Advertisement

- South Korea

- /

- Machinery

- /

- KOSDAQ:A086670

Don't Race Out To Buy BMT Co., Ltd. (KOSDAQ:086670) Just Because It's Going Ex-Dividend

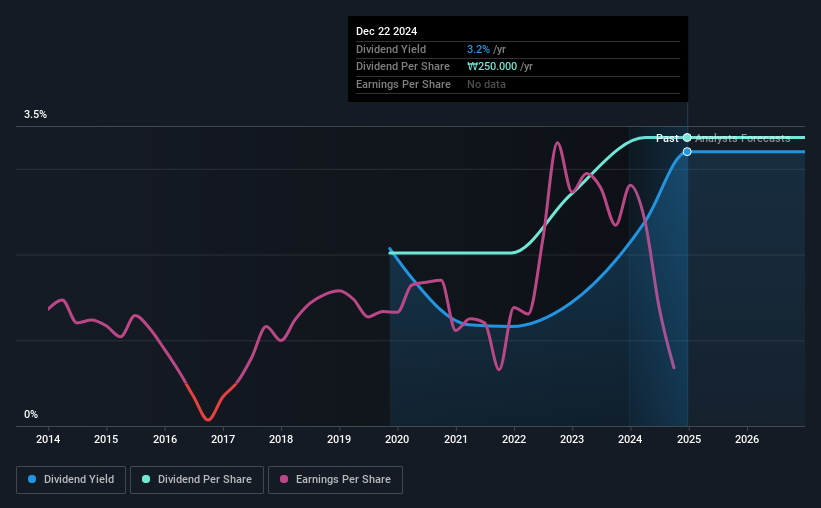

Readers hoping to buy BMT Co., Ltd. (KOSDAQ:086670) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. Therefore, if you purchase BMT's shares on or after the 27th of December, you won't be eligible to receive the dividend, when it is paid on the 8th of April.

The company's next dividend payment will be ₩250.00 per share, on the back of last year when the company paid a total of ₩250 to shareholders. Calculating the last year's worth of payments shows that BMT has a trailing yield of 3.2% on the current share price of ₩7810.00. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to investigate whether BMT can afford its dividend, and if the dividend could grow.

Check out our latest analysis for BMT

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. BMT distributed an unsustainably high 174% of its profit as dividends to shareholders last year. Without extenuating circumstances, we'd consider the dividend at risk of a cut. A useful secondary check can be to evaluate whether BMT generated enough free cash flow to afford its dividend. Over the past year it paid out 167% of its free cash flow as dividends, which is uncomfortably high. We're curious about why the company paid out more cash than it generated last year, since this can be one of the early signs that a dividend may be unsustainable.

Cash is slightly more important than profit from a dividend perspective, but given BMT's payments were not well covered by either earnings or cash flow, we are concerned about the sustainability of this dividend.

Click here to see how much of its profit BMT paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. BMT's earnings have collapsed faster than Wile E Coyote's schemes to trap the Road Runner; down a tremendous 30% a year over the past five years.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the last five years, BMT has lifted its dividend by approximately 11% a year on average. The only way to pay higher dividends when earnings are shrinking is either to pay out a larger percentage of profits, spend cash from the balance sheet, or borrow the money. BMT is already paying out a high percentage of its income, so without earnings growth, we're doubtful of whether this dividend will grow much in the future.

The Bottom Line

Is BMT worth buying for its dividend? Not only are earnings per share declining, but BMT is paying out an uncomfortably high percentage of both its earnings and cashflow to shareholders as dividends. This is a starkly negative combination that often suggests a dividend cut could be in the company's near future. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

With that being said, if you're still considering BMT as an investment, you'll find it beneficial to know what risks this stock is facing. Every company has risks, and we've spotted 5 warning signs for BMT (of which 2 shouldn't be ignored!) you should know about.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if BMT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A086670

BMT

Manufactures and sells industrial fittings and valves for various industrial fields in South Korea and internationally.

Second-rate dividend payer low.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor