Advertisement

- South Korea

- /

- Commercial Services

- /

- KOSDAQ:A049720

Koryo Credit Information (KOSDAQ:049720) Has A Pretty Healthy Balance Sheet

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Koryo Credit Information Co., Ltd. (KOSDAQ:049720) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Koryo Credit Information

What Is Koryo Credit Information's Net Debt?

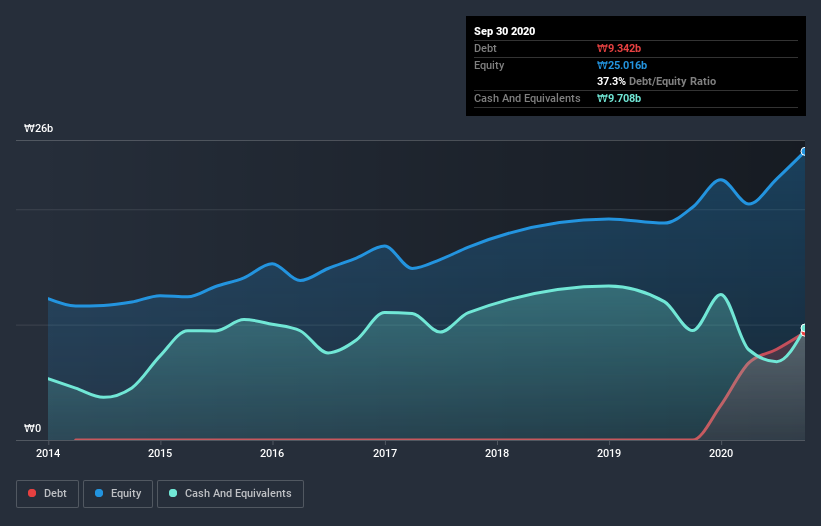

As you can see below, at the end of September 2020, Koryo Credit Information had ₩9.34b of debt, up from none a year ago. Click the image for more detail. However, its balance sheet shows it holds ₩9.71b in cash, so it actually has ₩365.8m net cash.

A Look At Koryo Credit Information's Liabilities

The latest balance sheet data shows that Koryo Credit Information had liabilities of ₩23.5b due within a year, and liabilities of ₩11.2b falling due after that. Offsetting this, it had ₩9.71b in cash and ₩7.97b in receivables that were due within 12 months. So it has liabilities totalling ₩17.0b more than its cash and near-term receivables, combined.

Koryo Credit Information has a market capitalization of ₩84.1b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. While it does have liabilities worth noting, Koryo Credit Information also has more cash than debt, so we're pretty confident it can manage its debt safely.

Another good sign is that Koryo Credit Information has been able to increase its EBIT by 23% in twelve months, making it easier to pay down debt. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Koryo Credit Information will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Koryo Credit Information may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Koryo Credit Information produced sturdy free cash flow equating to 51% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Summing up

While Koryo Credit Information does have more liabilities than liquid assets, it also has net cash of ₩365.8m. And it impressed us with its EBIT growth of 23% over the last year. So we don't think Koryo Credit Information's use of debt is risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 2 warning signs we've spotted with Koryo Credit Information (including 1 which is is potentially serious) .

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade Koryo Credit Information, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Koryo Credit Information might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KOSDAQ:A049720

Koryo Credit Information

Engages in the debt collection/credit investigation/civil complaint agency business in South Korea and internationally.

Outstanding track record with flawless balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.7% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor