Advertisement

NIKKON Holdings Co.,Ltd.'s (TSE:9072) investors are due to receive a payment of ¥37.00 per share on 12th of December. The yield is still above the industry average at 2.3%.

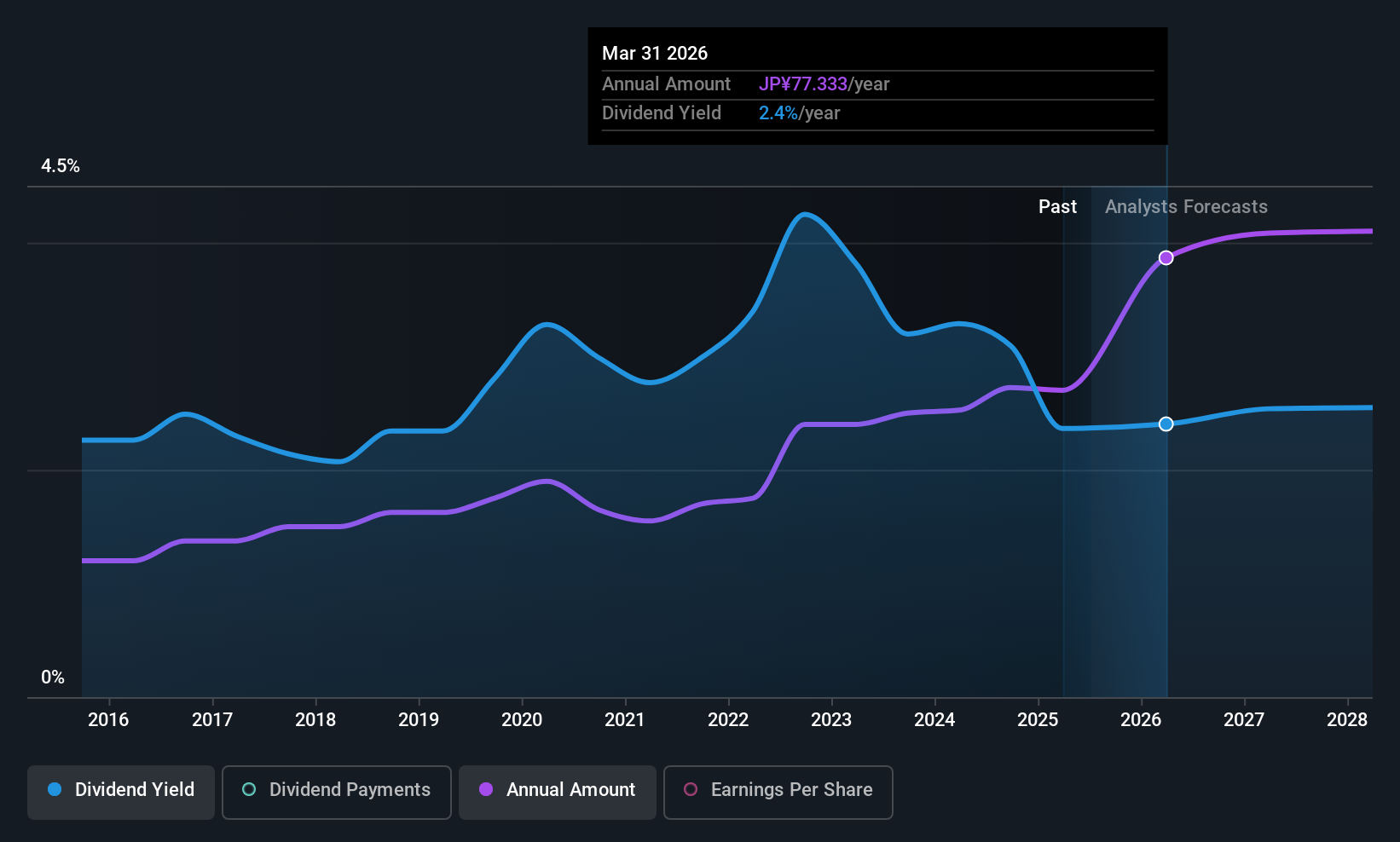

NIKKON HoldingsLtd's Payment Could Potentially Have Solid Earnings Coverage

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. The last payment was quite easily covered by earnings, but it made up 7,332% of cash flows. The company might be more focused on returning cash to shareholders, but paying out this much of its cash flow could expose the dividend to being cut in the future.

Looking forward, earnings per share is forecast to rise by 9.2% over the next year. If the dividend continues on this path, the payout ratio could be 46% by next year, which we think can be pretty sustainable going forward.

View our latest analysis for NIKKON HoldingsLtd

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. Since 2015, the annual payment back then was ¥20.50, compared to the most recent full-year payment of ¥74.00. This means that it has been growing its distributions at 14% per annum over that time. NIKKON HoldingsLtd has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

NIKKON HoldingsLtd May Find It Hard To Grow The Dividend

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. However, NIKKON HoldingsLtd's EPS was effectively flat over the past five years, which could stop the company from paying more every year. The company has been growing at a pretty soft 1.5% per annum, and is paying out quite a lot of its earnings to shareholders. While this isn't necessarily a negative, it definitely signals that dividend growth could be constrained in the future unless earnings start to pick up again.

In Summary

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. As an example, we've identified 1 warning sign for NIKKON HoldingsLtd that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if NIKKON HoldingsLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:9072

NIKKON HoldingsLtd

Engages in the cargo transportation businesses in Japan and internationally.

Adequate balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor