- South Korea

- /

- Machinery

- /

- KOSE:A011700

Health Check: How Prudently Does Hanshin Machinery (KRX:011700) Use Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Hanshin Machinery Co., Ltd. (KRX:011700) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Hanshin Machinery

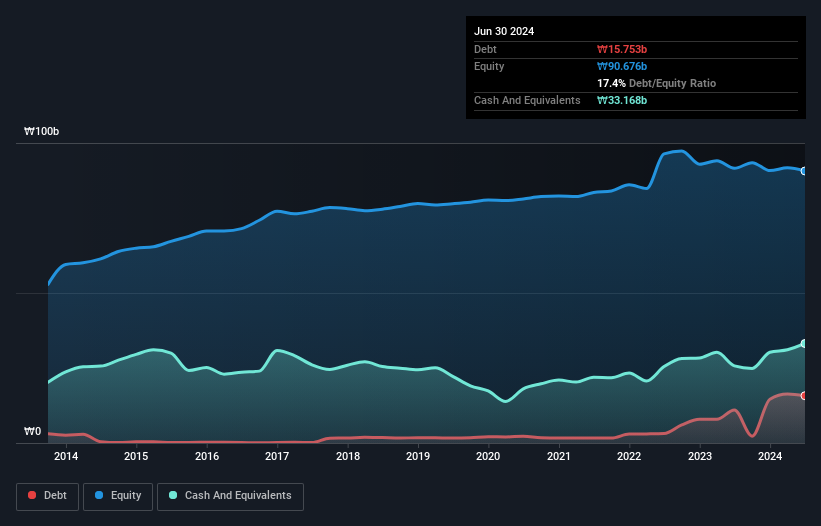

How Much Debt Does Hanshin Machinery Carry?

The image below, which you can click on for greater detail, shows that at June 2024 Hanshin Machinery had debt of ₩15.8b, up from ₩11.0b in one year. However, it does have ₩33.2b in cash offsetting this, leading to net cash of ₩17.4b.

How Healthy Is Hanshin Machinery's Balance Sheet?

The latest balance sheet data shows that Hanshin Machinery had liabilities of ₩22.1b due within a year, and liabilities of ₩8.87b falling due after that. Offsetting this, it had ₩33.2b in cash and ₩24.0b in receivables that were due within 12 months. So it can boast ₩26.2b more liquid assets than total liabilities.

This excess liquidity suggests that Hanshin Machinery is taking a careful approach to debt. Because it has plenty of assets, it is unlikely to have trouble with its lenders. Succinctly put, Hanshin Machinery boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Hanshin Machinery will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Hanshin Machinery saw its revenue hold pretty steady, and it did not report positive earnings before interest and tax. While that's not too bad, we'd prefer see growth.

So How Risky Is Hanshin Machinery?

Although Hanshin Machinery had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of ₩5.1b. So taking that on face value, and considering the net cash situation, we don't think that the stock is too risky in the near term. With mediocre revenue growth in the last year, we're don't find the investment opportunity particularly compelling. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for Hanshin Machinery (of which 1 is potentially serious!) you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Hanshin Machinery might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A011700

Hanshin Machinery

Manufactures and sells air compressors in Korea and internationally.

Mediocre balance sheet low.