringLtd's performance is quite a big let-down. As a result of its low ROE and lack of mich reinvestment into the business, the company has seen a disappointing earnings growth rate. With that said, the latest industry analyst forecasts reveal that the company's earnings are expected to accelerate. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you’re looking to trade KEPCO Plant Service & EngineeringLtd, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if KEPCO Plant Service & EngineeringLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KOSE:A051600

KEPCO Plant Service & EngineeringLtd

KEPCO Plant Service & Engineering Co.,Ltd.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative