Advertisement

- South Korea

- /

- Construction

- /

- KOSE:A000720

Slowing Rates Of Return At Hyundai Engineering & ConstructionLtd (KRX:000720) Leave Little Room For Excitement

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. However, after investigating Hyundai Engineering & ConstructionLtd (KRX:000720), we don't think it's current trends fit the mold of a multi-bagger.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Hyundai Engineering & ConstructionLtd is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

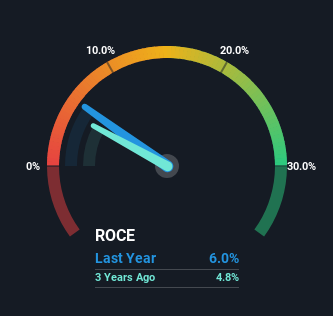

0.06 = ₩823b ÷ (₩25t - ₩11t) (Based on the trailing twelve months to June 2024).

Therefore, Hyundai Engineering & ConstructionLtd has an ROCE of 6.0%. Even though it's in line with the industry average of 6.4%, it's still a low return by itself.

Check out our latest analysis for Hyundai Engineering & ConstructionLtd

In the above chart we have measured Hyundai Engineering & ConstructionLtd's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Hyundai Engineering & ConstructionLtd for free.

The Trend Of ROCE

The returns on capital haven't changed much for Hyundai Engineering & ConstructionLtd in recent years. The company has employed 20% more capital in the last five years, and the returns on that capital have remained stable at 6.0%. This poor ROCE doesn't inspire confidence right now, and with the increase in capital employed, it's evident that the business isn't deploying the funds into high return investments.

Another thing to note, Hyundai Engineering & ConstructionLtd has a high ratio of current liabilities to total assets of 45%. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

The Bottom Line

Long story short, while Hyundai Engineering & ConstructionLtd has been reinvesting its capital, the returns that it's generating haven't increased. And in the last five years, the stock has given away 28% so the market doesn't look too hopeful on these trends strengthening any time soon. On the whole, we aren't too inspired by the underlying trends and we think there may be better chances of finding a multi-bagger elsewhere.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 2 warning signs for Hyundai Engineering & ConstructionLtd (of which 1 is significant!) that you should know about.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if Hyundai Engineering & ConstructionLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A000720

Hyundai Engineering & ConstructionLtd

Hyundai Engineering & Construction Co.,Ltd.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor