Advertisement

- South Korea

- /

- Auto Components

- /

- KOSDAQ:A215360

Woory Industrial Co., Ltd.'s (KOSDAQ:215360) Stock Is Rallying But Financials Look Ambiguous: Will The Momentum Continue?

Most readers would already be aware that Woory Industrial's (KOSDAQ:215360) stock increased significantly by 6.6% over the past month. However, we decided to pay attention to the company's fundamentals which don't appear to give a clear sign about the company's financial health. Particularly, we will be paying attention to Woory Industrial's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Put another way, it reveals the company's success at turning shareholder investments into profits.

See our latest analysis for Woory Industrial

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Woory Industrial is:

4.1% = ₩4.8b ÷ ₩117b (Based on the trailing twelve months to June 2020).

The 'return' refers to a company's earnings over the last year. Another way to think of that is that for every ₩1 worth of equity, the company was able to earn ₩0.04 in profit.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Woory Industrial's Earnings Growth And 4.1% ROE

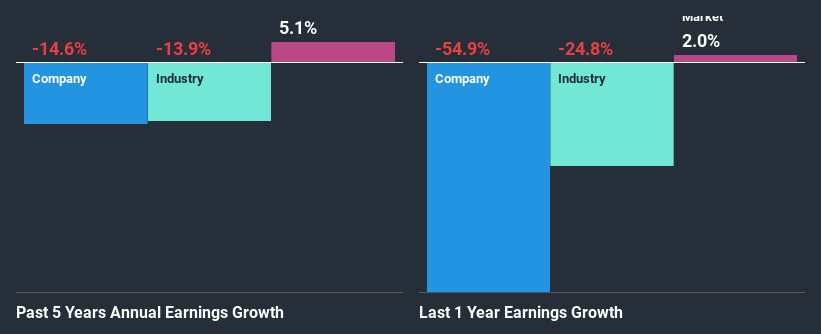

As you can see, Woory Industrial's ROE looks pretty weak. Further, we noted that the company's ROE is similar to the industry average of 4.2%. Given the circumstances, the significant decline in net income by 15% seen by Woory Industrial over the last five years is not surprising.

Next, on comparing with the industry net income growth, we found that Woory Industrial's earnings seems to be shrinking at a similar rate as the industry which shrunk at a rate of a rate of 14% in the same period.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. If you're wondering about Woory Industrial's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Woory Industrial Using Its Retained Earnings Effectively?

Woory Industrial's low three-year median payout ratio of 15% (or a retention ratio of 85%) over the last three years should mean that the company is retaining most of its earnings to fuel its growth but the company's earnings have actually shrunk. The low payout should mean that the company is retaining most of its earnings and consequently, should see some growth. So there could be some other explanations in that regard. For example, the company's business may be deteriorating.

Only recently, Woory Industrial stated paying a dividend. This likely means that the management might have concluded that its shareholders have a strong preference for dividends. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to drop to 7.7% over the next three years. As a result, the expected drop in Woory Industrial's payout ratio explains the anticipated rise in the company's future ROE to 12%, over the same period.

Summary

In total, we're a bit ambivalent about Woory Industrial's performance. While the company does have a high rate of profit retention, its low rate of return is probably hampering its earnings growth. With that said, we studied the latest analyst forecasts and found that while the company has shrunk its earnings in the past, analysts expect its earnings to grow in the future. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

If you decide to trade Woory Industrial, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Woory Industrial might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KOSDAQ:A215360

Woory Industrial

Manufactures and sells automotive parts and components for IC and electric engines in South Korea and internationally.

Adequate balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor