Advertisement

- South Korea

- /

- Machinery

- /

- KOSDAQ:A101170

Earnings Not Telling The Story For WOORIM POWER TRAIN SOLUTION Co., Ltd. (KOSDAQ:101170) After Shares Rise 43%

The WOORIM POWER TRAIN SOLUTION Co., Ltd. (KOSDAQ:101170) share price has done very well over the last month, posting an excellent gain of 43%. Taking a wider view, although not as strong as the last month, the full year gain of 18% is also fairly reasonable.

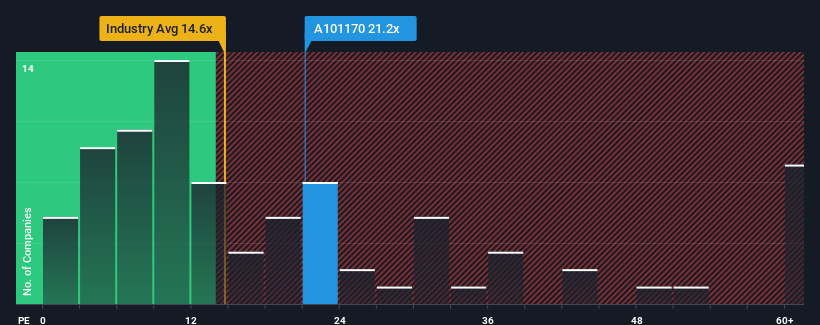

Since its price has surged higher, given close to half the companies in Korea have price-to-earnings ratios (or "P/E's") below 12x, you may consider WOORIM POWER TRAIN SOLUTION as a stock to avoid entirely with its 21.2x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Recent times haven't been advantageous for WOORIM POWER TRAIN SOLUTION as its earnings have been falling quicker than most other companies. It might be that many expect the dismal earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for WOORIM POWER TRAIN SOLUTION

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like WOORIM POWER TRAIN SOLUTION's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 11% decrease to the company's bottom line. At least EPS has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Turning to the outlook, the next year should generate growth of 25% as estimated by the lone analyst watching the company. With the market predicted to deliver 33% growth , the company is positioned for a weaker earnings result.

In light of this, it's alarming that WOORIM POWER TRAIN SOLUTION's P/E sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Final Word

The strong share price surge has got WOORIM POWER TRAIN SOLUTION's P/E rushing to great heights as well. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of WOORIM POWER TRAIN SOLUTION's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with WOORIM POWER TRAIN SOLUTION (at least 1 which makes us a bit uncomfortable), and understanding these should be part of your investment process.

Of course, you might also be able to find a better stock than WOORIM POWER TRAIN SOLUTION. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if WOORIM POWER TRAIN SOLUTION might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A101170

WOORIM POWER TRAIN SOLUTION

Manufactures and sells transmissions, reducers, gears, and wind power generator parts primarily in South Korea.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor