Advertisement

- South Korea

- /

- Commercial Services

- /

- KOSDAQ:A063570

How Does NICE Total Cash Management Co., Ltd (KOSDAQ:063570) Fare As A Dividend Stock?

Today we'll take a closer look at NICE Total Cash Management Co., Ltd (KOSDAQ:063570) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. On the other hand, investors have been known to buy a stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

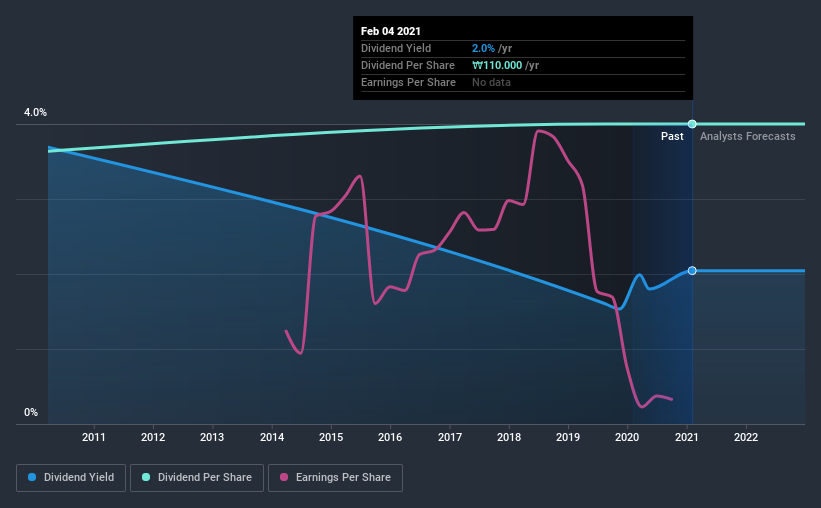

While NICE Total Cash Management's 2.0% dividend yield is not the highest, we think its lengthy payment history is quite interesting. Some simple research can reduce the risk of buying NICE Total Cash Management for its dividend - read on to learn more.

Explore this interactive chart for our latest analysis on NICE Total Cash Management!

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. As a result, we should always investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax. NICE Total Cash Management paid out 167% of its profit as dividends, over the trailing twelve month period. Unless there are extenuating circumstances, from the perspective of an investor who hopes to own the company for many years, a payout ratio of above 100% is definitely a concern.

We also measure dividends paid against a company's levered free cash flow, to see if enough cash was generated to cover the dividend. Unfortunately, while NICE Total Cash Management pays a dividend, it also reported negative free cash flow last year. While there may be a good reason for this, it's not ideal from a dividend perspective.

Consider getting our latest analysis on NICE Total Cash Management's financial position here.

Dividend Volatility

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. For the purpose of this article, we only scrutinise the last decade of NICE Total Cash Management's dividend payments. The dividend has been stable over the past 10 years, which is great. We think this could suggest some resilience to the business and its dividends. During the past 10-year period, the first annual payment was ₩100 in 2011, compared to ₩110 last year. Dividend payments have grown at less than 1% a year over this period.

Slow and steady dividend growth might not sound that exciting, but dividends have been stable for ten years, which we think is seriously impressive.

Dividend Growth Potential

While dividend payments have been relatively reliable, it would also be nice if earnings per share (EPS) were growing, as this is essential to maintaining the dividend's purchasing power over the long term. NICE Total Cash Management's EPS have fallen by approximately 27% per year during the past five years. With this kind of significant decline, we always wonder what has changed in the business. Dividends are about stability, and NICE Total Cash Management's earnings per share, which support the dividend, have been anything but stable.

Conclusion

To summarise, shareholders should always check that NICE Total Cash Management's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. NICE Total Cash Management paid out almost all of its cash flow and profit as dividends, leaving little to reinvest in the business. Second, earnings per share have actually shrunk, but at least the dividends have been relatively stable. In this analysis, NICE Total Cash Management doesn't shape up too well as a dividend stock. We'd find it hard to look past the flaws, and would not be inclined to think of it as a reliable dividend-payer.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. To that end, NICE Total Cash Management has 4 warning signs (and 1 which is potentially serious) we think you should know about.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

If you decide to trade NICE Total Cash Management, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if NICE Infra might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A063570

NICE Infra

Engages in the operation and management of unmanned systems in South Korea.

Slight with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor