- South Korea

- /

- Machinery

- /

- KOSDAQ:A024880

Korea Parts & Fasteners Co.,Ltd's (KOSDAQ:024880) Share Price Boosted 29% But Its Business Prospects Need A Lift Too

Korea Parts & Fasteners Co.,Ltd (KOSDAQ:024880) shareholders would be excited to see that the share price has had a great month, posting a 29% gain and recovering from prior weakness. Longer-term shareholders would be thankful for the recovery in the share price since it's now virtually flat for the year after the recent bounce.

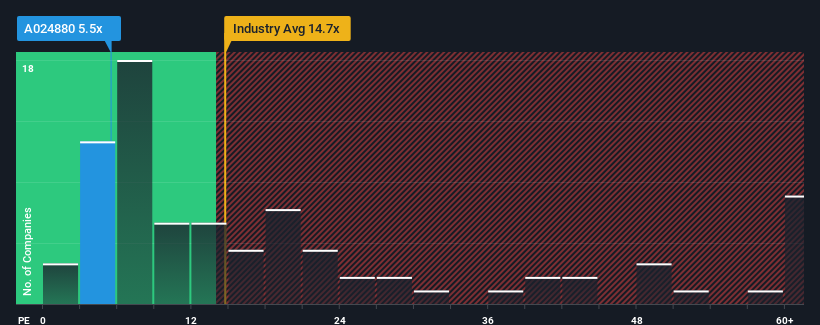

Although its price has surged higher, Korea Parts & FastenersLtd may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 5.5x, since almost half of all companies in Korea have P/E ratios greater than 14x and even P/E's higher than 28x are not unusual. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

For example, consider that Korea Parts & FastenersLtd's financial performance has been poor lately as its earnings have been in decline. It might be that many expect the disappointing earnings performance to continue or accelerate, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Korea Parts & FastenersLtd

Does Growth Match The Low P/E?

In order to justify its P/E ratio, Korea Parts & FastenersLtd would need to produce anemic growth that's substantially trailing the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 28%. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 30% shows it's noticeably less attractive on an annualised basis.

With this information, we can see why Korea Parts & FastenersLtd is trading at a P/E lower than the market. It seems most investors are expecting to see the recent limited growth rates continue into the future and are only willing to pay a reduced amount for the stock.

The Final Word

Shares in Korea Parts & FastenersLtd are going to need a lot more upward momentum to get the company's P/E out of its slump. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Korea Parts & FastenersLtd revealed its three-year earnings trends are contributing to its low P/E, given they look worse than current market expectations. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

We don't want to rain on the parade too much, but we did also find 4 warning signs for Korea Parts & FastenersLtd (1 shouldn't be ignored!) that you need to be mindful of.

If these risks are making you reconsider your opinion on Korea Parts & FastenersLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

If you're looking to trade Korea Parts & FastenersLtd, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Korea Parts & FastenersLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A024880

Korea Parts & FastenersLtd

Manufactures and sells fasteners and automotive parts in South Korea and internationally.

Reasonable growth potential with proven track record.

Market Insights

Community Narratives