- South Korea

- /

- Electrical

- /

- KOSDAQ:A160190

More Unpleasant Surprises Could Be In Store For HIGEN Motor Co., Ltd.'s (KOSDAQ:160190) Shares After Tumbling 27%

HIGEN Motor Co., Ltd. (KOSDAQ:160190) shares have retraced a considerable 27% in the last month, reversing a fair amount of their solid recent performance. To make matters worse, the recent drop has wiped out a year's worth of gains with the share price now back where it started a year ago.

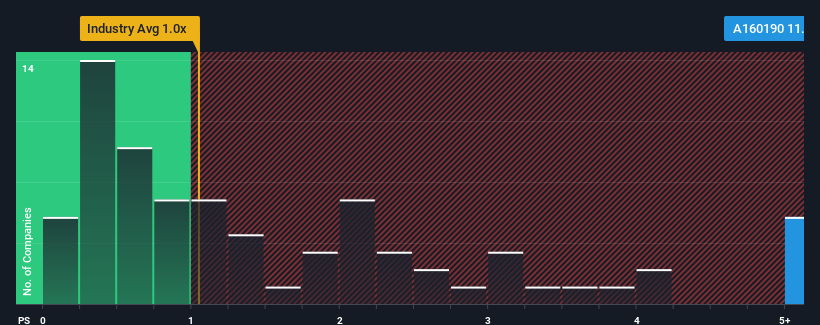

Even after such a large drop in price, when almost half of the companies in Korea's Electrical industry have price-to-sales ratios (or "P/S") below 1x, you may still consider HIGEN Motor as a stock not worth researching with its 11.2x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for HIGEN Motor

How HIGEN Motor Has Been Performing

As an illustration, revenue has deteriorated at HIGEN Motor over the last year, which is not ideal at all. One possibility is that the P/S is high because investors think the company will still do enough to outperform the broader industry in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Although there are no analyst estimates available for HIGEN Motor, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The High P/S Ratio?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like HIGEN Motor's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 3.9% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 9.9% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Weighing that medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 6.0% shows it's an unpleasant look.

With this in mind, we find it worrying that HIGEN Motor's P/S exceeds that of its industry peers. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

The Key Takeaway

A significant share price dive has done very little to deflate HIGEN Motor's very lofty P/S. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that HIGEN Motor currently trades on a much higher than expected P/S since its recent revenues have been in decline over the medium-term. When we see revenue heading backwards and underperforming the industry forecasts, we feel the possibility of the share price declining is very real, bringing the P/S back into the realm of reasonability. Should recent medium-term revenue trends persist, it would pose a significant risk to existing shareholders' investments and prospective investors will have a hard time accepting the current value of the stock.

You need to take note of risks, for example - HIGEN Motor has 3 warning signs (and 2 which are concerning) we think you should know about.

If you're unsure about the strength of HIGEN Motor's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if HIGEN Motor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A160190

Adequate balance sheet very low.

Market Insights

Community Narratives