The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Bumyang Construction Co.,Ltd. (KRX:002410) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Bumyang ConstructionLtd

How Much Debt Does Bumyang ConstructionLtd Carry?

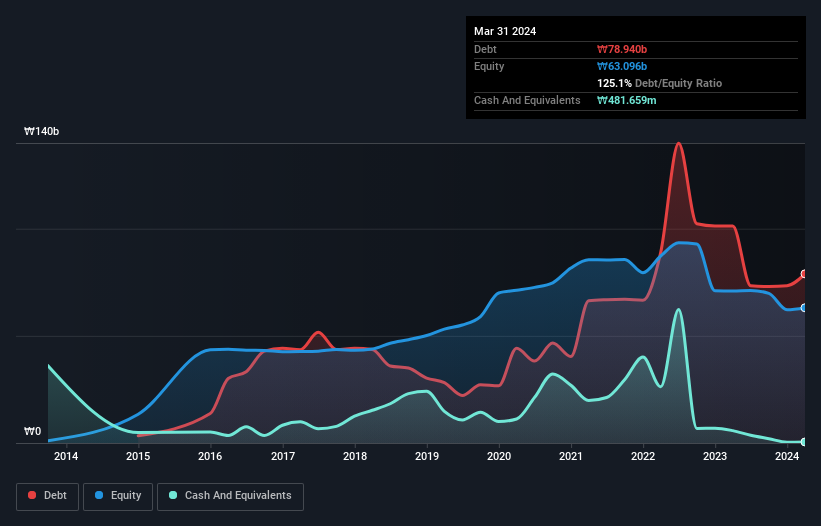

You can click the graphic below for the historical numbers, but it shows that Bumyang ConstructionLtd had ₩78.9b of debt in March 2024, down from ₩101.3b, one year before. And it doesn't have much cash, so its net debt is about the same.

How Healthy Is Bumyang ConstructionLtd's Balance Sheet?

According to the last reported balance sheet, Bumyang ConstructionLtd had liabilities of ₩118.4b due within 12 months, and liabilities of ₩17.9b due beyond 12 months. On the other hand, it had cash of ₩481.7m and ₩38.9b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₩96.9b.

The deficiency here weighs heavily on the ₩34.9b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. At the end of the day, Bumyang ConstructionLtd would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Bumyang ConstructionLtd's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Bumyang ConstructionLtd reported revenue of ₩131b, which is a gain of 20%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

Caveat Emptor

Despite the top line growth, Bumyang ConstructionLtd still had an earnings before interest and tax (EBIT) loss over the last year. Its EBIT loss was a whopping ₩12b. If you consider the significant liabilities mentioned above, we are extremely wary of this investment. That said, it is possible that the company will turn its fortunes around. But we think that is unlikely, given it is low on liquid assets, and burned through ₩9.5b in the last year. So we think this stock is risky, like walking through a dirty dog park with a mask on. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example Bumyang ConstructionLtd has 3 warning signs (and 2 which are a bit unpleasant) we think you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Bumyang ConstructionLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A002410

Bumyang ConstructionLtd

Engages in the housing construction, civil engineering construction, water heating construction contract businesses in South Korea.

Low with worrying balance sheet.

Market Insights

Community Narratives